Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

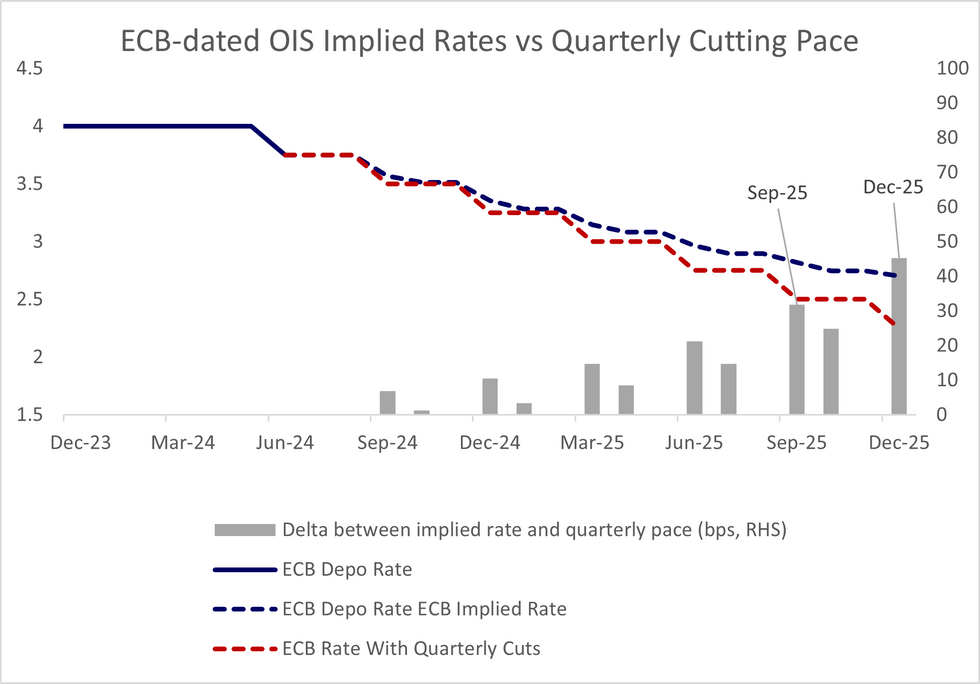

ECB-dated OIS currently price just over 100bps of cuts through the end of 2025, implying a deposit rate of 2.70% through the December ’25 meeting. The current implied market path is broadly consistent with quarterly cuts in H2 2024 (i.e in September and December) but not in 2025.

- The deposit rate would reach 2.25% were the ECB to deliver 25bp cuts at each of the next six quarterly projection meetings. Such a path would align with the dovish contingent of analyst rate forecasts we have seen.

- We think current market pricing appears reasonable at this stage. Concerns around sticky wage-driven services inflation, fiscal policy pressures and a rising neutral rate of interest warrant a wedge between the “quarterly cut” path and current pricing.

- Markets should also remain cognizant of the risk that the ECB chooses to hold rates at one of the September or December meetings.

- Uncertainty around the Fed's rate path and unfavourable developments in core inflation/labour cost outcomes could be enough for some of the Governing Council to err on the side of caution in easing policy this year.

- However, those expecting the ECB to follow through with consistent quarterly cuts through 2025 - as headline inflation returns to the 2% target in line with the June projections - may find value in the September ’25 and December ’25 OIS contracts (See chart).

Source: MNI, Bloomberg

Source: MNI, Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok