Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: Heavy Two-Way After ADP Miss

Tsy futures traded weaker all session but were off late morning lows after the closing bell, bonds holding a narrow range last couple hours while equities tripped lower on the back of optimistic Fed Beige Book assessment:- ECONOMY EXPANDED MODESTLY FOR MOST DISTRICTS TO MID-FEB; MOST BUSINESSES OPTIMISTIC FOR NEXT 6-12 MONTHS ON VACCINE, Bbg

- Tsys sold off early appr 15 minutes BEFORE weaker than est ADP +117k vs. +205k. likely knock-on selling tied to Sunak or Onto on UK budget or Corp taxes. Yield curves, particularly in the short end) continue to move steeper: 5s30s tapped 155.532 overnight compared to last Thu's 166.984 level last seen Aug 2014.

- Building inflation expectations and improving growth spurring heavy consolidation tone since last week. Wide range of estimates for this Fri's Feb NFP employ data +60k to +410k, 205k mean est.

- Sources reported two-way from prop and fast$ in shorts to intermediates, rate paying in 5s-10, real$ and bank selling out the curves.

- Technicals: Treasuries are still trading within the body of price action from Feb 25. In candle terms the pattern on this day is a bearish standard line - a continuation pattern. TYM focus on 131-31, Feb 25 low. Key S/T resistance is at 134-06+, the Feb 25 high.

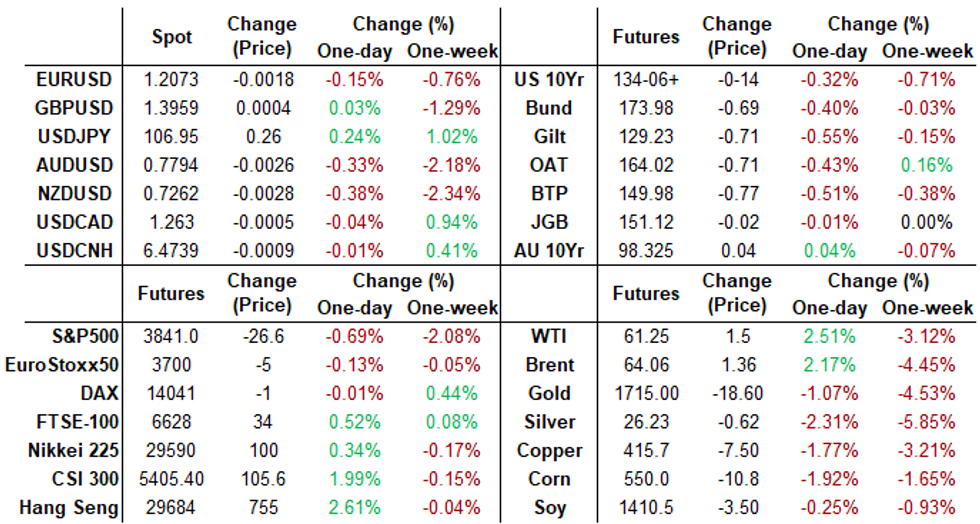

- The 2-Yr yield is up 1.8bps at 0.1388%, 5-Yr is up 6.3bps at 0.722%, 10-Yr is up 7.2bps at 1.4635%, and 30-Yr is up 5.5bps at 2.2462%.

US TSY: Short Term Rates

US DOLLAR LIBOR: Latest settles:

- O/N -0.00038 at 0.07850% (-0.00550/wk)

- 1 Month -0.00538 to 0.10300% (-0.01550/wk)

- 3 Month +0.01037 to 0.19375% (+0.00537/wk) ** (Record Low of 0.17525% on 2/19/21)

- 6 Month +0.00425 to 0.21100% (+0.00800/wk)

- 1 Year +0.00300 to 0.28200% (-0.00175/wk)

- Daily Effective Fed Funds Rate: 0.07% volume: $68B

- Daily Overnight Bank Funding Rate: 0.07%, volume: $204B

- Secured Overnight Financing Rate (SOFR): 0.04%, $951B

- Broad General Collateral Rate (BGCR): 0.02%, $390B

- Tri-Party General Collateral Rate (TGCR): 0.02%, $349B

- (rate, volume levels reflect prior session)

- Tsy 4.5Y-7Y, $6.001B accepted vs. $16.880B submission

- Next scheduled purchases:

- Thu 3/4 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Fri 3/5 1100-1120ET: Tsy 2.25Y-4.5Y, appr $8.825B

EURODOLLAR/TREASURY OPTIONS:

Eurodollar Options:- +5,000 Blue Jun 87/90 1x2 call spds 3.0

- Update 6,600 Blue Dec 93 calls, 2.5

- +4,000 short Jun 99.56/99.62 put spds, 0.5

- +5,000 Red Dec'22 92 puts, 8.5

- -5,000 short Sep 96/97 put spds, 4.0 adds to block

- Block, -20,000 short Sep 96/97 put spds, 4.0 vs. 0916:17

- 8,800 Blue Mar 91/92 put spds

- -2,000 Green Sep 91 straddles, 35.5

- +2,500 Green Dec 96 calls 1.5

- 1,500 short Jul 95/96/97 2x3x1 put flys

- Overnight trade

- Green Jun put trade outright and on spd

- >13,000 Green Jun 91 puts

- >23,600 Green Jun 92 puts

- >9,300 Green Jun 93 puts

- 2,500 Green Apr and Green May 92/93/95 put flys

- 8,400 short Sep 93/95/98/100 call condors

Treasury Options:

- +8,000 TYJ 134.5 calls, 10 vs. 133-01

- >4,100 TYK 134/135.5 call spds, 24 screen

- +5,000 TYK 133/133.5/134 call flys, 3.0

- Block, -20,000 TYJ 133.25/133.5 1x2 put spds, 58 vs. 133-06/0.75% at 0848:39ET

- +2,700 TYM 131/135 strangles from 60-64

- Overnight trade

- 2,700 FVM 120.5/122.5 put spds

- 5,000 FVJ 124.25 puts, 15.5 last

- Block +30,000 TYJ 133/133.5 put spds, 13

- Block, -5,500 TYJ 133.5/TYK 131.5 put spds, 16 ongoing, adds to appr -30k Mon

FOREX: Markets Contained Despite Poor US Data

The single currency gave up early gains, settling lower against against the greenback despite Bloomberg reports citing sources in saying the ECB see no need for drastic action government bond yields at these levels. EUR/USD showed above 1.21 in the initial reaction, but faded swiftly into the London close.

- The greenback generally traded well, with the USD index in minor positive territory - but yesterday's highs contained, providing markets with few new directional signals.

- Both the ISM Services Index and ADP Employment Change came in slightly below forecast, heightening focus on Friday's jobs report, in which markets expect 200k jobs to have been added across the month.

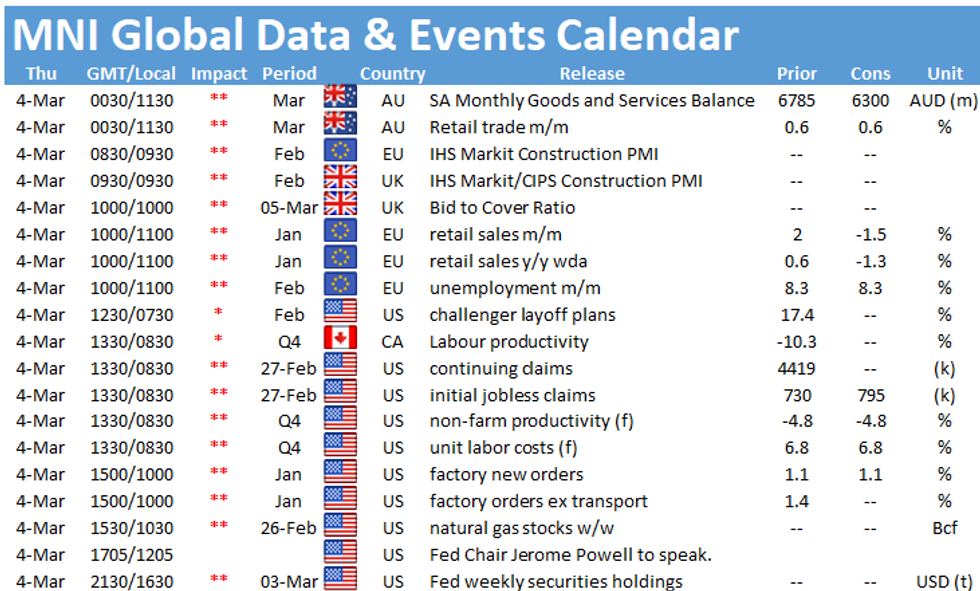

- Focus Thursday turns to weekly US jobless claims & factory orders and Australian trade balance for January. Central bank speak again takes focus, with RBA's Kearns, ECB's Knot & Centeno and Fed Chair Powell.

FX OPTIONS: Expiries for Mar04 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1890-10(E1.2bln), $1.2000-05(E739mln), $1.2075(E518mln), $1.2085-00(E1.2bln)

- USD/JPY: Y105.45-50($582mln), Y105.60-75($1.6bln), Y106.30-50($1.0bln)

- GBP/USD: $1.3900(Gbp550mln), $1.4090-00(Gbp708mln)

- AUD/USD: $0.7700(A$614mln), $0.7750(A$779mln), $0.7800(A$994mln), $0.7800(A$994mln), $0.7820-25(A$1.4bln-AUD puts), $0.7900(A$885mln)

- USD/CNY: Cny6.45($745mln)

PIPELINE: $4B Peru 3Pt Leads; Swedish Export Rolled to Thursday

- Date $MM Issuer (Priced *, Launch #)

- 03/03 $4B #Peru $1.75 2031-tap +125, $1.25 20Y +140, $1B 30Y +145

- 03/03 $2B #Barclays $1B 11NC10 +120, $1B 21NC20 +170

- 03/03 $1.6B #Vontier $500M 5Y +110, $500M 7Y +130, $600M 10Y +150

- 03/03 $1.1B #Marriott Int 10Y +140

- 03/03 $1B *Kommunivest WNG 3Y +1

- 03/03 $850 #Agilent 10Y +85

- 03/03 $750M #Equitable Financial Life 7Y +70

- 03/03 $700M #Omega Healthcare 12Y +185

- 03/03 $600M #Corp Office Properties 10Y +140

- Rolled to Thursday

- 03/04 $1B Swedish Export 3Y +6a

EQUITIES: Stocks Edge Off Solid Start

The e-mini S&P held the bulk of the late Tuesday gains throughout the European morning, but equities were sold in US hours to push prices through yesterday's low. Price action was muted, however, with markets taking little cue from the poorer-than-expected ISM Services and ADP Employment change data.

- Utilities and tech names led the declines, with energy and financials holding higher.

- The VIX index saw some supported as equities ebbed lower, but remains well inside the recent range.

- In Europe, performance was more positive, with mainland indices registering gains of 0.1-0.9%. Laggards were peripheral European indices including Italy and Spain, after BBG reported that the ECB see no need to take drastic action on yields at current levels.

COMMODITIES: Oil Surges After Record Drop In Domestic Fuel Inventories

- U.S. gasoline inventories collapsed last week by the most since 1990 after the Texas freeze erased over 5 million barrels/day of refining capacity in late Feb, according to EIA data. Crude stockpiles swelled with refineries still shut.

- Markets expected volatility in the data following the weather, however, the massive product draw more than offset the record crude build. WTI crude futures dipped on the data to $60.22 before quickly erasing the losses and rallying throughout the latter part of the session to a high just shy of $62, residing up 3.25% on the day.

- Additional tailwinds from OPEC+ headlines, where no recommendation was made on output. Some member states appear to be pushing for a higher level of easing of the cuts, while others are being more cautious. The talks will continue tomorrow.

- Higher yields and a slightly firmer US dollar weighed on metals, with spot gold (-1.28%) and silver (-1.85%) continuing their short-term downward bias that commenced in late February. Gold now eyes support at the 61.8% retracement of the Mar - Aug 2020 rally at $1689.90. Copper futures also struggled, losing 1.67%

- Bitcoin soared back above the $50,000 mark and is currently up 8.5% as markets continue to digest Goldman Sachs relaunching their crypto-currency trading operations.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok