Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA RATES

Goldman Sachs view “active CGB trading as part of the PBOC's regular open market operation toolbox, rather than QE.”

- They suggest that active CGB trading may mean that “policymakers gain better control of market interest rates, and thus reduce the risk of unintended over-tightening/loosening of financial conditions.”

- They also believe “the upcoming acceleration of government bond issuance implies limited room for further decline in market rates in the near term.”

- The recent policymaker communique on this front shouldn't be a surprise to MNI subscribers. A recent exclusive from our Beijing team (published on April 11) noted that the PBoC will “continue to monitor the longer-dated Chinese government bond market, adding supply and control over leverage to help guide 10-Year CGB yields closer to the present 2.50% one-year MLF rate.”

- Goldman go on to flag that “paying front-end IRS would provide some protection against tighter front-end liquidity conditions due to the likely large volume of government bond supply in the coming months.”

- Finally, they take profit on their long 1-Year CGB trade recommendation for a potential gain of 60bps (entered on 10 November ‘23).

- This comes after CGB yields moved off cycle lows following Tuesday's comments from policymakers.

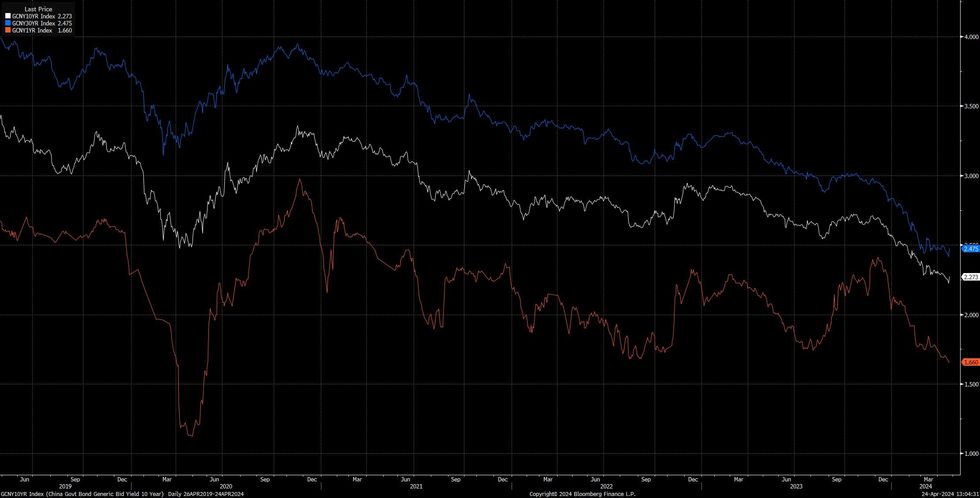

Fig. 1: China 1-, 10- & 30-Year Yields (%)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok