Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWITZERLAND DATA

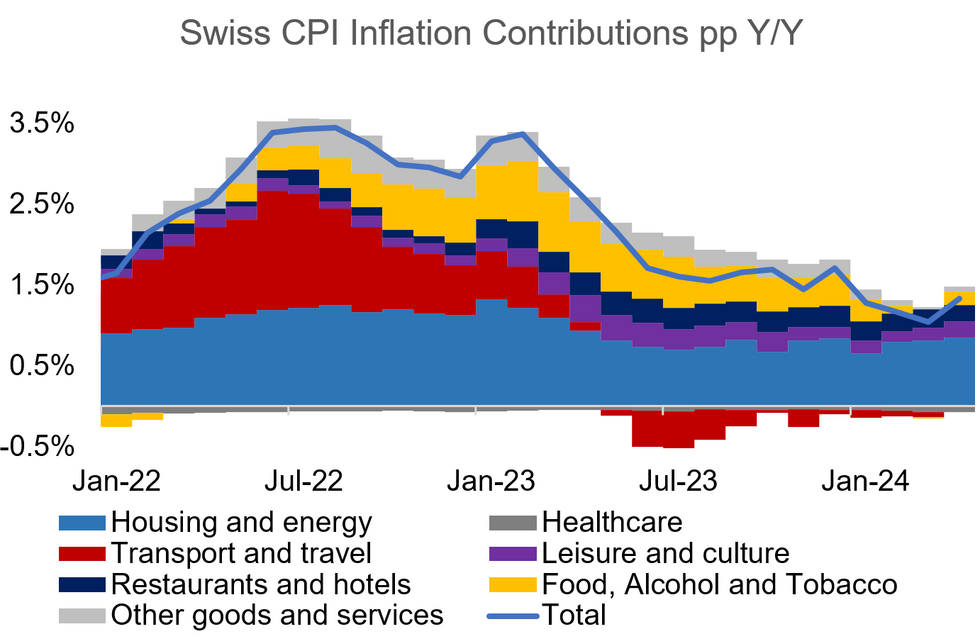

Swiss CPI inflation printed higher than expected at 1.4% Y/Y in April (vs 1.1% cons; 1.0% prior), and 0.3% M/M (vs 0.1% cons; 0.0% prior). Core CPI came in also higher at 1.2% Y/Y (vs 0.9% cons; 1.0% prior). We had flagged upside risks to core in our preview yesterday.

- For the Y/Y headline rate, this marks the first increase after three consecutive declines.

- Re the categories in focus, predominatnely imported inflation realized its expected uptick, at -0.4% Y/Y vs -1.3% Y/Y in March.

- The overall residential rents category (incl. both the actual rental price index and owner-occupied housing) printed flat however vs March at 2.8% Y/Y. The contribution of the housing and energy category rose from 0.82pp to 0.85pp, meanwhile.

- Services inflation remained at +2.0% Y/Y, which means that all of the increase in both headline and core CPI is from the goods side.

- The print opens up some upside risks to the current SNB forecast for Q2 2024 of 1.4%, as rental price inflation might accelerate in the coming months.

MNI, SECO

MNI, SECO

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok