Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

US retail sales saw surprising strength in November, with the headline reading up 0.3% M/M (-0.1% survey, -0.2% prior revised).

- The core figures, while offset by downward revisions, surprised to the upside as well: ex-auto +0.2% M/M (-0.1% survey, 0.0% prior revised), ex-auto/gas +0.6% M/M (+0.2% survey, +0.1% prior unrevised), and the GDP input control group +0.4% M/M (+0.2% survey, albeit 0.0% prior revised down from 0.2%).

- November saw a rebound in motor vehicle/parts sales (to +0.5% from -1.1%), furniture (+0.9% from -2.2%), clothing (+0.6% from -0.1%), offset by greater weakness in misc store retailers (-2.0% from +0.7%) electronics/appliances (-1.1% from +1.1%) and building materials (-0.4% from -0.1%). Gasoline prices spurred a bigger contraction in sales (-2.9% from -1.2%).

- Standout positive categories included food services/drinking places (+1.6% from +0.6% prior), and nonstore retailers (+1.0% from -0.3% prior),

- Health and personal care, food and beverage shops saw slower but positive growth vs October.

- Overall, after a soft reading in October, this report suggested decent strength in private consumption going into year-end. The downward revision in October control group sales may take the sheen off the report though, as it relates to Q4 GDP calculations.

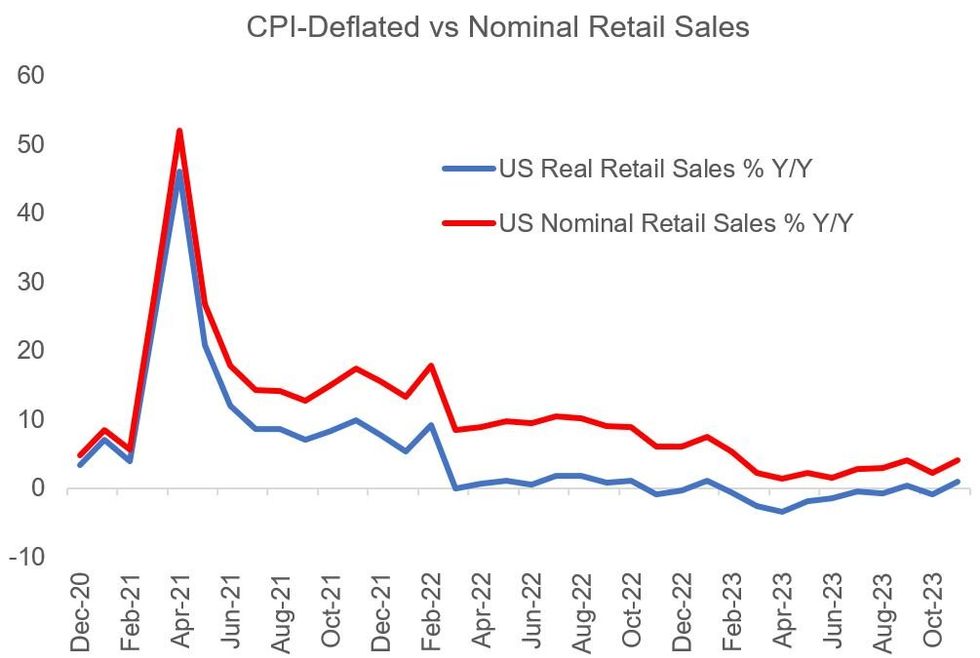

- From a longer-term perspective, the deceleration in inflation combined with steady/improving nominal retail sales saw the strongest Y/Y growth - and first positive Y/Y reading - in "real" retail sales since January.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok