Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

KRW

1 month USD/KRW has spent most of today's session drifting lower, although some support was evident in the low 1308/high 1307 region. We are now back close to 1310, but for now we are avoiding a test of the 1315/16 zone.

- Onshore equities are modestly higher, with the Kospi up a little over 0.3% at this stage, while the Kosdaq is trailing slightly (+0.28%).

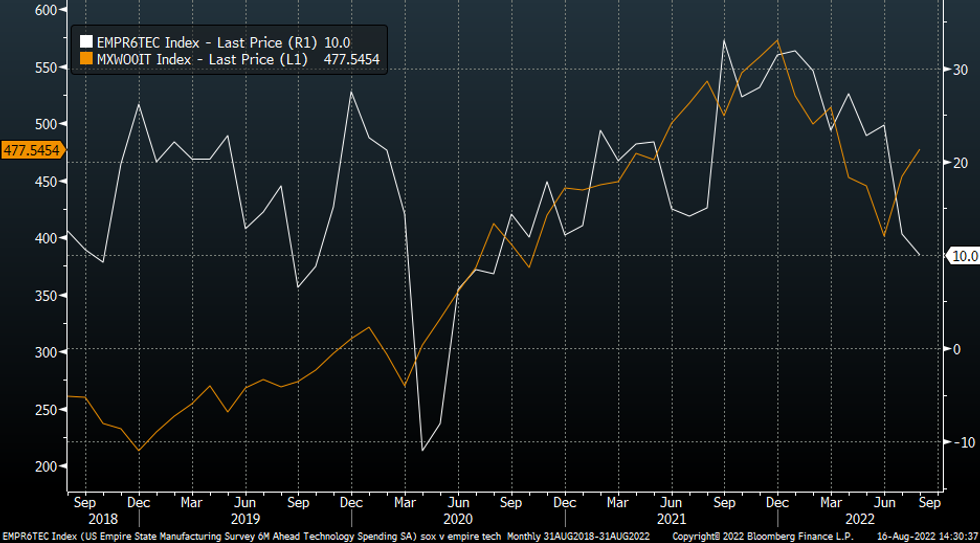

- Overnight the slump in the empire manufacturing survey (-31.3 versus +5.0 expected) cast a fresh cloud over the US/global growth backdrop. Most of the detail of the survey painted a bearish outlook, although one of the sub components of the survey looks at intentions around the tech spending outlook for the next 6 months. This sub-index also fell, but much more modestly, down to +10 from +12 in July.

- The chart below overlays this sub-index against the MSCI IT equity market index. The weakness in the tech spending outlook is a little at odds with the recent rebound in IT equity performance.

Fig 1: Empire Survey Tech Spending Intentions & MSCI IT Equities

Source: MNI/Market News/Bloomberg

Source: MNI/Market News/Bloomberg

- The resilient equity picture should be helping KRW sentiment at the margin. As we highlighted previously there is already a decent wedge between onshore Korean equities and USD/KRW performance. All else equal the won should be stronger based off current equity levels.

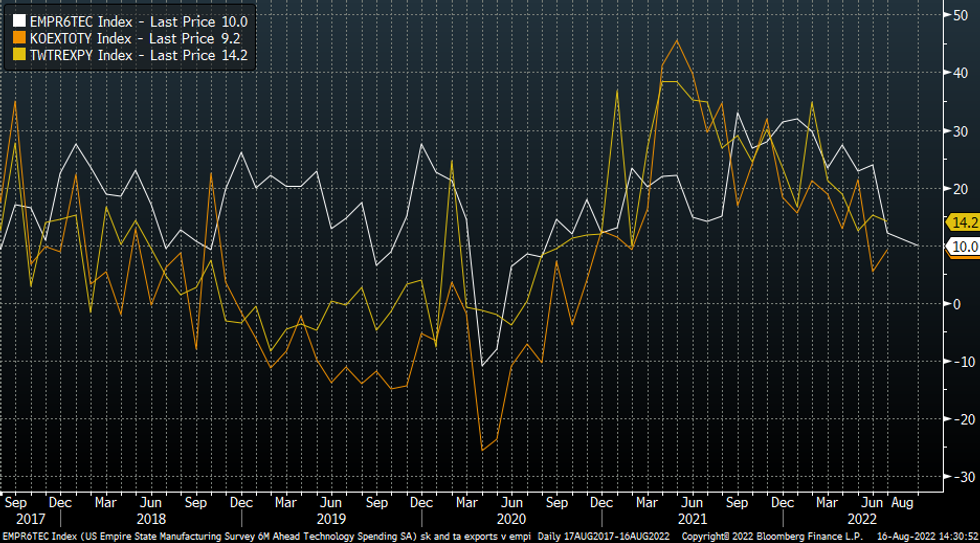

- The other point to note is that the slowing in South Korea export growth is also already reflected to some degree in terms of the tech spending outlook, see the second chart below. This also applies for Taiwan export growth, (which is the yellow line on the chart).

Fig 2: Empire Survey Tech Spending Intentions Versus South Korea & Taiwan Export Growth

Source: MNI/Market News/Bloomberg

Source: MNI/Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok