Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

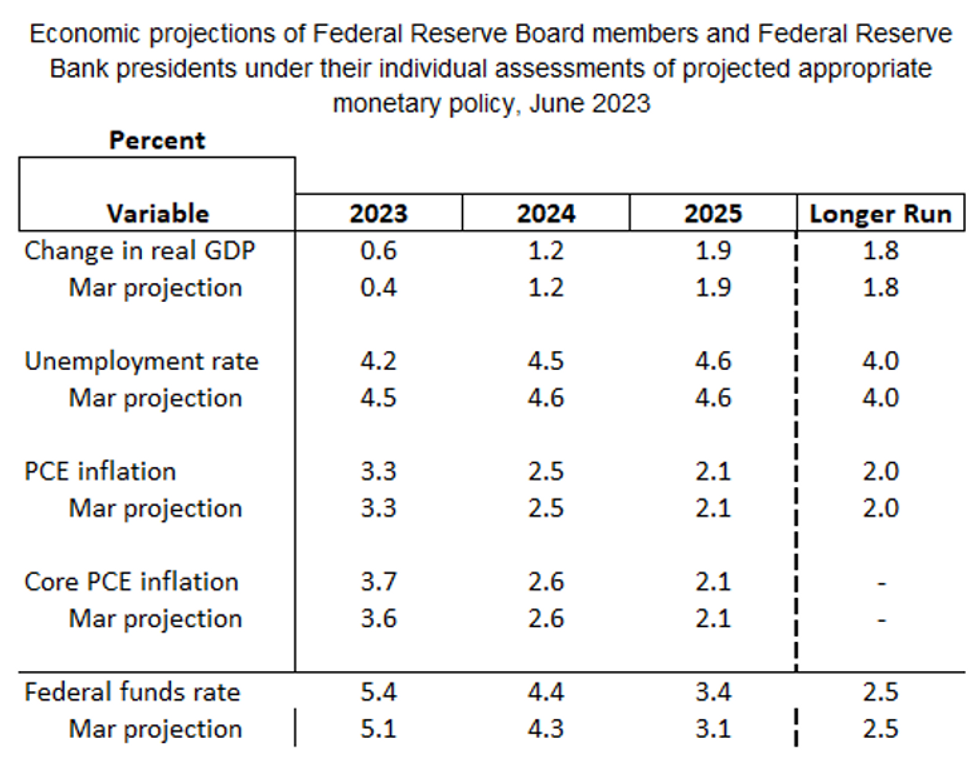

With the May CPI data (though not yet the PCE data that the Fed uses in its projections) in hand, below are MNI's expectations for the June Summary of Economic Projections.

- Outside of the Fed funds rate medians, we don’t expect many changes in the projected SEP macro variables in the June edition.

- There could be an uptick in the GDP growth rate for 2023 based on recent activity data tracking through Q2 and a modest tweak to PCE inflation projections.

- But the biggest change is likely to be to the 2023 unemployment rate. Even with the 0.3pp uptick in May, at 3.7% the unemployment rate would have to rise a fairly rapid 0.8pp in the remaining months of the year to reach the FOMC’s 4.5% March projection.

- We think the FOMC median will split the difference and revise the end-2023 unemployment rate down a few percentage points though we’ve seen sell-side expectations as low as 4.0%.

- Indeed that lower unemployment forecast combined with stronger GDP growth may force an upward revision to end-year PCE prices as the implication of a tighter jobs market.

- The March estimates of 3.3% headline PCE / 3.6% core are exactly in line with current analysts' estimates consensus, but we see core PCE at least being raised for 2023.

Source: MNI Expectations

Source: MNI Expectations

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok