Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

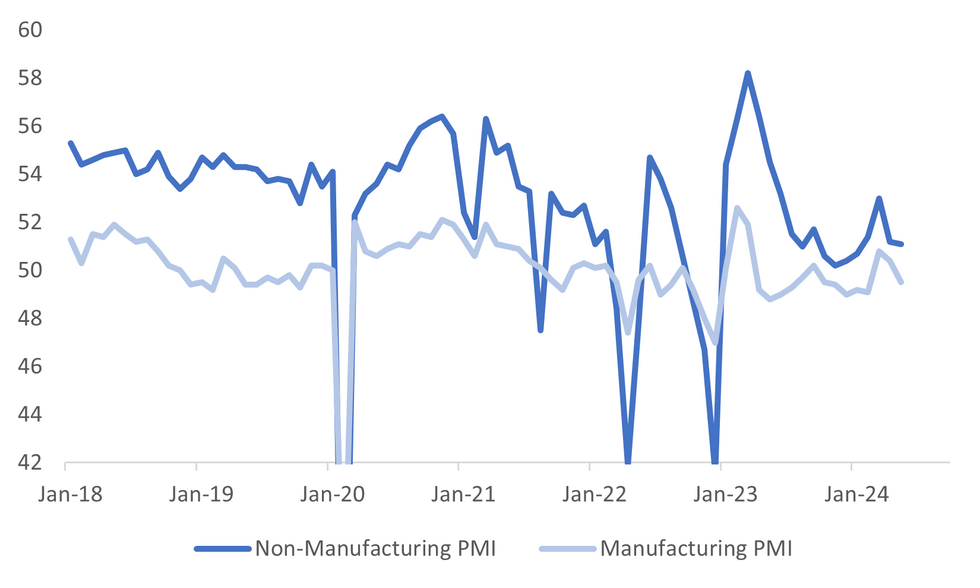

The official PMIs were weaker than expected. Manufacturing slipped back into contraction territory, printing at 49.5, versus 50.5 forecast. This ends the 2 month run of above 50.0 prints. The services or non-manufacturing PMI printed at 51.1, against a forecast of 51.5 and a prior outcome of 51.2. The composite PMI printed at 51.0, versus 51.7 in April.

- For the manufacturing PMI, we saw weakness in new orders, the headline falling to 49.6 (51.1 prior). New orders to orders eased slightly but remains elevated by recent standards. New export orders fell to 48.3 form 50.6. Output was 50.8 from 52.9 in April, while imports fell to 46.8 from 48.1.

- The employment sub index was steady near 48.0, while input and output price measures both rose. Input prices to 56.9 from 54.0, output prices to 50.4 (49.1 prior).

- On the services side, the detail was mostly softer. New orders rose but only to 46.9. Input and selling prices both eased. Both these measures are back sub the 50.0 expansion/contraction point. Employment also fell further to 46.2 (from 47.2).

- The data is disappointing in the sense the manufacturing/industrial side had been showing more positive trends compared to other parts of the China economy. It will see on-going calls for policy support maintained.

Fig 1: China PMIs Soften In May

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok