Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

Banking system reserves have risen to the highest level since mid-April at over $3.48T, defying expectations of being run down alongside QT and Treasury cash rebuilding post-debt limit crisis. With their rise of over $400+B since just prior to March’s banking turmoil, we’re probably beginning to approach the limits of how high they can climb given ongoing Fed balance sheet runoff.

- But there is still some room to run to the downside for the overnight reverse repo facility (ON RRP) which has fallen to just above $850B, down $1.4T since June,

- Most analysts’ whose 2024 balance sheet outlooks we have seen suggest that the ON RRP facility will decline to near zero by some time in the 2nd half of next year, with varying splits of that cash going into the Treasury’s coffers vs reserves – and QT running down $900B on an annual basis.

- NatWest sees ON RRP fully drained by Q4 (though not before), with Morgan Stanley suggesting signs of reserve scarcity will remain at bay until mid/late 2024 when the RRP starts approaching zero.

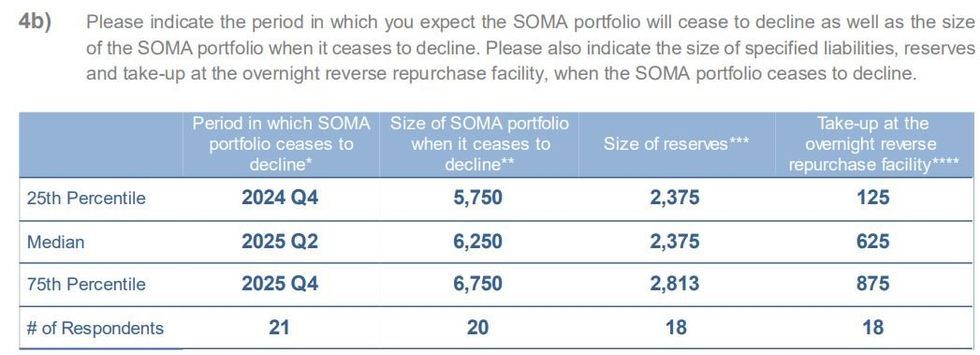

- The latest NY Fed Survey Of Market Participants shows the median respondent expecting QT running to Q2 2025, ending at a size of $6.25trn (vs $7.2T currently), with reserves at $2.375trn and ON RRP takeup at $625bln. Survey results below (from NY Fed:)

- Of course that suggests ON RRP won’t fully be drained. KC Fed researcher Stefan Jacewitz told MNI “a significant balance in ON RRP is probably more likely than something closer to zero at least for next year.”

Source: NY Fed SMP

Source: NY Fed SMP

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok