Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

China June trade data was mixed, with exports up 8.6% y/y, versus 8.0% forecast and 7.6% prior. Imports fell though, down 2.3% y/y, against the +2.5% forecast and 1.8% prior. The trade surplus, as a result of the import miss surged to $99.05bn, well above expectations and surpassing previous cycle highs seen in mid 2022.

- Export growth, which has been a bright spot in recent months, sits close to 2024 y/y highs. Base effects from 2023 were favorable. By country, exports rose in m/m terms to the US, EU, Japan and South Korea, while falling to ASEAN economies.

- Exports to US were just above $45.5bn, well below 2021/22 highs but likely to be a focus point in the lead up to the US election in November.

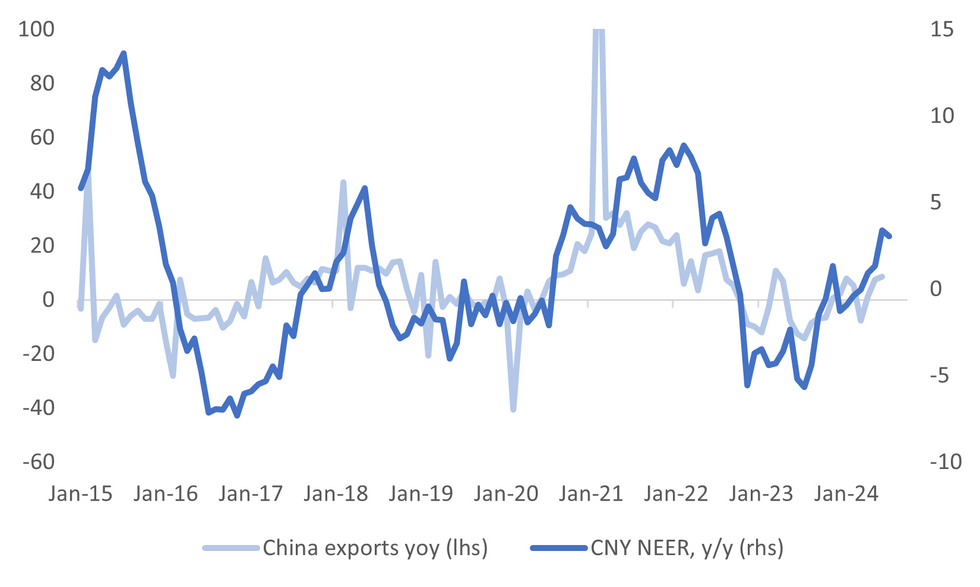

- The CNY NEER gains, in y/y terms, is still broadly in line with export growth, see the first chart below. The NEER may be running a little ahead but is within historical norms.

Fig 1: China Export Growth & CNY NEER Y/Y

Source: MNI - Market News/Bloomberg

- On the import side, y/y growth at -2.3% is above 2024 lows, but has largely displayed a sideways trends since Q4 last year from a growth standpoint. Base effects are favorable in coming months but the data may keep domestic demand concerns still in play.

- In terms of commodity import volumes, we were generally down in m/m terms. Crude oil (-1.1% m/m), refined oil products, iron ore (-4.3%m/m) and natural gas were down. The only notable rise came from coal.

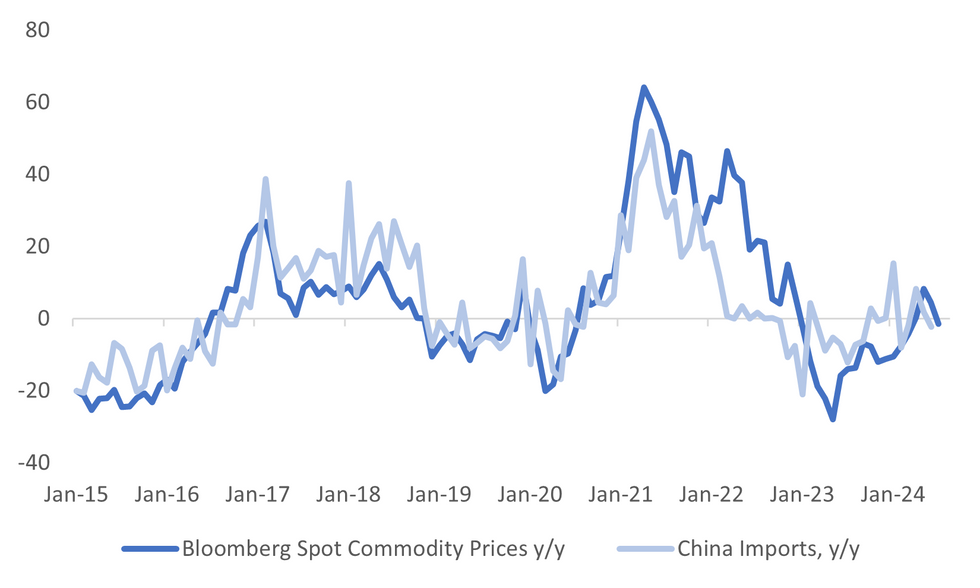

- The second chart below shows the reasonable link between China's import growth and spot global commodity prices.

- Note on Monday we get June activity figures and Q2 GDP growth. Net exports looking to be a positive for the quarter.

Fig 2: China Imports & Global Spot Commodity Prices - Y/Y

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok