Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

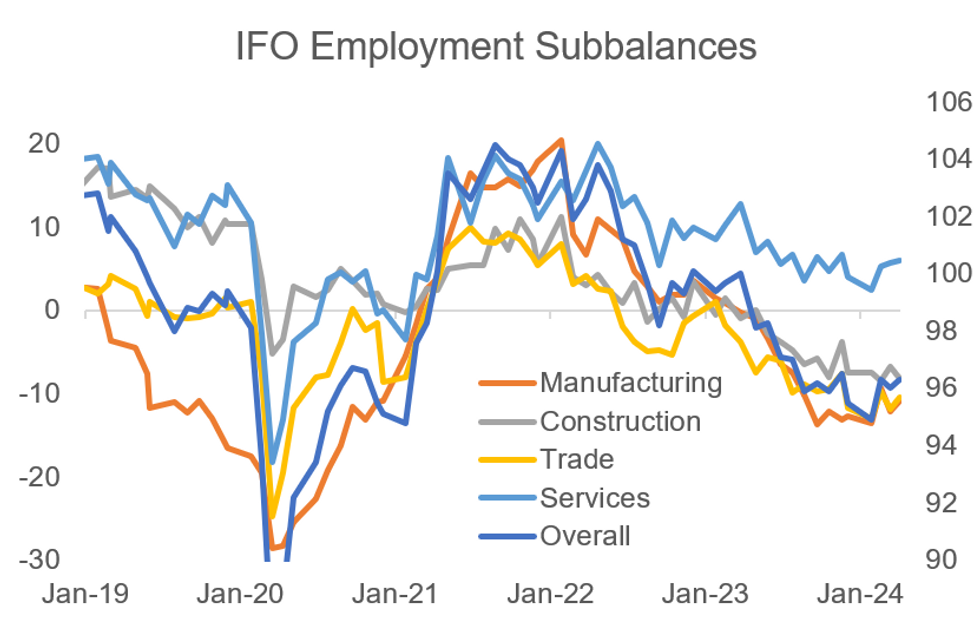

The IFO employment barometer rose slightly in April, reversing March's decline, to stand at 96.3 (96.0 prior).

- The uptick was relatively broad-based from a sectoral standpoint, as all but the construction sub-index firmed.

- While the overall print is back to around mid-2023 levels, "the demand for labour remained relatively weak", IFO notes.

- Still, only the services sector experienced an expansion in employment (+0.2 to 5.7). Construction (-1.4p to -8.2), manufacturing (+1.3p to -10.9) and trade (+1.3p to -10.5) all remained in contractionary territory.

- IFO flagged that tourism firms are looking for new employees ahead of the summer season. Consulting firms are also looking to expand their workforce. Enterprises in the construction sector are reducing their personnel planning amid order shortages.

- The data seems broadly in line with/a little a bit weaker than the employment index seen within May's Germany flash PMI. The latter showed a slight pick-up around its long-term average, with the services sector being the sole upside driver.

- Official German statistics show employment rising gradually (Q1 +0.1% Q/Q SA), also driven by the services sector (public and financial sectors specifically), while construction employment fell ('GERMAN DATA: Employment Rebounds In Q1 On Services, With More Hours Worked' - MNI, May 17).

- Looking ahead, the data suggests that there is no major lagged wave of redundancies driven by the sluggish manufacturing sector, and that overall employment will likely hover around current levels in the coming months.

MNI, Destatis

MNI, Destatis

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok