Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US

Overall, the macro impact from the debt limit bill looks limited, apart from relieving uncertainty over the prospect of a near-term US debt default.

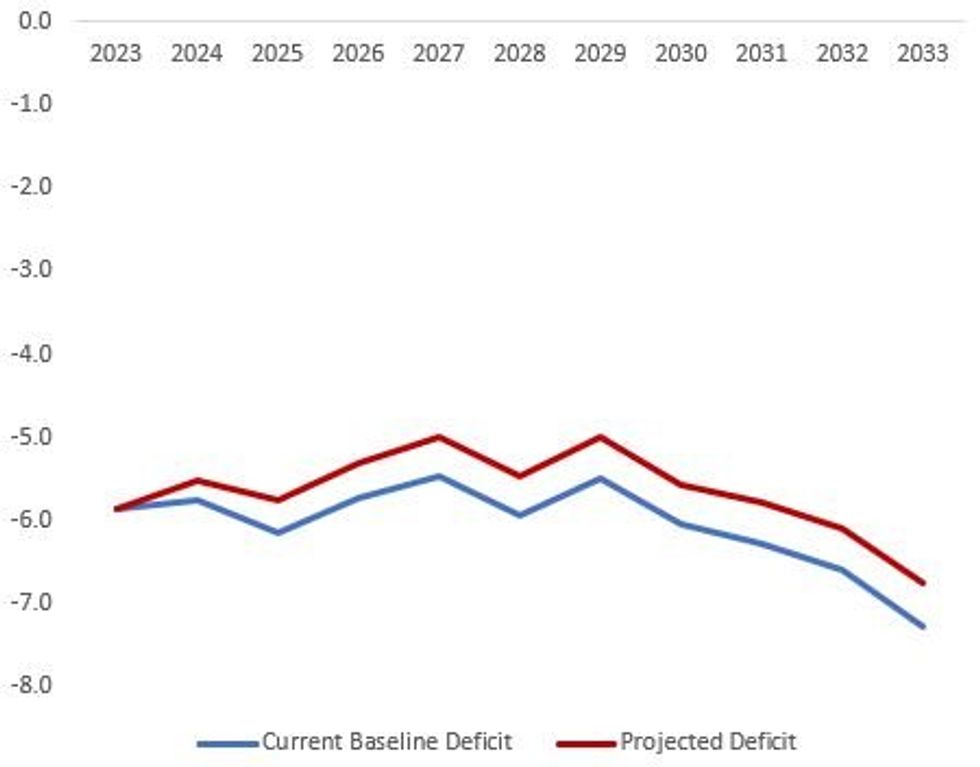

- The GDP equivalent deficit reduction in 2024 will be on the order of 0.2-0.3% of GDP lower vs baseline, growing slightly over the next decade in part due to lower implied debt servicing costs - see chart.

- To put that in context - over a decade, the cumulative deficit reduction in nominal dollars of $1.5T compares to nominal cumulative GDP projected at $332T, so about 0.45% GDP, and the 2023 deficit estimated at 5.9% of GDP.

- Another basis of comparison is the 2011 debt limit agreement which reduced deficits by $2T - that led to a projected 0.7% of GDP deficit reduction in 2012.

- They key macro impact of the deal in the short term is likely to come from the deal's cementing the end of federal student loan forbearance by Aug 30. This has no impact on the fiscal deficit projections because it had already been assumed by the CBO, and student debt relief had probably been likely to end by the fall anyway.

- But the end of forbearance will drag on consumer spending via a reduction in disposable personal income by a mostly high-spending-propensity demographic. There could be a sudden impact as well in September as debt repayments start back up (we've seen estimates of the average monthly forbearance at $250-400 per month per impacted borrower).

- For example: JPM estimates the spending reduction impact at 0.1% of GDP, though GDP could be hit at 0.25-0.5% quarterly annualized in a short period of time.

Annual Deficits As % of GDPSource: CBO, MNI

Annual Deficits As % of GDPSource: CBO, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok