Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

China data was uniformly better than expected, Q4 GDP was flat against a -1.1% forecast, which left y/y growth at 2.9%, also above expectations, but down from the 3.9% pace seen in Q3. IP (+1.3% y/y, versus 0.1% forecast) and retail sales (-1.8% y/y, -9.0% forecast) also comfortably beat expectations. Both measures are also above trough points in recent years (which coincided with previous Covid waves).

- FAI and property investment were both a touch better than expected, but property sales remained very depressed at -28.3%, little changed from November.

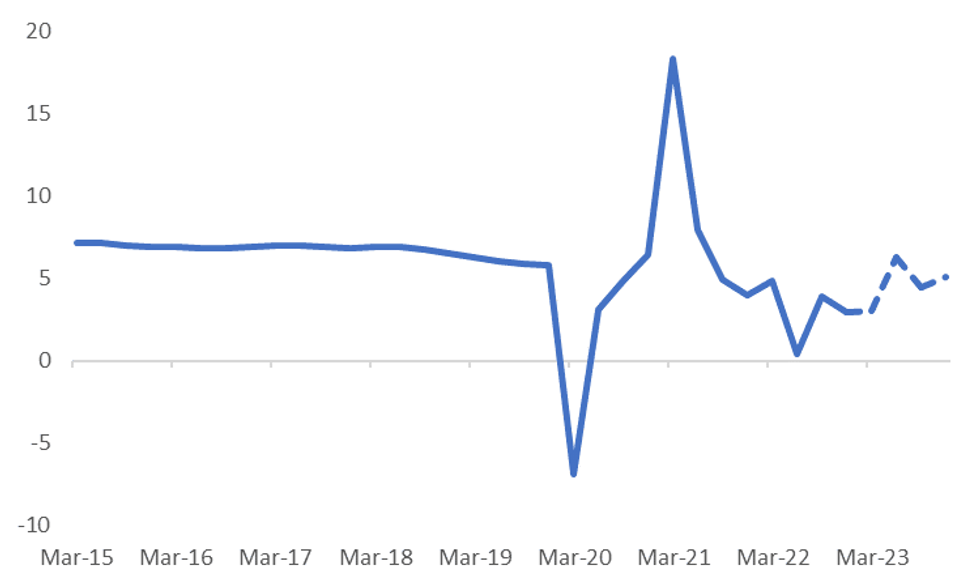

- The consensus expectation is growth momentum will improve from here, see the chart below, with the dashed lines the consensus y/y projections for 2023. We are expected to be back above 6% by Q2, although part of this reflects base effects versus 2022.

- This is well above projected pace for other major economies/regions. EU y/y GDP growth is expected to be negative in Q2 (-0.3%) and modestly positive for the US (+0.8%).

Fig 1: China GDP Momentum Projected To Improve Through 2023

Source: MNI - Market News/Bloomberg

- Still, the overall projection for 2023 growth is unchanged at 4.8% for the consensus. This is also consistent with a steady J.P. Morgan Growth Forecast Revision Index (FRI) over recent weeks.

- Forecasters may want to see how the economy unfolds post the recent Covid waves and see genuine improvement in underlying activity before upgrading 2023 aggregate forecasts.

- This factor, coupled with the fact the market has been trading off the re-opening theme for some time may explain today's muted reaction in the Asian FX space to the better than expected data outcomes.

- The second chart below shows the J.P. Morgan ADXY Y/Y momentum is already on the improve at this stage, so some of the re-opening story is already priced to a degree.

Fig 2: ADXY Y/Y & China Industrial Production Growth

MNI: J.P. Morgan/MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok