Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EGBS

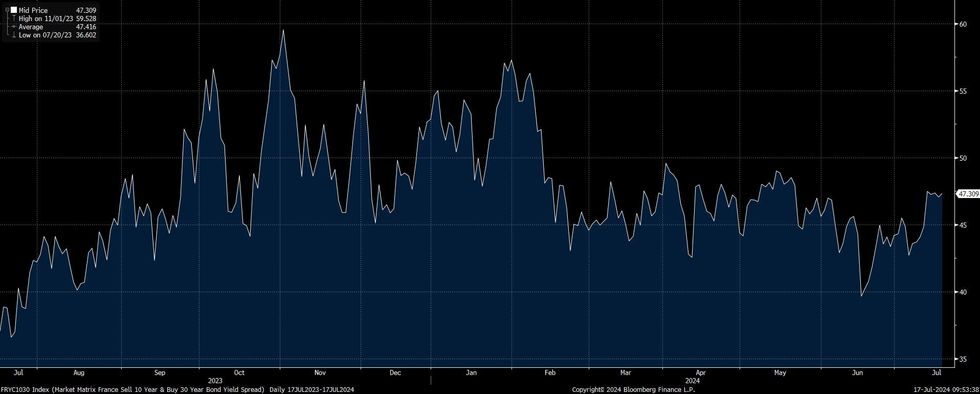

The 10-/30-Year BTP/OAT box sits just below its July closing high, and ~2bp below its ’24 closing high.

- A period of prolonged French political and fiscal risks could weigh on the structure.

- Relative Italian political stability would be a factor in that instance, even as the country faces some of its own fiscal issues.

- Italian 10s30s may be turning, with the recent run of steepening stalling at multi-month highs around the 60bp mark.

- Meanwhile, the French curve will become more susceptible to steepening pressure the longer the French political and potential fiscal impasse rolls on.

- March’s price action shows how quickly the tide can turn, although we note that BTP beta to wider EGB fiscal worries could provide some limitations to the downside.

- Here, we point to the French situation being viewed as idiosyncratic, as opposed to a systemic threat to the Eurozone, which should allow BTPs to outperform if French fiscal worry becomes more pronounced.

Fig. 1: 10-/30-Year BTP/OAT Box (bp)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok