Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: Strong Rebound Yld Curves

Yield curves bounced, making new session highs (5s30s 151.036) latter half of Monday trade as duration selling in long end extends new session lows in bonds. Levels nowhere near Thursday's post 7Y auction indigestion when 30YY hit 2.3944% high (currently 2.2183%) levels closer to Fri's midrange.

- Technicals: TYM currently 133-05 +14/32 vs. 133-00 low, well above first support of 132-08, second support 131-31 Feb 25 Low and bear trigger.

- Early support in rates evaporated in lead up to early data (Jan const spend +1.7%; ISM Feb Mfg PMI 60.8 vs Jan 58.7) extended duration sale on release, better selling in 10s-30s with some prop, real$ and central bank selling in 10s-30s floowed, misc acct selling 5s-7s.

- Tsys jump-bid on Fed Gov Brainard comments, notably: BRAINARD: VALUATIONS ELEVATED IN A NUMBER OF ASSET CLASSES, Bbg, fast$ and algo-driven buying.

- Decent pick-up in swappable corporate issuance: $23.55B To Price Monday, $7B GS 6pt jumbo adds to $5.5B issued on Jan 20. Deal-tied paying evident in 10s-30s, payers in 20s second half.

- Sporadic real$ and central bank selling in 10s-30s after better selling from same in first half, generally cautious positioning as new month gets underway and Feb employment this Friday.

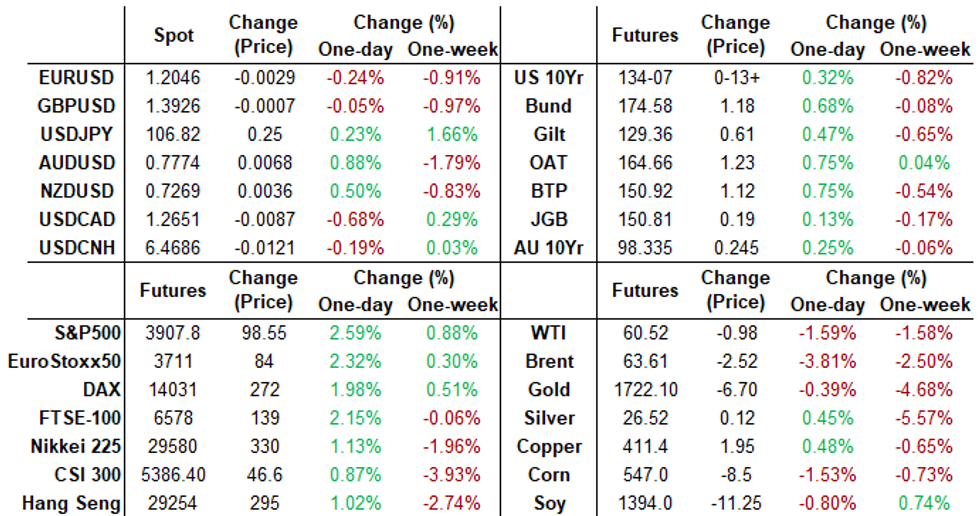

- The 2-Yr yield is down 0.4bps at 0.123%, 5-Yr is down 1.6bps at 0.7153%, 10-Yr is up 4.5bps at 1.4496%, and 30-Yr is up 7.5bps at 2.2266%.

US TSY: Short Term Rates

US DOLLAR LIBOR: Latest settles:

- O/N -0.00450 at 0.07950% (+0.00587 net last wk)

- 1 Month -0.00925 to 0.10925% (+0.00305 net last wk)

- 3 Month -0.00413 to 0.18425% (+0.01313 net last wk) ** (Record Low of 0.17525% on 2/19/21)

- 6 Month -0.00250 to 0.20050% (+0.00700 net last wk)

- 1 Year -0.00012 to 0.28363% (-0.00275 net last wk)

- Daily Effective Fed Funds Rate: 0.07% volume: $71B

- Daily Overnight Bank Funding Rate: 0.07%, volume: $208B

- Secured Overnight Financing Rate (SOFR): 0.01%, $889B

- Broad General Collateral Rate (BGCR): 0.01%, $367B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $336B

- (rate, volume levels reflect prior session)

- TIPS 1Y-7.5Y, $2.399B accepted vs. $4.080B submission

- Next scheduled purchases:

- Tue 3/2 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Wed 3/3 1100-1120ET: Tsy 4.5Y-7Y, appr $6.025B

- Thu 3/4 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Fri 3/5 1100-1120ET: Tsy 2.25Y-4.5Y, appr $8.825B

EURODOLLAR/TREASURY OPTIONS: Summary

Eurodollar Options:- -10,000 short Sep 96/97 put spds, 4.0

- -7,500 short Sep 95 puts, 3.5

- +5,000 Blue Jul 81/85 put spds 5.5 over 88/91 call spds.

- +5,000 Blue Apr 92 calls, 1.0

- +10,000 Red Sep 95 puts, 10.0 vs. 99.68/0.32%

- -5,000 Green Jun 90 puts, 4.5 vs. 99.37/0.20%

- -2,000 Blue Jun 92 calls 0.5 over the 77/78/782 put tree vs. 99.92/0.20%

- Block, -13,750 short Dec 93/95 put spds, 3.0 vs. 99.57/0.11%

- -7,000 short Dec 93/95 put spds, 3.0 vs. 99.575/0.11%

- 3,300 Green Dec 95 calls, 3.5

- Overnight trade

- Block +14,000 Blue Jul 81/85 put spds 5.0 over 88/91 call spds, 13.5 at 0618-0638ET

- Blocks, total 15,000 Blue Jun 81/83 put spds vs. 98.68/0.10% from 0558ET-0605ET, another 6k on screen

- +11,000 short Dec 93/95 put spds, 3.0

- +13,000 Blue Apr 81/83 put spds, 3.5

- +10,000 Blue Jun/Blue Sep 93/96 1x2 call spd strip, 1-leg over on both, 2.0 total

- 3,000 Blue Mar 91 calls

- +10,000 Green Sep 93/95 1x2 call spds vs. Green Sep 91/92 put spds

- +12,000 TYM 135/136/137 call trees, 4

- -2,500 TYJ 135 calls, 5

- -1,000 TYM 133/133.5 strangles, 221

- -28,000 TYK 129.5/135.5 combo, put over sale from +2 to -1

- +10,000 FVJ 125 calls, 8 vs. 124-12

- +4,000 TYM 136/137/138 call trees, 1-2

- -20,000 FVM 124.5/124.75 call spds 8.5

- -9,000 TYJ 133.5/TYK 132 put spds, 16 (Apr over) adds to block

- Block, -20,000 TYJ 133.5/TYK 132 put spds, 16 at 0827:30ET

- Overnight trade

- +3,000 USJ 155/156/157/158 put condors, 6

- +2,500 TYJ 132/133 put spds 0.0 over TYJ 134.25 calls

- -2,000 FVJ 122.5/125.25 put over risk reversals, 0.5 vs. 124-10/0.20%

BONDS/EGBs-GILTS CASH CLOSE: More Dovish ECB Talk Boosts Big Rally

Monday's session saw a big rally across the space, with 10-Yr Bunds and BTPs dropping most since June 2020, and Gilts underperforming though also stronger.

- An early rally unwinding some of last week's losses gained momentum in the afternoon on comments by ECB's Villeroy that the bank "can and must react" against "unwarranted" tightening of financial conditions. This follows last week's dovish comments by Lagarde, Schnabel, Lane.

- Bunds briefly dipped on ECB data showing a slowdown in asset purchases (vs expectations that the ECB picked up the pace during last week's bond sell-off), but an ECB spokesperson was on the wires to explain this was due to large redemptions.

- Markets largely ignored in-line/above consensus Italy and Spain Feb PMIs, and higher-than-expected German and Italian inflation.

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is down 2.4bps at -0.687%, 5-Yr is down 6.1bps at -0.629%, 10-Yr is down 7.4bps at -0.334%, and 30-Yr is down 5bps at 0.144%.

- UK: The 2-Yr yield is down 2.9bps at 0.099%, 5-Yr is down 4.7bps at 0.353%, 10-Yr is down 6.1bps at 0.759%, and 30-Yr is down 5.2bps at 1.334%.

- Italian BTP spread down 2.9bps at 99.2bps /Spanish spread down 2.5bps at 65.8bps

OPTIONS/EUROPE SUMMARY: Red And Green Stg Mids

Monday's options flow included:

- DUJ1 112.10/20/30 call fly bought for 2 in 7.25k

- DUK1 112.10/20/30 call fly bought for 1.5 in 4k

- DUK1 112.20/30/40/50 call condor bought for 1.75 in 5k

- OEM1 135.00^ sold at 89 in 1k

- RXJ1 170.5/172 RR, bough the call for 1 in 10k

- 0RZ1 100.62/100.5ps 1x2, bought the 2 for 2 in 5k

- LZ1 99.875/100.00 call spread bought for 5.5 in 6k

- 0LM1 99.75/99.62/99.50p fly, trades for 2 in 9k

- 0LU1 99.62/99.50ps, bought for 3.5 in 7.5k

- 0LU1 99.87/99.75ps 1x2, bought the 2 for up to 6.25 in 10k

- 2LJ1 99.50p, sold at 9 in 5k

- 2LM1 99.50/99.25/99.125/98.875 broken put condor sold at 5 in 11k

- 2LU1 99.50/99.25/99.12/98.87p condor, sold at 5.5 in 4

- 2LU1 99.50/99.00ps, sold at 14.25 in 5k

- 2LU1 99.25/99.00/98.87 with 2LZ1 99.25/99.00/98.87p ladder strip, bought for 4.5 in 2.5k

- 3LU1 99.37/99.12ps, sold at 12 in 3k

FOREX: Havens Offered as Risk Sentiment Repairs

Following the sharp equity sell-off in the second half of last week, markets stabilised slightly on Monday, with gains of over 2% apiece for the main three US indices. This translated to haven FX being offered throughout the Monday session, prompting JPY and CHF to underperform all others in G10.

- At the other end of the table, Antipodean and commodity-tied currencies benefited from the bounce in the reflation trade and oil & metals prices. AUD/USD has now bounced close to 80 pips off the recent lows, but still remains shy of the cycle highs printed mid-last week.

- US data was largely ineffectual, despite February's US Manufacturing ISM beating expectations. Prices paid drew particular focus, surging to new cycle highs of 86.0 vs. Exp. 80.0 - the highest since 2008.

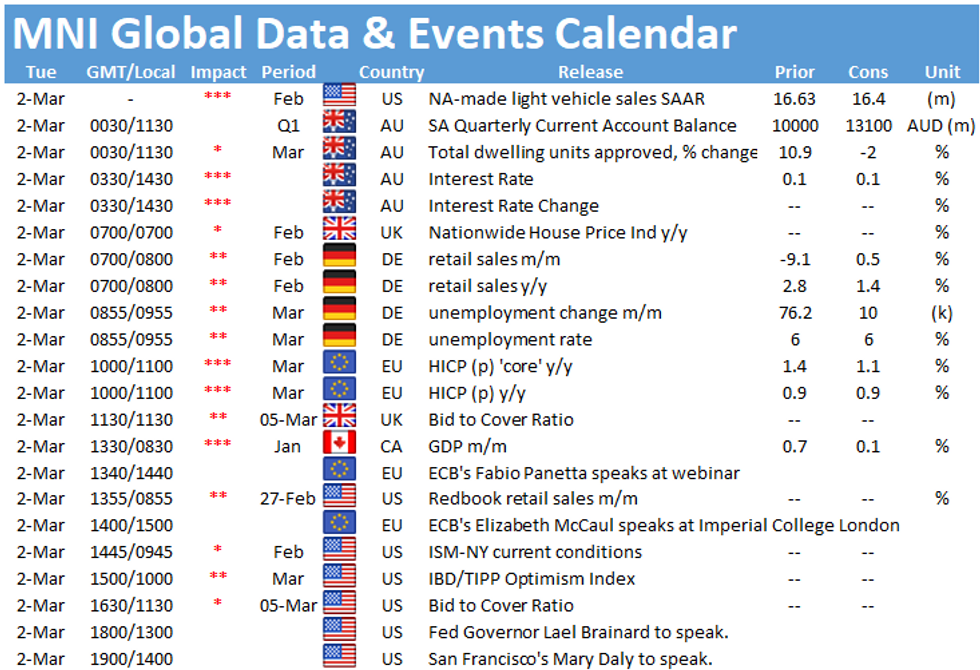

- Focus Tuesday turns to the RBA rate decision, German retail sales, prelim Eurozone CPI numbers and Canadian GDP. Fedspeak continues ahead of the blackout period at the end of this week, with Brainard and Daly both on tomorrow's docket.

FX OPTIONS: Expiries for Mar 02 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1900-20(E843mln), $1.2045-65(E1.3bln), $1.2085-90(E523mln)

- USD/JPY: Y105.75-80($1.0bln), Y105.90-10($1.7bln), Y106.30-50($1.2bln), Y107.50($600mln)

- EUR/GBP: Gbp0.8630-35(E540mln)

- AUD/USD: $0.7875(A$589mln)

- AUD/NZD: N$1.0670(A$722mln)

- USD/CNY: Cny6.4500($588mln), Cny6.4645($833mln)

PIPELINE: $7B Goldman Sachs 6Pt Jumbo Leads

$7B GS 6pt jumbo adds to $5.5B issued on Jan 20 ($2.25B 2NC1 +35, $750M 2NC1 FRN SOFR+41, $2.5B 11NC10 fix/FRN +90),

- Date $MM Issuer (Priced *, Launch #)

- 03/01 $7B #Goldman Sachs $700M 2NC1 +40, $450M 2NC1 FRN SOFR+43, $1.75B 3NC2 +55, $700M 3NC2 FRN SOFR+58, $3B 6NC5 +73, $400M 6NC5 FRN SOFRT+81

- 03/01 $4.3B #Cigna $500M 3NC1 +35, $800M 5Y +55, $1.5B 10Y +95, $1.5B 30Y +120

- 03/01 $2.5B #Coca-Cola $750M 7Y +45, $750M 10Y +60, $1B 30Y +85

- 03/01 $2.15B #Keurig Dr Pepper Inc $1.15B 3NC1 +48, $500M 10Y +83, $500M 30Y +113

- 03/01 $1.9B #John Deere $600M 2Y +15, $800M 3Y +22, $500M 7Y +45

- 03/01 $1.5B #Roche $500M 3Y +20, $350M 3Y FRN SOFR+24, $650M 5Y +30

- 03/01 $1.5B #Toronto-Dominion Bank 3Y +32, 3Y FRN SOFR+35.5

- 03/01 $800M #Graphics Packaging Int $400M 3Y +55, $400M 5Y +80

- 03/01 $700M #PPG Ind 5Y +60

- 03/01 $600M *Estee Lauder 10Y +57

- 03/01 $600M #Fairfax Fnvl Holdings 10Y +195

EQUITIES: Stocks Bounce, But Still Off Last Week's Best

Equity markets across both Europe and the US traded well Monday, with continental indices rising close to 2%, while US bourses modestly outperformed. The S&P 500 traded with gains of close to 2.3%, while the tech-heavy NASDAQ rose over 2.5% at some points of the session.

- Markets are bouncing off last week's lowest levels and, despite Monday's decent gains, are still well off recent highs. Whether the bounce can be sustained remains a key sticking point, with firm resistance expected ahead of 3950 in the e-mini S&P.

- Across the US, energy names benefited from the stabilisation of oil and gas prices to lead Monday's rise, while defensive healthcare and consumer staples still rose, but were close to the bottom of the Monday table.

- Stabilisation in equity prices led to a lower VIX, with the index shedding close to 5 points and back below 25.

COMMODITIES: Late Pressure In Oil Sparks An Otherwise Muted Session

- WTI futures have come under some late pressure, dipping back beneath $60 as markets anticipate the looming Opec plus easing of cuts and retrace prior reflationary optimism. The continuation of last week's late sell-off has prompted some momentum selling through Feb 23rd lows and currently trades down over 2%.

- Precious metals exhibited less pronounced, but similarly heavy price action. Despite the majority of the session lacking any momentum, spot gold and silver have lost ~0.65%, bringing some late relief demand for the Bloomberg Dollar Index, trading back towards flat on the session.

- Copper futures also pared gains from the open to approach Friday's lows under 410.

- Bitcoin gained ~6% amid headlines that Goldman Sachs Inc has restarted its cryptocurrency trading desk. Price firmed to trade back above $48,000.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.