Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

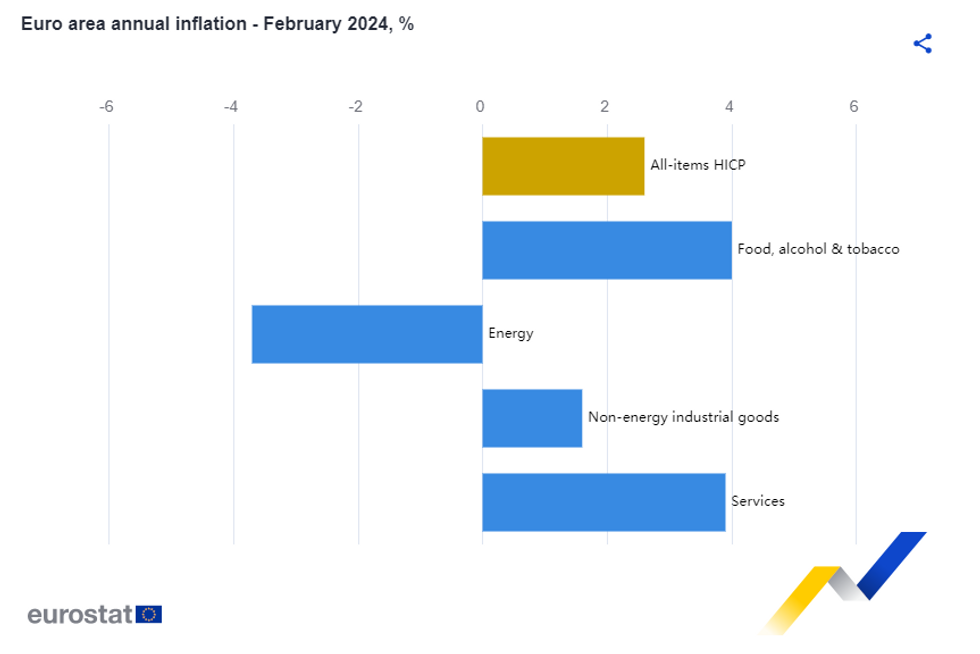

Eurozone flash inflation for February printed at +2.6% Y/Y (vs +2.5% cons;+2.8% prior) while core (ex-energy/food) was +3.1% Y/Y (vs 2.9% cons; +3.3%prior). Monthly NSA prints were 0.6% for headline and 0.7% for core.

- The unrounded prints were 2.58% Y/Y, 0.62% M/M for headline inflation, and 3.08% Y/Y for core.

- The national releases over the past two days have been come in firmer than expected for the core measure, driven by services stickiness. This has led analysts to increase their estimates for the core rate to 3.0-3.2% Y/Y, suggesting the figures out now were largely priced in.

- For the headline figure, the print was also in line with analyst tracking estimates, and the early consensus.

- We await the ECB's seasonally-adjusted series due out later today for a better indication of sequential momentum.

- Of the core components, services disinflated only slightly to +3.9% Y/Y (vs +4.0% prior) while non-energy industrial goods came in at +1.6% Y/Y (vs +2.0% prior). Monthly NSA rates were positive for both (0.8% for services, 0.3% for NEIG).

- Food, alcohol, and tobacco inflation was 4.0% Y/Y (vs 5.6% prior), with the disinflation trend continuing.

- At a country level, the February Y/Y prints were lower (or the same) in 16/20 countries than in January. On a monthly basis, no countries saw M/M NSA deflation.

Eurostat

Eurostat

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok