Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

POLAND

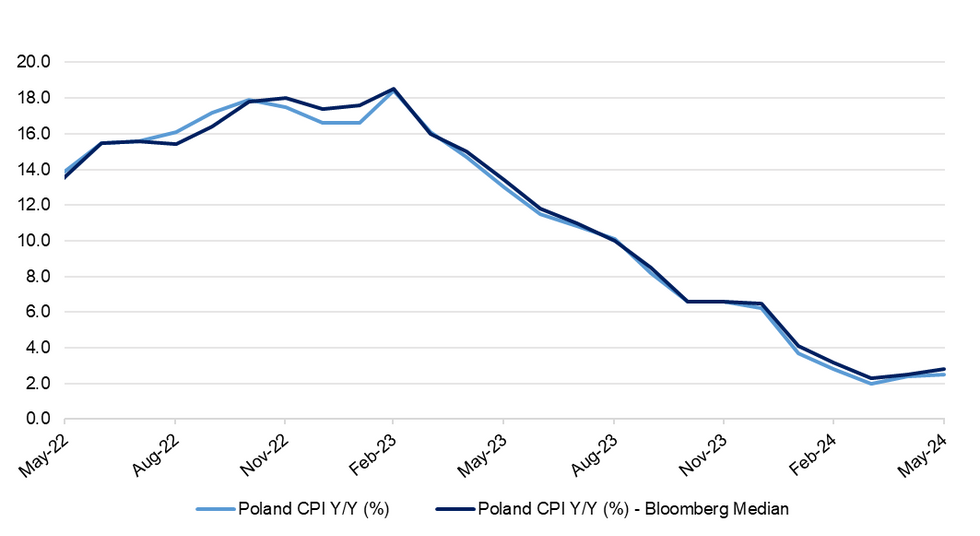

Preliminary data showed that Poland's headline inflation undershot expectations in May, printing at +2.5% Y/Y (i.e. right at the NBP's point-target). Consensus was looking for an acceleration to +2.8% from +2.4% registered in April. On a sequential basis, prices ticked higher by just 0.1% M/M versus +0.5% expected and +1.1% in April.

- ING call the price increase in May "symbolic," noting that small declines in fuel and heat prices were coupled with a very small rise in the costs of food. Per their calculations, core inflation may have fallen to around +3.8-3.9% Y/Y. They note that a slightly slower sequential core inflation (+0.2% M/M) is typical for May. They maintain their call for stable rates through the rest of 2024 as the economy is rebounding.

- mBank estimate that core inflation fell further to +3.8% Y/Y from +4.1%, while noting that it is difficult to say how the reaction in food prices to recent VAT adjustments played out before the publication of detailed data.

- Pekao suggest that core inflation fell to +3.9% Y/Y, adding that forecasts suggesting that headline inflation could end the year at +6-7% Y/Y are "going through a difficult time."

- PKO write that prices rose 0.1% M/M mostly on the back of an increase in food prices, which was largely neutralised by cheaper fuel and heat.

- The Polish Economic Institute write that core inflation likely fell to around +3.8% Y/Y. They note that food prices ticked higher by a small margin, despite a higher VAT rate. They believe that June will be the last month with inflation within the NBP's target. CPI may accelerate to +4.0-4.5% Y/Y in July due to the adjustments to energy price caps. A rebound in core inflation cannot be ruled out due to wage pressures. The Institute warn that 2H2024 will also bring higher inflation.

Fig. 1: Poland CPI Y/Y (%) vs. Bloomberg Median

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok