Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

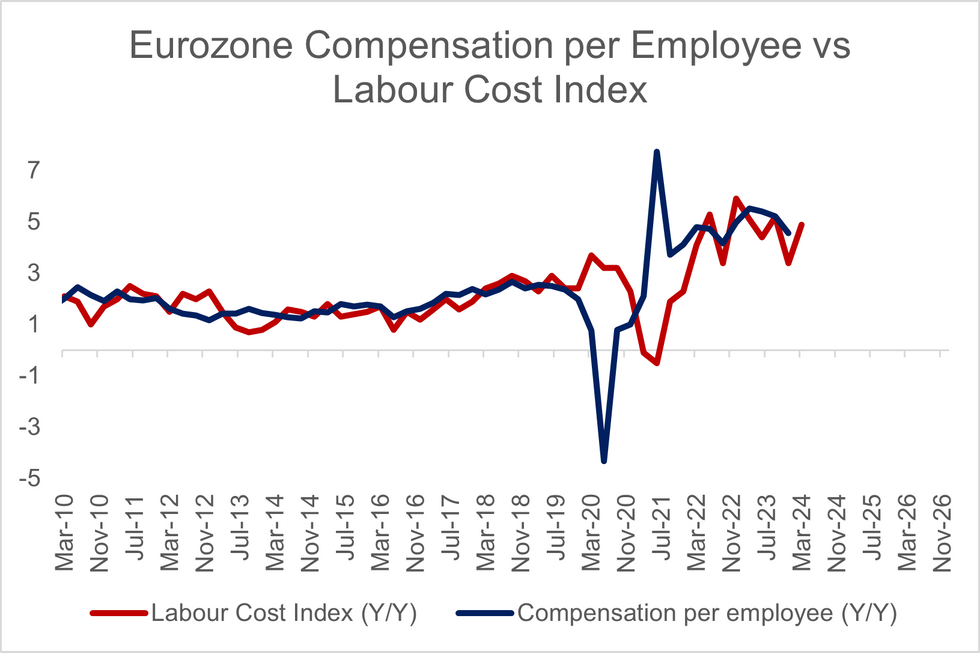

The preliminary estimate of the Eurozone Q1 labour cost index showed growth of 4.9% Y/Y. While there was no consensus for the print, it represents a notable acceleration from the 3.4% Y/Y seen in Q4 2023.

- We will have a better indication of where Q1 compensation per employee (released on June 7 alongside the full EZ national accounts) is headed once Thursday’s negotiated wages data are in hand, but today’s labour cost estimate alone suggests upside risks to overall unit labour costs.

- However, the ECB's March projections assume that still-strong unit labour cost growth will be absorbed by a moderation in unit profits in Q1, enabling GDP deflator growth to soften. As such, today’s data shouldn’t sway the ECB meaningfully towards a particular path for rates after the June meeting.

- But the data creates some tension with other indicators of Q1 wage growth: The Indeed wage tracker has moderated in the last 3 months, and analysts expect Thursday’s ECB negotiated wages tracker to decelerate from 4.5% Y/Y in Q4 2023 (though it is projected to remain above the 4.0% handle).

- The preliminary labour costs release from Eurostat does not contain country level estimates, but the Eurozone-wide industry split indicated a broad-based acceleration.

- Services labour costs accelerated to 5.2% Y/Y (vs 4.0% prior) while industry/construction labour cost growth rose to 5.0% Y/Y (vs 4.1% prior). Note that this makes it a little unclear why overall labour costs didn’t rise by more, given public sector and defence costs also registered 5.0% Y/Y growth in Q1.

- A reminder that we need a deep dive into the mechanics of the GDP deflator and Unit labour costs in March here.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok