Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

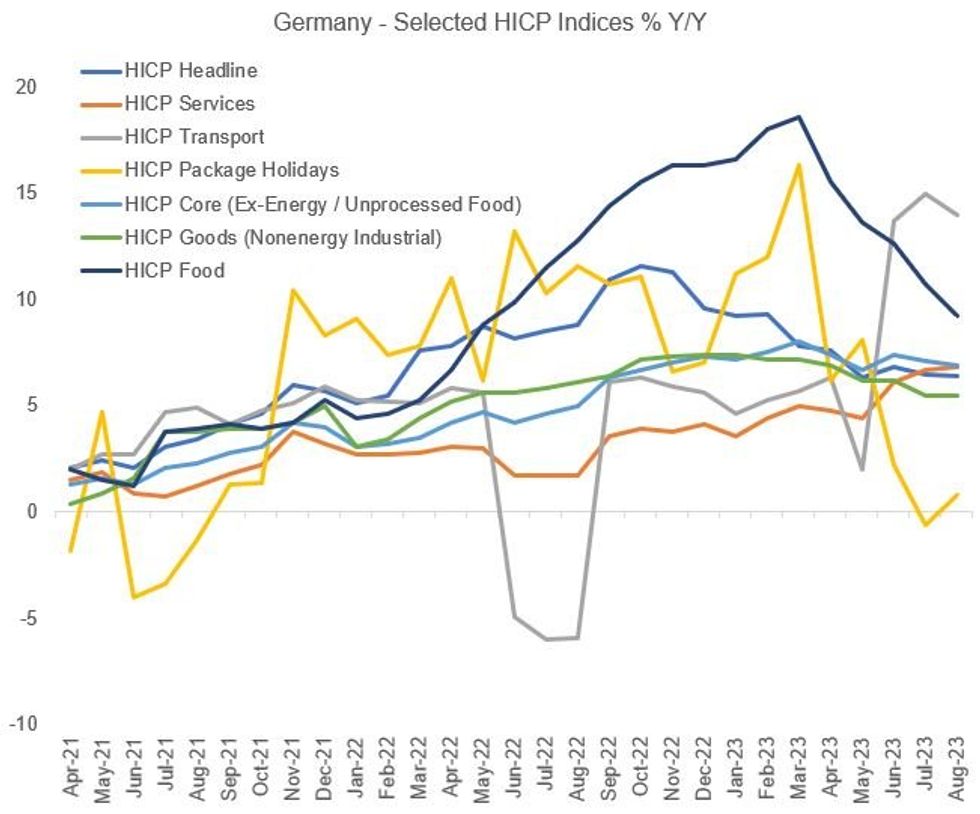

Germany (28% of EZ HICP) – 1300UK Thu 28 September (after state-level data in the morning)

Consensus expectations:

- HICP: 4.5% Y/Y (6.4% prior) / 0.3% M/M (0.4% prior)

- CPI: 4.6% Y/Y (6.1% prior) / 0.3% M/M (0.3% prior)

German inflation is seen to be the largest driver of Euro-area disinflation in September, as base effects relating to the 2022 9-euro travel ticket drop out of the comparison, and pressures from holiday services (which were subject to large weighting changes in the HICP basket in 2023) ease.

- The September flash PMI signalled weaker firm pricing power as a result of the subdued demand environment, with output charges rising at the slowest pace since February 2021. While services prices continued to rise, the rate of inflation was a 28-month low. Input cost inflation ticked up, though, most notably in the service sector due to wage pressures and higher fuel prices.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok