Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

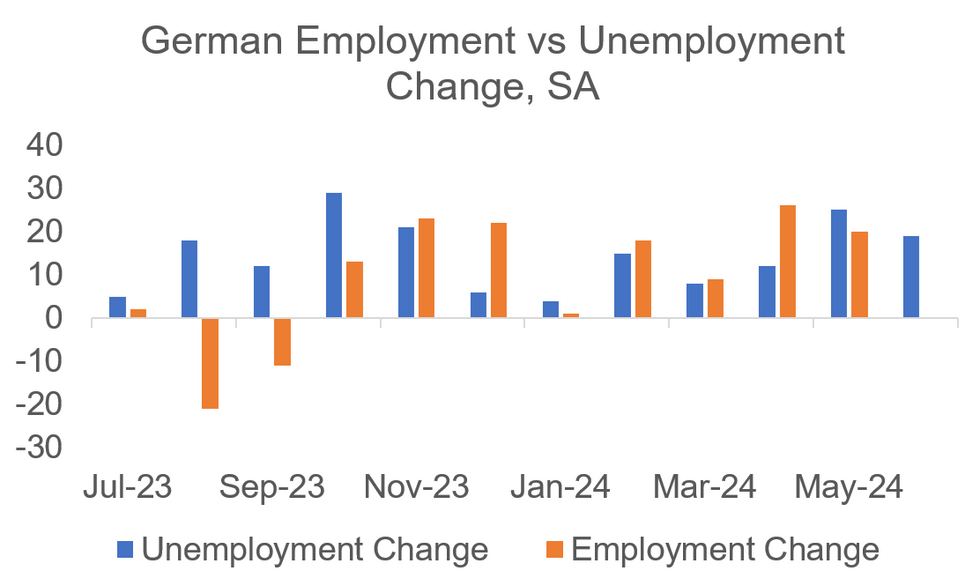

The latest German labour market data has been slightly on the weaker side overall, with rising unemployment and underemployment as well as a fall in labour demand, offset somewhat by a marginal rise in employment.

- Unemployment rose more than expected in June, by 19k (vs 15k cons) but less than in May (25k) on a seasonally-adjusted basis. This nudged the SA unemployment rate up to 6.0% (vs 5.9% cons and prior).

- Employment rose by 20k in May (latest month for which data is available; vs 26k Apr) in a further extension of all-time levels on a seasonally-adjusted basis. Employment gains since the beginning of 2024 continue to be solely driven by part-time employment, according to the German employment agency.

- The expected number of employees impacted by Kurzarbeit (which has to be reported in advance by companies and can be interpreted as an early indicator for future use of state benefits) remained relatively steady in June vs May according to the employment agency (42k June 1-24). Underemployment excl. Kurzarbeit meanwhile continued its slight uptrend on a SA basis, printing 16k higher (around +0.5% M/M vs +0.4% prior).

- Labour demand, reflected by the agency's seasonally-adjusted job index "BA-X", declined by 2 points to 109 in June (-10p vs June 2023; all-time high of 138p in May 2022; the index is normalised to 2015=100 and reflects vacancy levels and activity).

- Looking ahead, forecasts and sentiment indicators suggest that the German labour market will continue to soften slightly. The unemployment rate is expected to increase to up to 6.1% in the coming quarters according to MNI's collation of sellside consensus and the IFO Employment Barometer has printed in contractionary territory for 14 consecutive months.

MNI, Destatis, Bloomberg

MNI, Destatis, Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok