Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

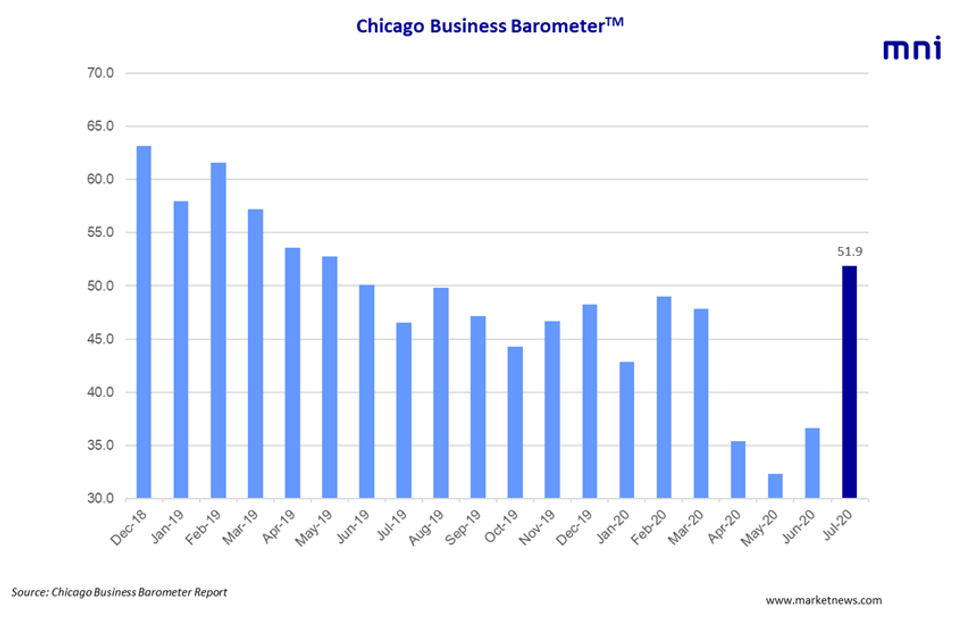

The Chicago Business Barometer bounced back in July from the virus-hit levels seen in H1 and the subdued levels seen through much of late 2019, beating market expectations looking for a smaller gain.

Among the main five main indicators, New Orders and Production saw the largest monthly gains, while Supplier Deliveries eased.

The main points of note from the release follow:

The headline index rose 15.3 points to 51.9 in July, the highest level since May 2019. Business activity recovered following twelve consecutive months of readings below 50. Nevertheless, companies noted continued uncertainty amid the ongoing Covid-19 crisis.

Demand increased sharply in July, recovering from the sharp pandemic hit. New Orders jumped to 53.1, up 23.8 points to the highest level since August 2019. Production strengthened, rising 16.7 points to 50.6, putting the index back into expansion. While some companies noted recovering orders, others reported continued difficulties due to the Covid-19 effects.

Order Backlogs grew 15.3 points to 47.2 in July, marking a near one-year high. However, the index remains in contraction, where it's been since September 2019.

Inventories gained 6.9 points to 46.3 in July after falling sharply in the previous month.

Even though Employment ticked up 8.3 points to 40.1, there was anecdotal evidence that firms had to lay off staff as a result of the current health crisis. However, others mentioned difficulties in finding new staff.

Supplier Deliveries cooled in July, falling 6.4 points to 60.3, the lowest reading since January 2020.

Prices paid at the factory gate edged higher, gaining 1.7 points to 56.9, posting a seven-month high.

This month's special question asked: "Have you updated your contingency plans to control a potential second wave in the future?" The majority, at 51.3%, have planned ahead, while 30.2% have no contingency plans in place. The second question asked: "What is your planned business activity forecast for balance of 2020, by percent?" While 65% of respondents expect growth to be below 5% in 2020, 25% project average growth between 5% and 10%.

The survey ran from July 1 to 20.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.