Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

One question that has emerged from the hotter-than-expected March CPI data is how well it will translate into the Fed's preferred PCE measure (due out April 26). Some initial post-CPI estimates of March core PCE eye 0.3% M/M (Citi, Wrightson ICAP), in other words lower than the core CPI print (0.36%). JPMorgan is now pencilling in 0.26% which would be exactly the same as February's PCE print.

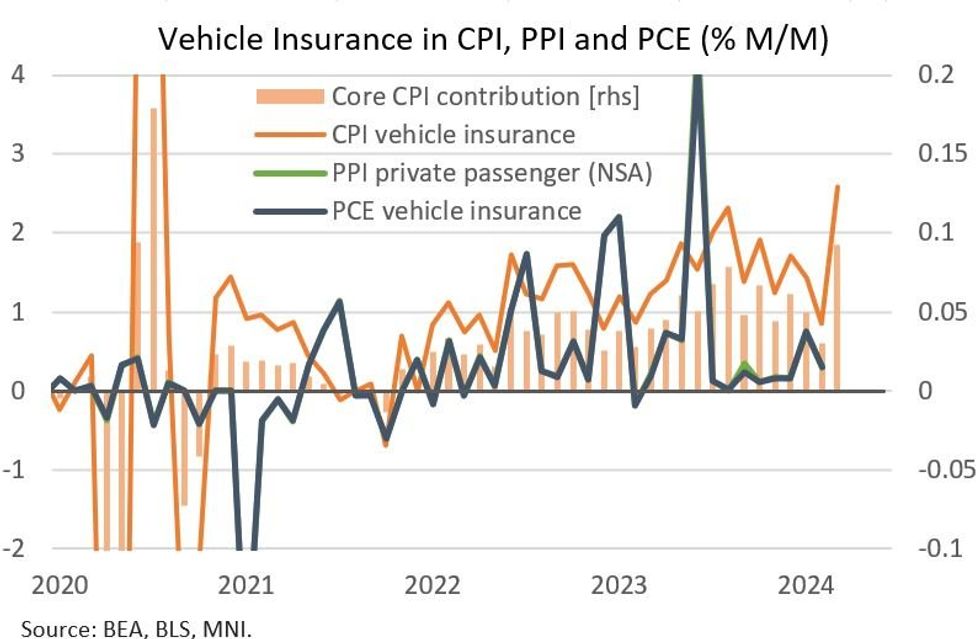

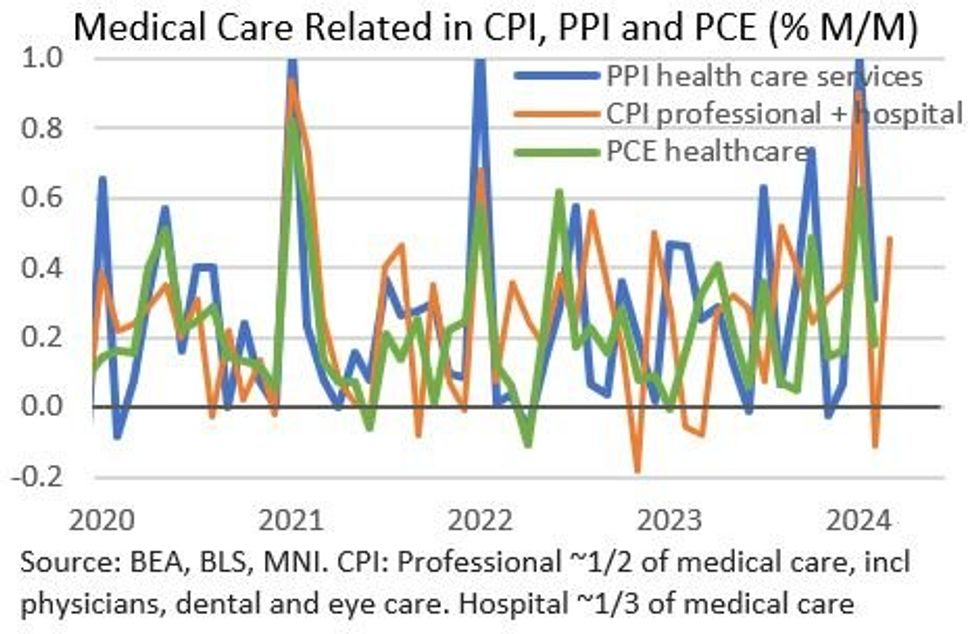

- As we wrote earlier, auto insurance and medical care inflation were arguably the biggest upside surprise factors in the strong core/supercore CPI readings, so it's worth noting that the PCE equivalents might tell a different story. The divergence between the two has been a key theme, with core PCE printing 0.26% in February, with supercore at 0.18% (vs CPI equivalents of 0.36%/0.47%, respectively).

- PCE vehicle insurance has been running much softer than its CPI equivalent, which surprisingly hit a 44-month high in March (+2.58% M/M after +0.85% in Feb), alone adding 0.09pp to core CPI. PCE vehicle insurance rose 0.17% in Jan and 0.15% in Feb.

- The strong CPI healthcare reading, which added 0.05pp to the core M/M reading in March on a 0.56% M/M rise (was -0.05% in Feb), could also look different in the PCE report, which has a very high weighting in core for healthcare services (which rose 0.62% in Jan and 0.18% in Feb).

- This raises the stakes for PPI release Thursday which will include components that translate into healthcare services, airfares, and portfolio management.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok