Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: Reversing Mon's Risk Aversion Move

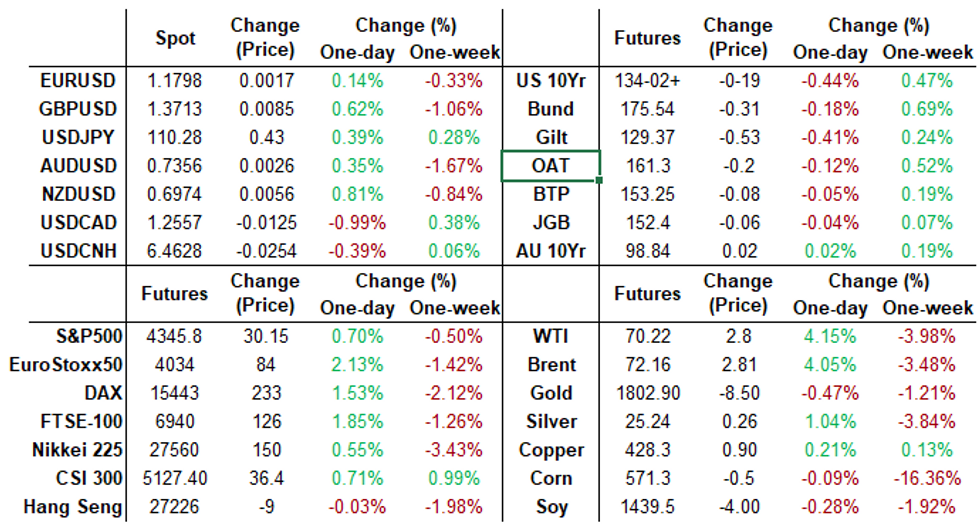

Tsys held broadly weaker but off session lows after the bell late Wednesday, bonds all the way back to last Friday's levels while equities completely erased Monday's rout as well, ESU1 marking 4348.0 in late trade.- No data to trade off of, Tsys took risk-on cues from higher global equities and softer EGBs and Gilts overnight.

- Tsys extend session lows after weak $24B 20Y auction re-open: drawing a high yield of 1.890% (2.120% last month) vs. 1.877% WI. Bid-to-cover 2.33 vs. 2.40 in June. Indirect take-up to 60.16% vs. 62.07% in June (58.77% 5M avg). Primary dealer take-up climbs to 20.91% vs. 22.60% 5M avg. Direct take-up 18.94% vs. 18.63% 5M avg.

- Moderate corporate issuance generated some two-way hedging on the day while Eurodollar futures say ongoing swap-tied flow in Greens (EDU3-EDM4).

- Focus turns to Thu's weekly claims (350k est vs. 360k prior, continuing claims (3.100M est vs. 3.241M prior).

- The 2-Yr yield is up 0.6bps at 0.2057%, 5-Yr is up 4.5bps at 0.7298%, 10-Yr is up 6bps at 1.2817%, and 30-Yr is up 5.2bps at 1.9295%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest Settles

- O/N -0.00162 at 0.08388% (-0.00188/wk)

- 1 Month -0.00237 to 0.08663% (+0.00300/wk)

- 3 Month -0.00037 to 0.13788% (+0.00363/wk) ** (Record Low: 0.11800% on 6/14)

- 6 Month +0.00038 to 0.15313% (+0.00100/wk)

- 1 Year +0.00125 to 0.24300% (+0.00088/wk)

- Daily Effective Fed Funds Rate: 0.10% volume: $70B

- Daily Overnight Bank Funding Rate: 0.08% volume: $259B

- Secured Overnight Financing Rate (SOFR): 0.05%, $855B

- Broad General Collateral Rate (BGCR): 0.05%, $373B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $348B

- (rate, volume levels reflect prior session)

- Tsy 2.25Y-4.5Y, $8.401B accepted vs. $31.868B submission

- Next scheduled purchases

- Thu 7/22 1010-1030ET: Tsy 22.5Y-30Y, appr $2.025B

- Fri 7/23 1010-1030ET: Tsy 4.5Y-7Y, appr $6.025B

FED: Reverse Repo Operations

NY Fed reverse repo usage climbs to $886.206B from 71 counterparties vs. $848.102B on Tuesday (compares to June 30 record high of $991.939B).

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +10,000 Blue Oct 98.25/98.62 put spds 3.5 over 99.00 calls vs. 98.71/0.49%

- 5,000 Green Aug 99.00 puts, 3.0

- 2,500 Blue Dec 98.37 puts, 2.0

- +5,000 Blue Dec 98.37 puts, 12.0, total volume over 16k

- +3,000 Green Oct 99.25 calls, 8.0

- +12,000 Blue Dec 98.12/99.25 put over risk reversals, 2 looking for more

- +4,000 Green Aug 99.12/99.25 2x1 put spds, 00

- 9,000 Blue Oct 98.50/98.62 put spds

- +5,000 Green Dec 98.75/99.12 2x1 put spds 1.0 over Green Dec 99.50 calls

- Overnight trade

- 10,000 Green Dec 98.50/98.75 put spds

- 10,000 Green Mar 100 calls, 1.0

- 4,000 Green Aug 99.50 calls, 1.0

- 4,000 Blue Aug 98.75 puts

- 19,200 TYU 133.5/134 put spds, 13

- Update 16,000 TYU 132.5 puts, 12-10

- Overnight trade

- 12,000 TYQ 133.75 puts, 1-3

- 5,000 TYU 136 calls, 18

- +10,000 FVU 123.5/124 put spds 1 over FVU 125.25 calls

- 4,000 USU 161/163 2x1 put spds

EGBs-GILTS CASH CLOSE: Flattening Retraces Ahead Of ECB Decision

The German and UK curves bear steepened Wednesday, retracing some of the earlier week's flattening amid a rebound in equities and ahead of the ECB meeting Thursday.

- Periphery spreads were flat/tighter in a broadly risk-on session.

- Little impactful on the headline front, with data being of a 2nd tier nature (UK public finances) and the only bond supply from Germany (Bund, EUR1.23bn allotted).

- Of note, the UK gov't demanded a re-write of the Northern Ireland protocol in the Brexit Withdrawal Agreement, setting up a showdown with the E.U. in coming months.

- Attention turns firmly to the ECB decision, which is the only calendar item of note Thursday.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.1bps at -0.715%, 5-Yr is up 0.6bps at -0.682%, 10-Yr is up 1.5bps at -0.395%, and 30-Yr is up 3bps at 0.088%.

- UK: The 2-Yr yield is up 0.9bps at 0.102%, 5-Yr is up 1.9bps at 0.301%, 10-Yr is up 3.9bps at 0.603%, and 30-Yr is up 4.6bps at 1.056%.

- Italian BTP spread down 1.3bps at 108.3bps / Spanish spread down 0.1bps at 67bps

OPTIONS/EUROPE SUMMARY: Mixed Rates Structures

Wednesday's options flow included:

- RXU1 176.5/178cs sold at 43 down to 41 in 7,318

- DUU1 112.20/112.10ps 1x2 bought for average 1.25 in 4

- ERU1/0RU1 100.50c calendar, bought the front for 2.5 in 5k

- 3RU1 100.25/100.12/100/99.87p condor, bought for 1.75 in 2k

- 0LU1 99.75c sold at 1 in 6k (ref 99.615, 5 del)

- 0LZ1 99.50/99.62cs 1x2, bought for 1 in 2k

- 2LU1 99.25p, bought for 2.75 in 3k

FOREX: CAD and NOK Enjoy Oil Price Recovery

- With crude futures retracing the majority of Monday's sell-off, the Canadian Dollar and Norwegian Krone were the clear outperformers on Wednesday.

- After taking out the overnight lows through 1.2675, USDCAD saw steady supply throughout US hours, with little to halt the CAD ascent. 1.2526 marked the low before a small bounce but USDCAD remains 1% lower for the session. CADJPY enjoyed a 1.5% rally, continuing the bounce from the 85.43 April lows matched on Monday.

- In similar vein, NOK enjoyed a strong reversal higher (EURNOK -1.24%) after reaching near 7-month lows during Monday's oil price rout.

- Overall greenback weakness helped favour NZD and GBP, both rising roughly 0.7%.

- Firmer risk sentiment left the Japanese Yen trading with a heavy tone for a second consecutive session. USDJPY rose back above 110 and eyes key resistance at 110.70, Jul 14 high in order to maintain technical bearish conditions.

- EURUSD held a relatively narrow 50 pip trading range as futures volumes indicated limited interest in the pair despite rising back to the 1.18 mark. Markets await tomorrow's July ECB monetary policy statement and accompanying press conference.

- With President Lagarde taking the spotlight, US jobless claims and consumer confidence data are unlikely to move the dial, while in the UK, MPC member Broadbent may deliver remarks at a BOE hosted event.

FOREX/Expiries for Jul22 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1650-60(E562mln), $1.1710(E1.1bln), $1.1800-15(E1.1bln), $1.1900(E589mln), $1.1935(E1.1bln)

- EUR/GBP: 0.8650(E815mln)

- AUD/USD: $0.7375(A$1.1bln)

- USD/CAD: $1.2750($1.4bln)

- USD/CNY: Cny6.4300($1.6bln), Cny6.4400($645mln), Cny6.4370($520mln), Cny6.4900-10($666mln)

PIPELINE: Indonesia Launched

- Date $MM Issuer (Priced *, Launch #)

- 07/21 $1.65B #Indonesia $600M 10Y 2.2%, $750M 30Y tap 3.1%, $300M 50Y 3.35%

- 07/21 $2.4B Carnival 7NCL 1st lien 4%a (adds to $3.5B 6NCL 5.75% on Feb 10)

- 07/21 $750M #Goldman Sachs 5Y 3.65%

- 07/21 $1B #Constellation Brands 10Y +100

- 07/21 $600M *Nonghyup Bank $300M each 3Y +55, 5Y +60

- 07/21 $Benchmark Chalco HK 3Y +125a, 5Y +145a

EQUITIES: Stocks Rally Further as Candle Pattern Points Up

- Equity markets traded solidly for a second session, with the S&P500 rising close to 1% to narrow the gap with the alltime high to just 40 points. Futures were similarly positive, with the e-mini S&P rallying sharply following the formation of a bullish Harami candle on Monday/Tuesday.

- Energy and financials were behind the rally in US indices, rising sharply after being the distinct underperformers at the beginning of the week. Recovering oil prices (aided by a sharp draw in distillate reserves) buoyed oil & gas explorers while a re-steepening of the Treasury yield curve worked in favour of banks and lenders.

- Volatile trade in stocks related to a post-pandemic recovery continued, with Carnival Cruiselines, Live Nation Entertainment and Host Hotels amongst the strongest in the S&P500. Mixed earnings for Netflix worked against the stock, which dropped 4%.

COMMODITIES: Oil Bounce Accelerates on Distillates Draw

- WTI and Brent crude benchmarks recovered further Wednesday, with the bounce accelerating on a bullish set of numbers from the Weekly DoE Report. Markets focused on the far larger than expected draw in distillates inventories, which saw stockpiles drop around 1.3mln bbls - the fastest pace of decline in months. Analysts had expected a build of 1.1mln bbls over the period.

- Traders also shrugged off the bigger-than-expected build in headline reserves, with isolated West Coast supply being largely responsible.

- Solid equity markets added some support as well as the formation of a bullish candle pattern on Monday/Tuesday, which could target first resistance at $71.40 (weekly high) and $72.48.

- Gold trade was uneventful, with the yellow metal spending most of the session in minor negative territory. Gold did print a new low of $1794.8 but steered clear of any material test on first support at the $1793.9 1.0% 10-dma envelope.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok