Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

BOJ

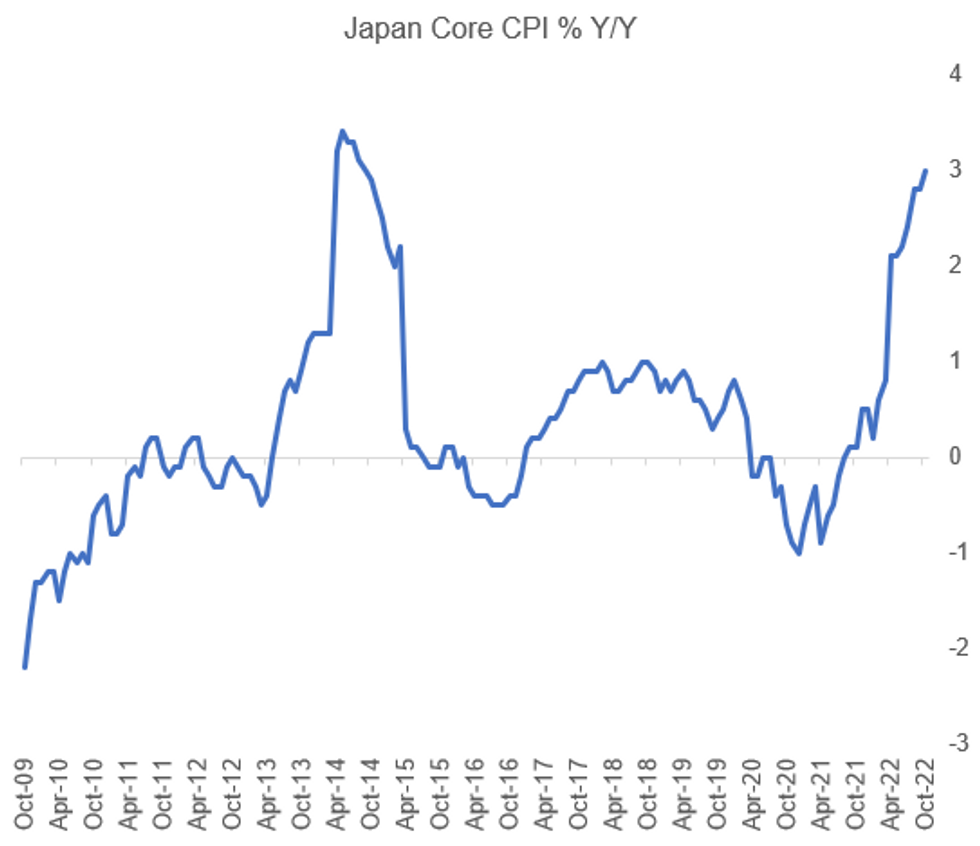

Ahead of the BOJ's re-assessment of the medium-term growth and price outlook at the Oct 27-28 meeting, Kyodo reported earlier today that the BOJ will raise its FY22 CPI forecast to the upper half of the 2% range (ie between 2.5-3%) from 2.3% currently.

- That 2.3% forecast is for Y/Y core for the fiscal year ending Mar 2023; the BOJ is also currently forecasting 1.4% to Mar'24, and 1.3% to Mar '25. The Kyodo report notes that they could tweak CPI forecasts for those fiscal years too - but not to above 2%.

- The current FY forecast increase seems like a plausible revision as it would basically be marking-to-market: Core CPI hit 2.8% Y/Y in August, with September's expected to have come in at 3% (data is out Oct 21st).

- The BOJ upwardly revised this fiscal year's forecast to 2.3% at the July meeting, from 1.9% in April (was 1.1% in Jan).

- Despite intervening to support the Yen on Sept 22 for the first time in 24 years, inflation data and expectations are unlikely to sway BOJ policy (including Yield Curve Control - see MNI INSIGHT: BOJ Unmoved by Rising Inflation, Slumping Yen) MNI's Policy Team reported in August that while the Bank sees core inflation rising close to 3% in coming months, it doesn't expect it to be sustainable without big wage hikes.

- And as per our last BOJ meeting review, we expect the BoJ to remain on hold through the end of Governor Kuroda’s term (which runs into April 2023).

Source: Statistics Bureau of Japan, MNI

Source: Statistics Bureau of Japan, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok