Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

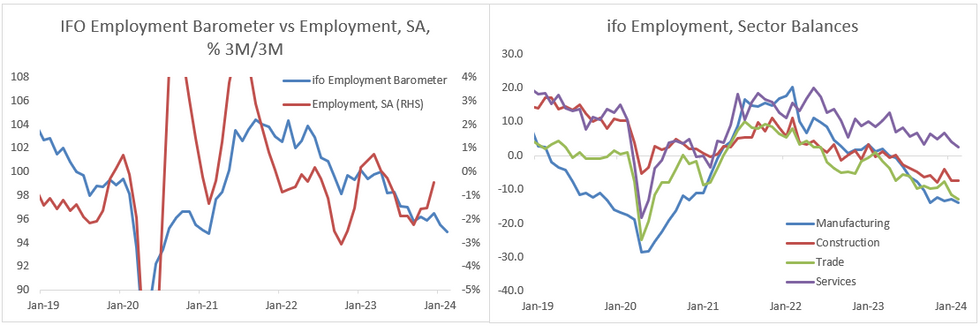

The IFO Employment Barometer for February came in lower again, at 94.9 (vs 95.5 Jan), the weakest value since February 2021 and the second consecutive downtick. Overall, the report seems to confirm an ongoing modest softening in Germany's labour market, with the relative resilience of the private services sector not making up for weakness in manufacturing. This could begin translating into reduced upward wage pressures, a key concern for the ECB in considering when to cut rates this year.

- The decrease was broad-based, with all subindices ticking down except construction, which was almost unchanged at a weak level (-7.4 vs -7.3 prior). Specifically, the manufacturing balance printed -13.9 (vs -12.9 prior), trade came in at -13.0 (vs -11.7, the fourth consecutive downtrend and the weakest level since the height of the pandemic).

- Services remains the only subindex in expansionary territory but is also on a downtrend, printing 2.5, its weakest level since February 2021.

- Alongside the weak employment trends in the manufacturing sector, also recruitment momentum in the services sector has weakened considerably. Demand for IT service providers and consultants remains strong, however, according to IFO.

- The survey suggests further continued weakness in the private sector labour market in early 2024. The German Q4 employment report showed an increase in total employment (to 46.2m, +0.06% Q/Q SA, +28k vs -0.02% prior) driven by the services sector, in which employment rose +0.06% Q/Q (SA, +20k, vs +0.09% prior). But this was driven by the "public service providers, education, health" subsector (+0.34 Q/Q SA at 41k, vs +0.38% prior), excluding which employment fell -0.04% Q/Q (SA, -13k, vs -0.16% Q/Q).

- February's Flash PMIs showed the employment component falling only fractionally on aggregate, with a divergence in sectoral activity as services strengthened and manufacturing deteriorated.

MNI, ifo

MNI, ifo

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok