Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

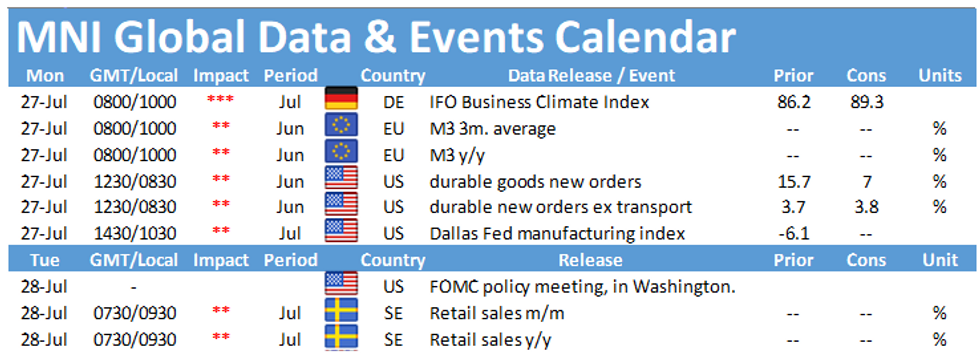

Monday's data calendar sees a quiet start to the week, with the only release worth noting being the publication of the Ifo business climate indicator at 0900BST. In the US the highlight of the day is the releases of durable goods orders at 1330BST.

Ifo business climate index seen higher

The Ifo business climate index rose to the highest level since February in June, picking up 6.5pt to 86.2, the steepest increase on record. In July markets are expecting another increase to 89.3 which would be third successive gain but still below pre-crisis levels. Current conditions plunged in April, fell slightly further in May and only recovered marginally in June. The indicator edged up to 81.3 in June and markets look for a small gain in July to 85.3. On the other hand, expectations rebounded sharply in May after the plummeted in April. June saw another strong increase in expectations and in July the index is seen higher at 93.2 which would be the highest reading since December 2019. Similar survey evidence suggests a downside risk for expectations. While the ZEW current conditions improved slightly, expectations dropped 4.1pt in July. The Sentix survey posted similar results with current conditions improving to the highest level since March, while expectations declined.

US durable goods orders expected to increase

New orders for manufactured durable goods rose sharply in May, increasing by 15.8% after two consecutive months of decline. Excluding transportation, new orders ticked up 3.7% in May. Markets are looking for another strong reading for durable goods orders by 6.5% in June, while orders excluding transport are seen higher at 3.8%. The ISM manufacturing PMI rebounded in June mainly on the back of a sharp increase in new orders and production. Moreover, the IHS manufacturing PMI for June reported a stabilization of new orders.

There are no events are currently scheduled for Monday.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.