Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY

Bonds lead Tsys higher after a muted overnight session, strong support topping out around noon with markets trading sideways into the closing bell. No data to trade off of and no revelations from the Fed speakers on tap -- all-in-all a quiet start to the week on light volume (TYU1 only 870k by the closing bell).- First-half support was not deemed headline driven -- more positioning related, trading desks said as 10YYmoving back near last week's level of 1.475-1.50% before climbing to 1.54% on Friday.

- Muted trade from sidelined desks ahead Fri's headline June NFP (+700k est vs.

- +559k prior). Modest deal-tied selling on supra-sovereign issuance, light option related flow as well.

- Other potential drivers adding impetus to the bid in rates: doubts over getting the infrastructure deal and month-end extensions (MBS climbed to 0.17 from 0.11 on prelim read).

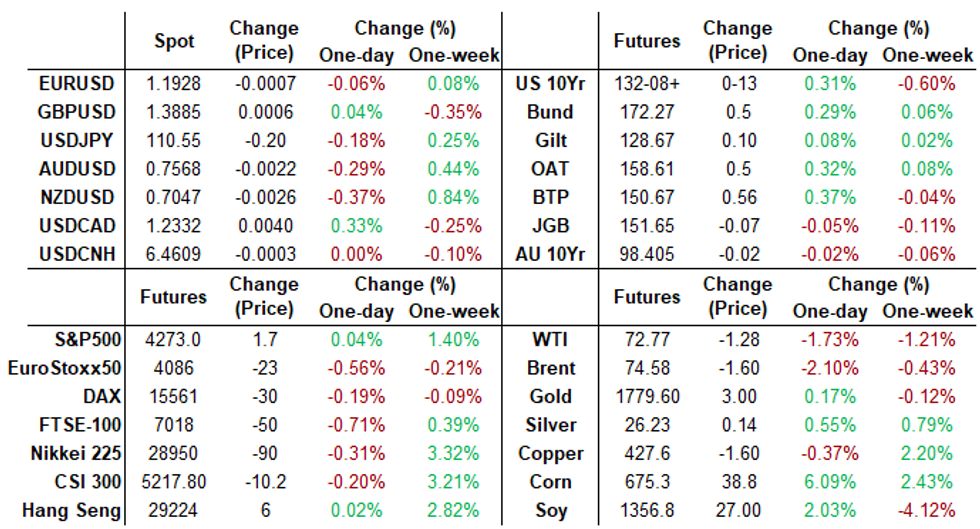

- The 2-Yr yield is down 1.2bps at 0.2543%, 5-Yr is down 2.7bps at 0.8942%, 10-Yr is down 4.8bps at 1.4765%, and 30-Yr is down 5.3bps at 2.0959%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest Settles

- O/N +0.00037 at 0.08375% (+0.00288 last wk)

- 1 Month +0.00812 to 0.10425% (+0.00513 last wk)

- 3 Month +0.00125 to 0.14725% (+0.01112 last wk) ** (New Record Low: 0.11800% on 6/14)

- 6 Month +0.00113 to 0.16663% (+0.00925 last wk)

- 1 Year -0.00175 to 0.24750% (+0.00912 last wk)

- Daily Effective Fed Funds Rate: 0.10% volume: $77B

- Daily Overnight Bank Funding Rate: 0.08% volume: $267B

- Secured Overnight Financing Rate (SOFR): 0.05%, $850B

- Broad General Collateral Rate (BGCR): 0.05%, $346B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $319B

- (rate, volume levels reflect prior session)

- Tsy 10Y-22.5Y, $1.401B accepted vs. $3.668B submission

- Next scheduled purchases:

- Tue 6/29 1010-1030ET: TIPS 7.5Y-30Y, appr $1.225B

- Wed 6/30 1010-1030ET: Tsy 7Y-10Y, appr $3.225B

- Thu 7/1 1100-1120ET: Tsy 22.5Y-30Y, appr $2.025B

FED: Repo and Reverse Repo Operations

Off last Thursday's record high of $813.573B, NY Fed reverse repo usage climbs to $803.019B from 75 counterparties Monday. Friday's usage fell to $770.830B.

MONTH-END EXTENSION: UPDATED Barclays/Bbg Extension Estimates for US

Updated forecast summary compared to avg increase for prior year and same time in 2020. TIPS 0.01Y; US Gov infl-linked -0.4Y. Note, MBS extension estimate climbs to 0.17 from 0.11 preliminary est.

| Indices | Estimate | 1Y Avg Incr | Last Year |

| US Tsys | 0.08 | 0.09 | 0.09 |

| Agencies | 0.12 | 0.04 | 0.06 |

| Credit | 0.05 | 0.12 | 0.09 |

| Govt/Credit | 0.07 | 0.10 | 0.09 |

| MBS | 0.17 | 0.06 | 0.08 |

| Aggregate | 0.06 | 0.09 | 0.09 |

| Long Gov/Cr | 0.06 | 0.09 | 0.12 |

| Iterm Credit | 0.07 | 0.10 | 0.10 |

| Interm Gov | 0.09 | 0.08 | 0.07 |

| Interm Gov/Cr | 0.07 | 0.09 | 0.08 |

| High Yield | 0.10 | 0.11 | 0.09 |

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +5,000 Green Sep 92 calls vs. Gold Sep 85/86 call spds, pays 0.25 net on conditional bull curve steepener

- 2,000 short Sep 95/96/97 put flys

- +6,000 Blue Sep 80/82 put spds vs. 87 calls, 7.0 net db

- -1,500 Green Mar 87 straddles, 49.0

- Block +2,750 Blue Sep 98.87/99.12 4x5 call spds, 7.5

- -5,000 Green Aug 99.06/99.18/99.31 put flys, 2.5 vs. 99.005/0.10%

- +2,000 Blue Aug/Sep 85 straddle spds, 7.0

- Overnight trade

- Block, 10,000 Gold Sep 97.00 puts, 0.5, another 5.6k/screen

- +2,000 TYU 130/131 2x1 put spds, 0.0

- +2,500 TYU 132 straddles, 150

- -5,000 USU 152/167 strangles, 35

- +1,500 USQ 160 calls, 100

- Overnight trade

- +4,000 TYQ 131 puts, 13

- -4,000 TYQ 132.5 calls, 20-21

- 2,000 TYQ 133.5 calls, 6

EGBs-GILTS CASH CLOSE: UK Case Surge And Some PEPP Talk

Gilts outperformed Monday, as the German and UK curves bull flattened. Periphery spreads tightened modestly as well.

- The UK recorded the highest number of COVID cases since January (22k+), though this surge largely appeared to be expected; Gilts gained all day, with 10s to 30 yields down 5+bps.

- The ECB taper debate widened, with hawks Weidmann and Holzmann calling for winding down PEPP earlier rather than later; dove Panetta said flexibility in purchases should be maintained. VP de Guindos said the ECB was mindful of second-round inflation effects.

- ECB weekly net PEPP purchases hit the highest in a year.

- Belgium sold E3.8bln of OLO; EU mandated banks for dual-tranche 5-/30Y NGEU, subject to be launched Tuesday.

Closing German/UK Yields And 10-Yr Spreads To Germany

- Germany: The 2-Yr yield is down 0.5bps at -0.652%, 5-Yr is down 2.3bps at -0.574%, 10-Yr is down 3.5bps at -0.19%, and 30-Yr is down 3.4bps at 0.311%.

- UK: The 2-Yr yield is down 2.7bps at 0.057%, 5-Yr is down 3.4bps at 0.341%, 10-Yr is down 5.6bps at 0.722%, and 30-Yr is down 6.6bps at 1.221%.

- Italian BTP spread down 1.5bps at 106.3bps / Spanish down 0.3bps at 63.2bps

FOREX: USDJPY Rejects 111 Mark Once More

- Unable to make a meaningful break above 111.00 last week, USDJPY once again retreated from the notable March highs as US equity indices also headed south following fresh record high prints earlier in the session.

- Although a technical uptrend remains in place, bulls will be wary following the inability of the pair to extend above the previous bull trigger at 110.97. Initial key support remains unchanged at 109.72, Jun 21 low. A break of this level is required to signal a top.

- Furthermore, yen crosses suffered the most on Monday, with AUDJPY and NZDJPY sliding the best part of 0.75% from their highs. Particular weakness was likely exacerbated by Sydney beginning a two-week lockdown on Sunday as a cluster of cases of the highly infectious coronavirus Delta variant rose to 110 in Australia's largest city.

- The Dollar Index continued it's consolidation trend with some initial strength being reversed throughout the latter half of Monday. With the DXY broadly unchanged, most G10 pairs are respecting most recent ranges. EM volatility was also capped with the biggest move seen in TRY (+0.77%).

- No notable price action around today's WMR fix. Citi's prelim month-end model for June indicates slight USD sales with their signal strength under half the historical norm.

- RBNZ Governor Orr due to speak overnight as well as further comments expected from Fed's Barkin tomorrow. Eurozone CPI Flash Estimate on Thursday, however, markets likely keeping firm focus on the US NFP report due Friday.

FOREX/Expiries for Jun29 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1900-10(E598mln)

- USD/JPY: Y109.30-45($1.4bln-USD puts), Y110.00-15($1.1bln-USD puts), Y110.85-90($515mln), Y112.00($1.25bln-USD puts)

- USD/CNY: Cny6.4000($510mln)

PIPELINE: $3B Philippines 2pt Launched

- Date $MM Issuer (Priced *, Launch #)

- 06/28 $3B #Philippines $750M 10.5Y +60, $2.25B 25Y 3.25%

- 06/28 $1B #Suzano Austria 10Y +180

- 06/28 $1B *LG Chem $00M 5Y +60, $500M 10Y +90

- 06/28 $1B #Mongolia $500M 6Y 3.75%, $00M 10Y 4.7%

- 06/28 $700M #Protective Life $350M 3Y +32, $350M 7Y +65

- 06/28 $Benchmark Qatar Petroleum multi-tranche investor calls

- 06/?? $Benchmark CIBC 5Y

EQUITIES: Stocks Edge Off Alltime Highs

- Stock markets started solidly, with the S&P 500 and the NASDAQ Composite striking new alltime highs at the open. This early strength faded as the session continued, however, with the Dow Jones slipping back into negative territory and the S&P 500 back to flat.

- Tech outperformed, which propped the NASDAQ above water into the close, buoyed by a solid turnout from chipmakers NVIDIA and Intel.

- Energy names were notable underperformer, with a flattening of the recent crude rally working against major oil & gas explorers. This increases the focus on the OPEC+ meeting later this week, at which the group are seen raising their daily output by as much as 550,000bpd.

COMMODITIES: WTI, Brent Rally Flattens Out

- The recent rally in oil futures has flattened out slightly, with both WTI and Brent crude lower into the Monday close. Markets focus turns to the upcoming OPEC+ meeting on Thursday, at which the group are expected to up their daily output by a further 550,000bpd - still shy of forecasts for demand growth headed into Q3.

- Both major crude benchmarks slipped around 1.5%, but managed to trade inside the recent range. This keeps first support for WTI at the Jun24 lows of $72.32/bbl.

- Silver recouped early losses having bounced ahead of the 200-dma support in spot. Early USD strength faded, helping buoy USD-denominated commodities ahead of the US close.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok