Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CREDIT MACRO

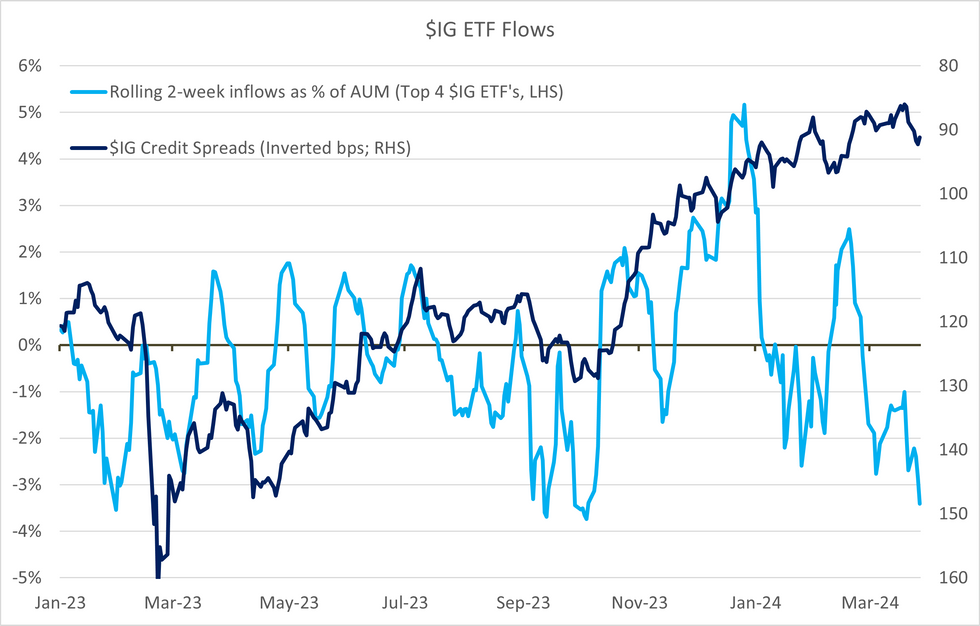

- Heavy outflows reported for week ending Wednesday in $ - we already flagged that after heavy outflows in ETF's (below) but we see reports (refinitiv) of conventional outflows adding to that - as we said yest. ETF's have stabilised since - but still no signs of inflows.

- €IG saw net outflows, €HY more flat. We wouldn't get too excited about firmer flows in €HY than $ - secondary spreads still decompressed & the much larger $HY ETF space is driving the weakness there (refinitiv reported -$2.6b across $HY ETFs).

- Both $ & € continued seeing inflows into govvies while equites including US had 2nd week of outflows - not much surprise - our IG eqv. baskets did reverse higher in tail end of this week (below) - move was matched in spreads.

- We noted govvie vs. credit divergences breaking yield buying narrative last week - that's continuing in flows with now more noticeable impact in secondary. Between Friday & Tuesday €IG widened +9bps (avg. +3/session) - sizeable moves given YTD vol has been low (avg.<0.5bps) with only 2 sessions outside of that' seeing 2+ widening.

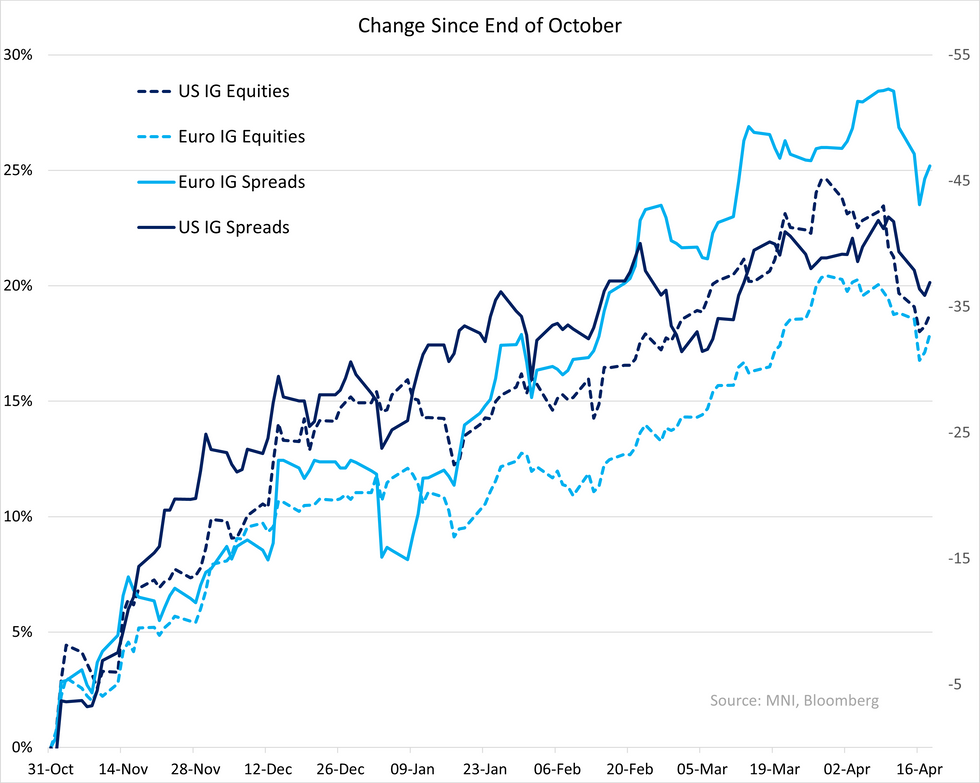

- Supply continues to be in backseat; $IG at $32b (vs. c$30b) on well expected bank supply (90% of it) while local supply remains more mute shy of €20b including covered's.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok