Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

Powell said at the press conference the two criteria for assessing the impact of higher long-end yields were a) whether they are persistent and b) whether they reflect Fed hiking expectations. And "In terms of how to think of the translation into rate hikes, I think it is just too early to be doing that."

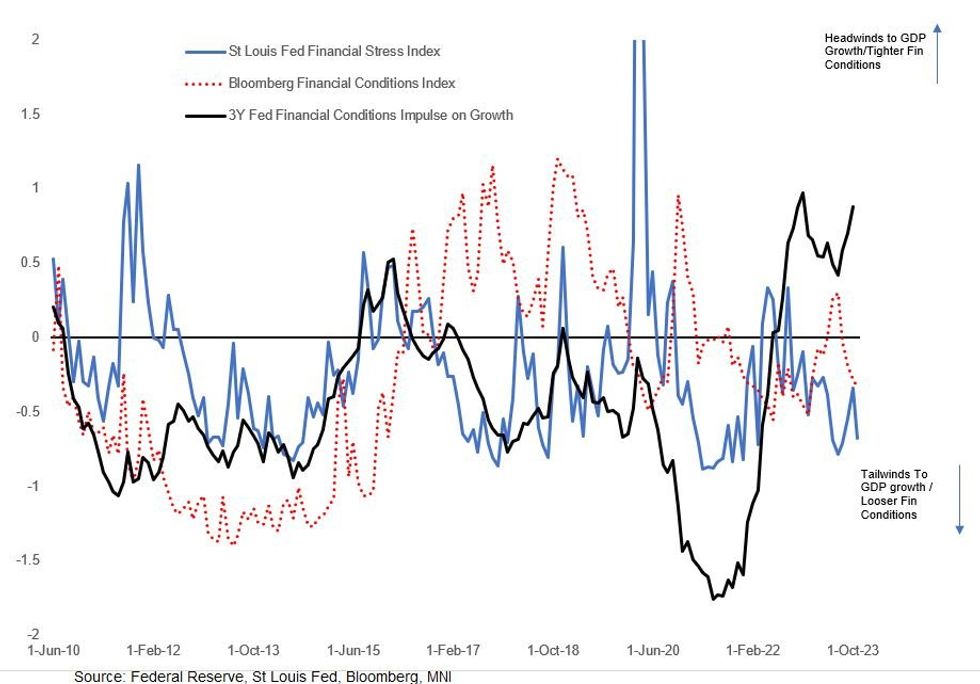

- Recent price action may mean his 1st criterion has not held. Indeed at that time, analysts had estimated that the financial conditions tightening in October was equivalent to between 1-4 rate hikes - with yields falling back, the dollar weakening, and equities higher since then, that's changed.

- Indeed at that time, analysts had estimated that the financial conditions tightening in October was equivalent to between 1-4 rate hikes - with yields falling back (10Y yields are around 38bp lower than at the beginning of the latest meeting), the dollar weakening, and equities higher since then, FOMC speakers have been pushing back a little more against rate cut talk – our PDF includes Fed speaker highlights from this month.

- FOMC speakers have re-emphasized of lingering upside inflation risks and potential for further cuts - which suggests that the FOMC is unlikely to remove its tightening bias despite the apparent progress in the October jobs/inflation data released since the Nov 1 decision.

- Some key post-CPI comments in this regard include multiple FOMC participants who have a dovish reputation: For instance, Boston Fed's Collins "I wouldn’t take additional firming off the table" ; SF's Daly "we are not certain whether inflation is on track to return to 2%...I wouldn’t want to declare victory"; and Gov Cook "I see risks as two sided, requiring us to balance the risk of not tightening enough against the risk of tightening too much".

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok