Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ECB

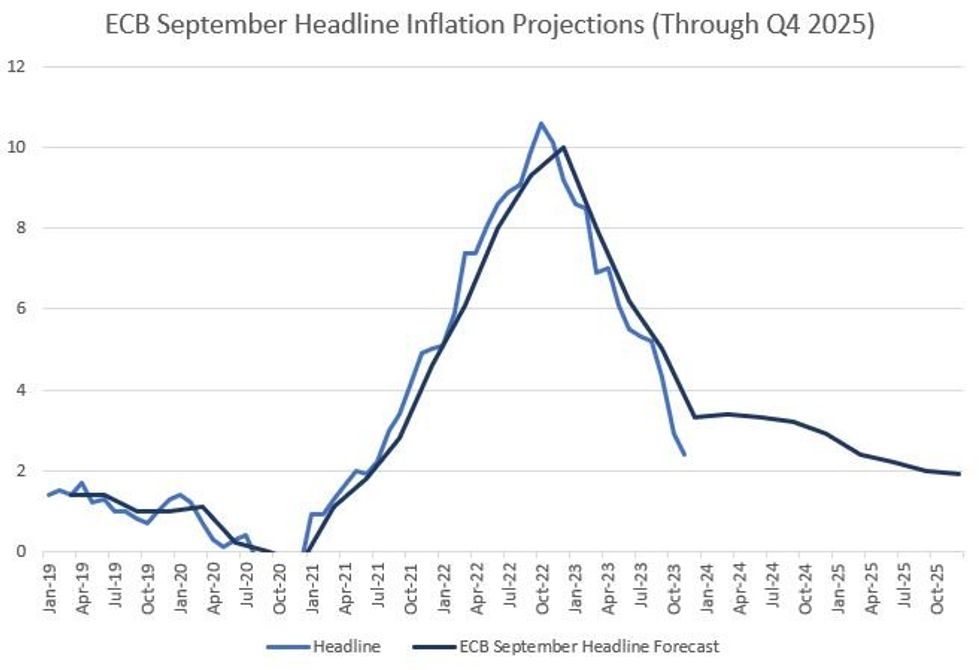

November's Eurozone inflation data (MNI's Insight here) poses further downside risks to the ECB’s near-term inflation forecasts which look likely to be revised downward at the Dec 14 meeting.

- In the September macroeconomic projections, headline inflation was forecast to average 3.3% Y/Y in Q4 2023, while core was seen at 4.1%Y/Y. With HICP averaging 2.65% headline / 3.9% core through the first 2 months of the quarter, it would take a December headline reading of 4.6% Y/Y / core 4.4% (up 2.2pp / 0.8pp respectively from November's flash readings) to reach the ECB's September estimates for the Q4 average.

- While there will almost certainly be an uptick in Y/Y inflation in the next couple of months - largely on energy subsidy-related base effects - the Q4 average headline figure looks likely to come in below 3.0%, with core below 4.0% - i.e. a major undershoot.

- In September, the ECB had projected a small rise in headline to 3.4% in Q1 2024 (up 0.1pp from Q4 2023), with core decelerating sharply to 3.4% (from 4.1%). By year-end 2024, core had been seen steadily declining to 2.5%, with headline 2.9%. Of course, the latter would now actually represent a significant jump from November's reading.

- Given also that energy prices have fallen slightly and the EUR has been steady versus September's technical assumptions (as of the presumed cutoff date mid-last week), there is clearly scope for downward revisions.

Actual Quarterly Average and Monthly Headline HICP % Y/Y; ECB Sept Forecasts From Q3 2023Source: ECB, MNI

Actual Quarterly Average and Monthly Headline HICP % Y/Y; ECB Sept Forecasts From Q3 2023Source: ECB, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok