Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

UK DATA

MNI (London)

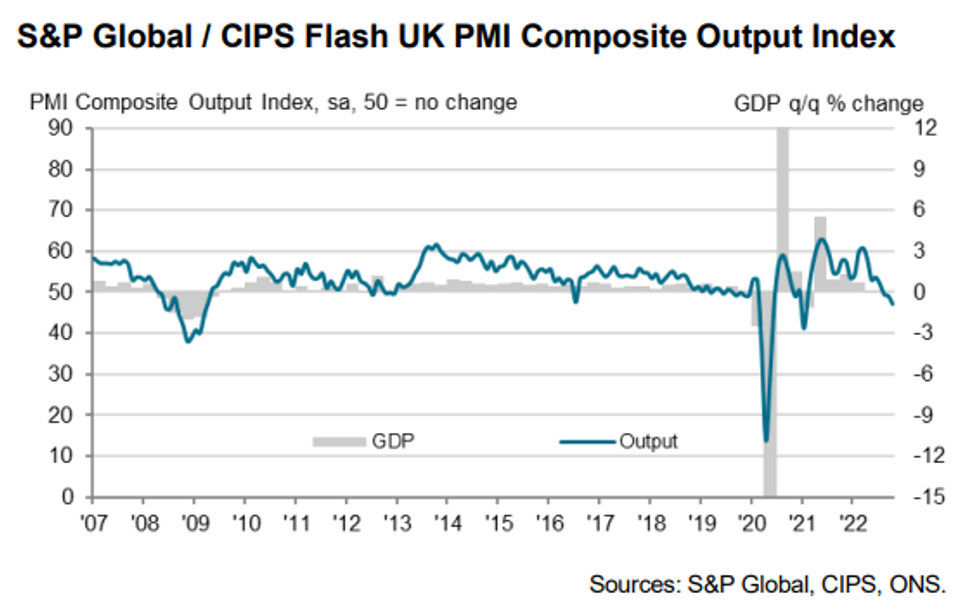

UK OCT FLASH SERVICES PMI 47.5 (FCST 49.0); SEP 50.0

UK OCT FLASH MANUFACTURING PMI 45.8 (FCST 48.0); SEP 48.4

UK OCT FLASH COMPOSITE PMI 47.2 (FCST 48.0); SEP 49.1

- The UK PMIs noted a deepening contraction in the October flash, both coming in weaker than anticipated.

- The October data saw the sharpest fall in services activity since January 2021 lockdowns. The composite index contracted for the third consecutive month and was the lowest since March 2009 when excluding pandemic lockdowns.

- Manufacturing slumped due to slowing demand and continued supply issues, whilst services contracted as inflation concerns, recessionary fears and political uncertainty saw consumer confidence weaken further.

- Highlights from the press release:

- "UK private sector firms ... indicated a steep fall in business expectations for the year ahead, with optimism the lowest since April 2020."

- "Overall input cost inflation eased to its lowest since September 2021. Average prices charged by private sector firms increased sharply during the latest survey period, although the rate of inflation moderated to its lowest since August 2021."

- "New business levels decreased at the sharpest rate since January 2021. Manufacturers experienced an especially steep fall in new work, exacerbated by the fastest downturn in export sales for nearly two-and-a-half years."

- "Staff hiring remained a relatively bright spot in October. The rate of private sector job creation was nonetheless the slowest for 20 months."

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok