Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EGBS

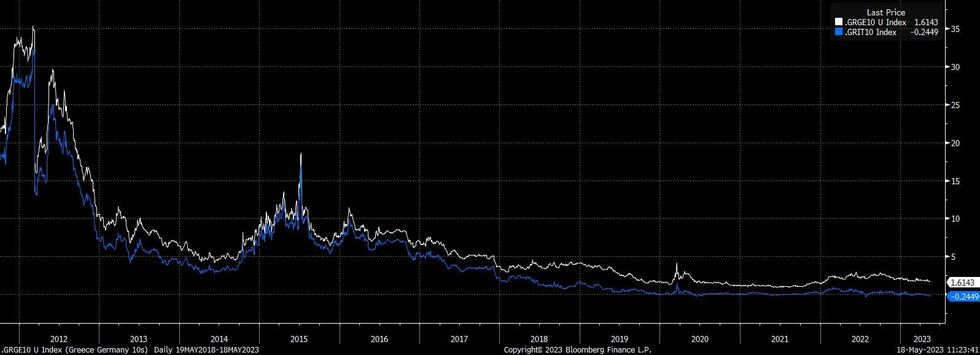

The recent run of Greek 10-Year compression vs. Bunds extends, leaving that spread around the 160bp mark (based on generic yields), the tightest level observed since the early part of ’22.

- 10-Year GGBs have also outperformed BTPs, trading through by ~25bp, operating within ~5bp of the all-time spread extremes printed in ’22.

- The lack of willingness for ECB terminal rate pricing to push meaningfully above the 3.75% mark on a consistent basis is helping.

- Looking ahead, the national election provides the highlight in the immediate term and could also provide the key explanatory factor for the tightening of Greek paper.

- Polling ahead of the 21 May election shows PM Mitsotakis' centre-right New Democracy is on course to win a plurality of seats, but fall short of an overall majority. The centre-left PASOK are likely to emerge as the kingmakers post-election (expect our political risk team’s preview of this event to be released tomorrow). A New Democracy-led parliament would be a more pro-business/economy outcome, although the country’s economy isn’t the worry area that it once was (largely owing to lasting fiscal support from broader Europe).

- Goldman Sachs have noted that the incumbent government “plans to almost triple European Recovery and Resilience Facility spending throughout 2023 and a convincing delivery upon this commitment will likely be the final step for Greek government bonds to regain investment grade rating.” Focus on the eventual attainment of IG status, assuming the incumbent ruling party prevails, is likely factoring into the compression.

Fig. 1: Greek 10-Year Spreads Vs. German & Italian Equivalents (%)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok