Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

BONDS

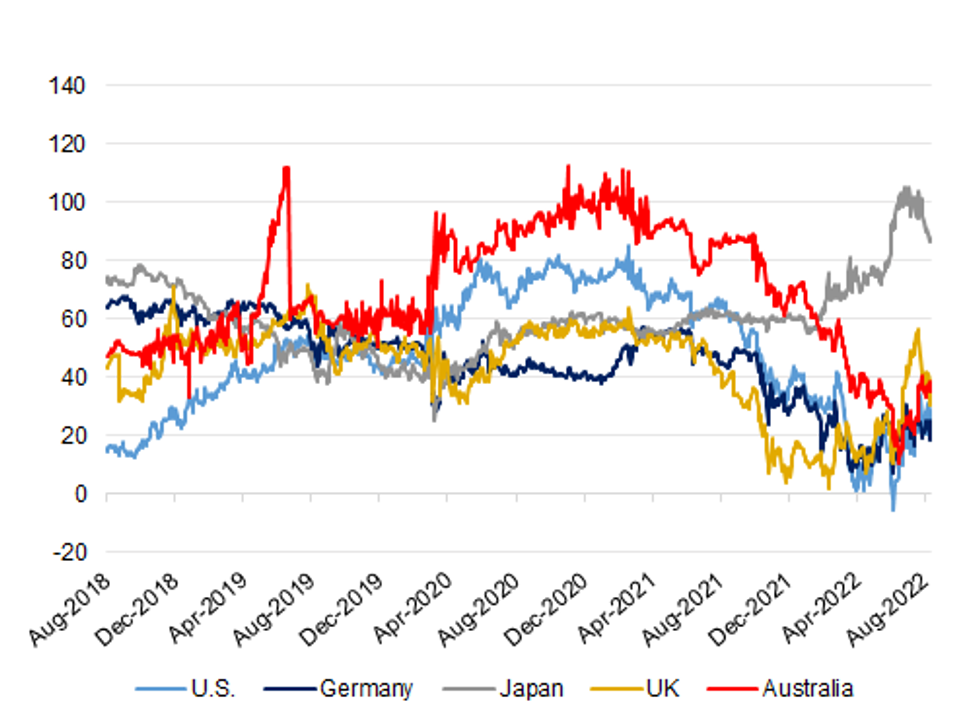

A quick eyeball of the 10-/30-Year yield spreads across some of the major core global FI markets shows that the Japanese 10-/30-Year yield spread has moved away from cycle steeps registered in mid-June, with the rest of the 10-/30-Year yield spreads that we have chosen (U.S., German, UK and Australian) all operating off of their cycle flats, albeit with the UK variant pulling flatter in recent sessions owing to increased stagflationary worry and a related uptick in BoE tightening premium priced into money markets. What are the driving factors for the JGB curve?:

- Increased recession worry centred on the U.S. & Europe, driving yields lower, but the flattening impulse hasn’t been observed in the remaining core FI global markets over the horizon in question, so there must be something else at play.

- Mid-June saw the challenge and ultimately successful defence of the BoJ’s existing YCC parameters with the subsequent insistence that the Bank remains on hold until meaningful underlying inflationary pressures emerge (with a formal easing bias maintained). Foreign investors were the key party in the challenge with subsequent data revealing notable short selling of JGBs by that particular cohort ahead of the Bank’s June meeting as speculation surrounding the potential for a hawkish move stepped up, followed by short covering in the weeks that have followed. The fact that the BoJ has less relative control beyond the 10-Year point of the curve allowed the test of the BoJ to be amplified by a steepening of the curve, with flows in swaps also noted at the time of the challenge. The recent short covering could have aided the flattening in question.

- Another idiosyncratic factor has been the willingness of domestic life insurers to deploy capital in the longer end of the JGB curve (as alluded to in their semi-annual investment interviews), with pension funds and lifers shedding a record amount of foreign bonds in the month of July (per JSDA data), as Japan experienced deployed a record stretch of weekly net sales of foreign paper, owing to market volatility and elevated FX-hedging costs. That trend has started to turn recently, with Japan registering purchases of foreign bonds in each of the last 4 weeks (albeit in relatively limited terms when compared to the net sales that came before).

- The previous steepness of the curve, in both a domestic and international sense, added to aforementioned demand from the domestic lifer and pension community, who have likely been the min driver of the recent curve flattening.

Fig. 1: U.S., German, Japanese, UK & Australian 10-/30-Year Yield Curves (bp)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok