Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

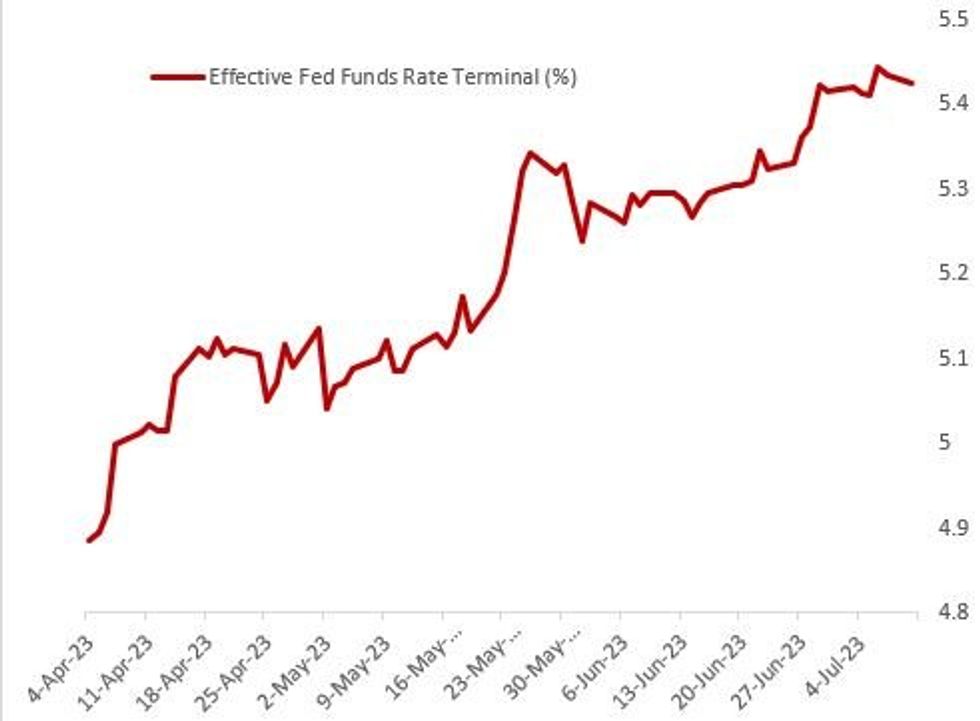

Fed hike pricing is settling slightly softer after Friday's headline payrolls miss (our review here), with a quiet data slate putting attention on FOMC speakers ahead of Wednesday's CPI print.

- After dipping an implied 0.5bp overnight on OIS amid soft China inflation data, July hike pricing has regained ground and is basically where it was before Friday's employment report at 22.5bp priced (90% prob of a quarter-point raise).

- Conversely, a tick higher overnight in implied hikes for meetings beyond July has reversed: the path sees a cumulative 28.5bp to September and 34.4bp through the November peak. That peak pricing - implying effective Fed funds of 5.42% is 1.8bp lower than the overnight high and almost a full 3bp below just before the payrolls release.

- A full 25bp cut from the terminal rate doesn't materialize until the May 2024 FOMC.

- With only limited data on the agenda (wholesale inventories), there will be attention on Fed speakers including Barr, Daly, Mester, and Bostic. Note that this is the final week of communications before the pre-meeting blackout period.

Source: BBG, MNI

Source: BBG, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok