Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Initial Claims Inching Lower

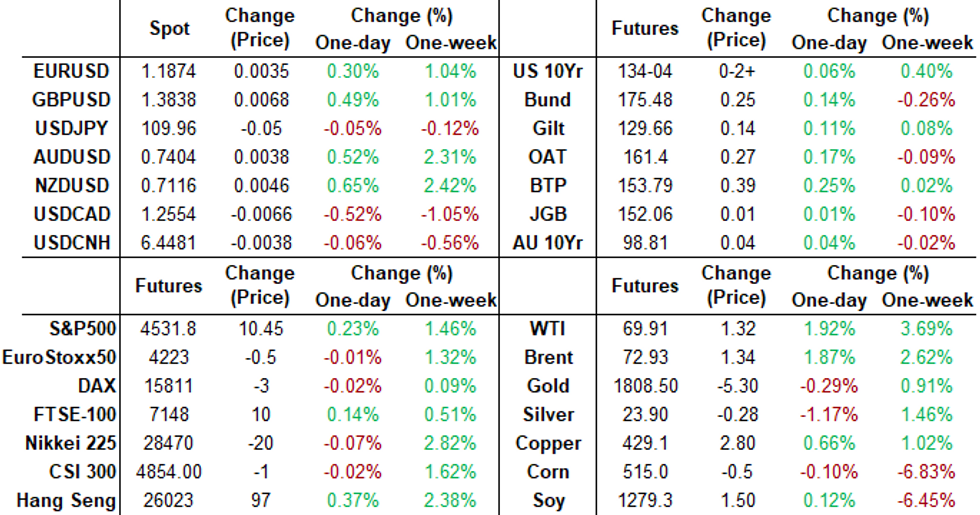

Tsys trade steady to mildly higher late Thu, very near the middle of narrow session range on modest volumes (TYZ<775k). Equities mildly higher (ESU1 +9.0), US$ weaker (DXY -.232 at 92.217), generally quiet in the lead-up to August employ data Fri morning.- August nonfarm payroll survey change median is +725k on a range of 400k to 1M, with average 707k and standard deviation 137k (suggesting a 570k to 844k figure would be roughly within expectations).

- Tsys gained early but scaled back support after lower than estimated weekly claims (340k vs. 345k), and continuing claims (2.748M vs. 2.808M), rates making session lows by midmorning (10YY 1.3037%H; 30YY 1.9228%H).

- Swappable corporate debt issuance and option related hedging generated two-way trade.

- The 2-Yr yield is up 0.2bps at 0.2115%, 5-Yr is up 0.2bps at 0.774%, 10-Yr is down 0.2bps at 1.2919%, and 30-Yr is down 0.9bps at 1.9045%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00062 at 0.07350% (-0.00262/wk)

- 1 Month -0.00037 to 0.08288% (-0.00313/wk)

- 3 Month -0.00125 to 0.11763% (-0.00225/wk) ** New Record Low

- 6 Month -0.00425 to 0.14763% (-0.00712/wk)

- 1 Year -0.00488 to 0.22275% (-0.01238/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $72B

- Daily Overnight Bank Funding Rate: 0.07% volume: $266B

- Secured Overnight Financing Rate (SOFR): 0.05%, $936B

- Broad General Collateral Rate (BGCR): 0.05%, $391B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $360B

- (rate, volume levels reflect prior session)

- Tsy 22.5Y-30Y, $2.001B accepted vs. $4.230B submission

- Fri 9/03 no buy operation ahead holiday, resume Tuesday Sep 7

FED: REVERSE REPO OPERATION

NY Fed reverse repo usage recedes to 1,066.987B from 70 counter-parties vs. $1,084.115B Wednesday. Record high of $1,189.616B set Tuesday, Aug 31.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +10,000 short Nov 99.62/99.75 call spds, 3.0 vs. 99.59/0.10%

- -10,000 Green Oct 98.62/98.75/98.87/99.00 put condors 2.25 over Green Oct 99.37/99.50 call spds

- -20,000 Green Oct 98.62/98.81/99.00 broken put flys, 3.25 wings over

- -5,000 Mar 100.06 calls, 0.5

- -2,000 Blue Dec 97.62/98.00 put spds, 1.25 legs

- Overnight trade

- -10,000 Jun 100.25 calls, 0.25

- +3,500 Green Sep 99.12/99.37 put over risk reversals, 3.0

- +2,000 Red Sep'22 99.87/100 call spds, 1.0

- -12,000 TYZ 131/135.5 strangles from 44-40

- -10,000 TYZ 133 puts 53 vs. 133-18 to -16.5/0.42%

- Overnight trade

- total +8,000 TYV 132.5 puts, mostly 14

- 4,000 TYV 132.25 puts, 11 last

- 3,300 TYV 133 puts, 21 last

- 4,000 TYV 134.5 calls, 13 last

EGBs-GILTS CASH CLOSE: Peripheries Outperform With One Eye On U.S. Jobs

Bund and Gilt yields came off session lows in Thursday afternoon trade, ending with modest bull flattening, with little decisiveness ahead of Friday's much-anticipated US jobs report.

- Periphery spreads compressed slightly, in accordance with stronger equities and a weaker dollar pointing to an uptick in risk appetite.

- Heavy supply again this morning, with Spain selling E4bln of Bono/Obli + E0.4bln linker, and France E10.5bln of OAT (incl Green OAT). That's it for the week.

- The only major data of the day showed Eurozone producer prices hit levels in July last seen in the early 1980s (+12.1% Y/Y). US data failed to have an impact.

- Final (and only, for Italy and Spain) Europe services PMIs eyed Friday.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.8bps at -0.719%, 5-Yr is down 1bps at -0.691%, 10-Yr is down 1.1bps at -0.384%, and 30-Yr is unchanged at 0.117%.

- UK: The 2-Yr yield is down 0.8bps at 0.193%, 5-Yr is down 1bps at 0.356%, 10-Yr is down 1.1bps at 0.682%, and 30-Yr is down 1.1bps at 1.023%.

- Italian BTP spread down 1.2bps at 105.2bps / Spanish down 1.2bps at 69.8bps

EGB OPTIONS: Large Sterling Call Buying Features

Thursday's European bond / rates options flow included:

- OEV1 135.75/136.0/136.25 1X2.3X1.3c fly 1x2.3x1.3, bought for 4 in 13.25k

- 0LZ1 99.50c vs 2LZ1 99.375c, bought the 1yr and receives 0.75 in 2k

- 0LZ1 99.75/99.87cs, bought for 0.75 in 40k

- 2LV1 99.25/99.37/99.50c fly, bought for 4.25 in 4k

FOREX: AUD, NZD and CAD Receive Commodity-Tied Boost, Greenback Pressured

- The dollar index is likely to close in the red for Thursday, extending a 5-day slide for the greenback.

- With the Bloomberg commodity index up 0.75% and a strong 2.5% boost for oil prices, commodity tied FX were among the best performers in the penultimate session before the August US employment report.

- NZDUSD leads G10 gains, rising 0.6% and above 0.71 for the first time since July 6. Today's peak matches closely with the 200-day moving average and represent fresh 2 and a half month highs.

- AUDUSD pierced the 50-day EMA and the 0.74 handle, maintaining a firmer technical tone with a key resistance at 0.7427 (Aug. 4 high) well in sight. The Canadian dollar took a little longer to react to the oil move, but eventually caught up firming 0.5% to 1.2557 as of writing.

- EURUSD continued to grind higher, slowly taking out Wednesday's 1.1857 highs and inching closer towards 1.19 resistance. Cable price action was a little more interesting with a sharp move from 1.3790 to 1.3836 approaching the WMR fix as EURGBP found resistance around the 0.86 handle.

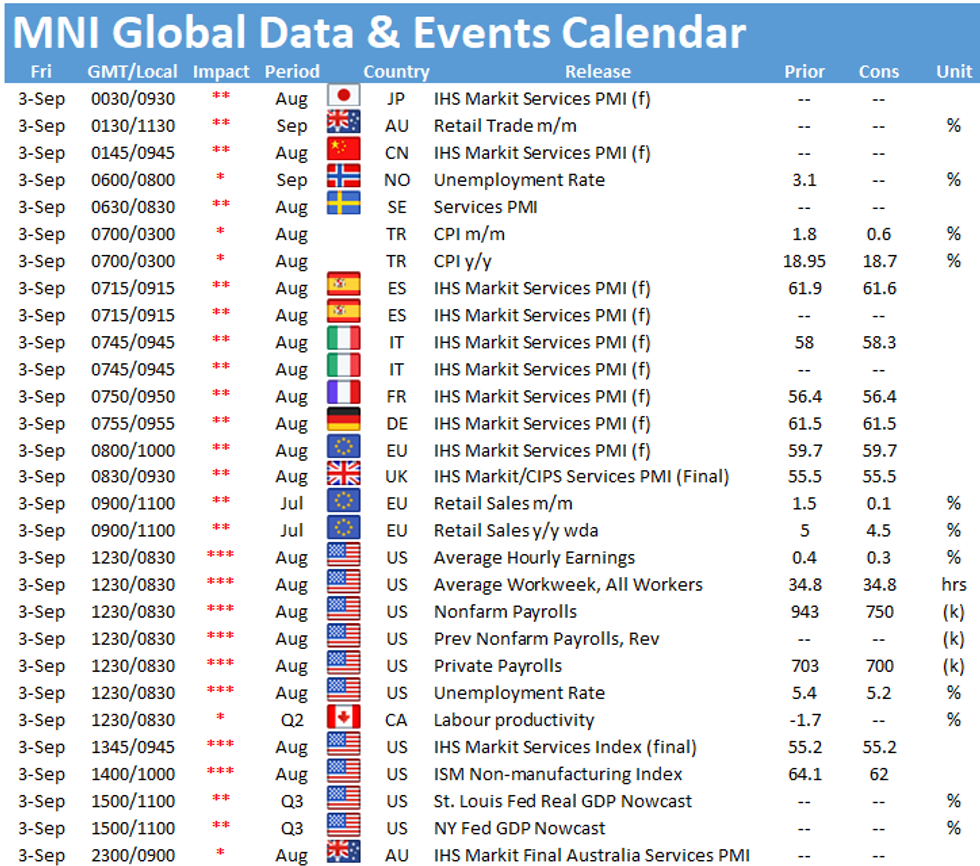

- Friday's market focus clearly on US non-farm payrolls where the current Bloomberg estimate for headline change is +725k. Australian retail sales will be also be published overnight.

FOREX: Expiries for Sep03 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1745-65(E942mln), $1.1850-55(E770mln), $1.1865-85(E2.1bln)

- USD/JPY: Y108.90-00($708mln), Y109.65-85($1bln), Y110.00($1.3bln), Y110.20($510mln)

- AUD/USD: $0.7280(A$790mln), $0.7350-70(A$1.6bln)

- USD/CAD: C$1.2500($892mln), C$1.2550($1bln)

PIPELINE: $7.025B to Price Thursday

- Date $MM Issuer (Priced *, Launch #)

- 09/02 $5B *World Bank 7Y +6

- 09/02 $1.025B #Japan Tobacco $625M 10Y +97.5, $400M 30Y 3.3%

- 09/02 $Benchmark Ahli United Bank 5Y +200a

- 09/02 $500M *Contemporary Amperex Tech 5Y +85

- 09/02 $500M *China Development Bank 3Y Green +23

EQUITIES: E-mini S&P Hits Another High, But Prices Ebb Lower Into Close

- US equity futures printed fresh alltime highs shortly following the open, tipping the high watermark to 4544.00. This price action faltered very slightly, with the e-mini S&P ebbing lower after the London close.

- The US energy sector rebounded solidly having underperformed into the midpoint of the week. Oil & gas exploration as well as oil services firms rallied sharply, with the likes of Occidental Petroleum, Marathon Oil and Diamondback Energy rallying as much as 7%.

- Across Europe, core indices traded in only minor positive territory, with the FTSE-100 higher by 0.2%, while the EuroStoxx50 held just above unchanged.

COMMODITIES: Oil Trades Firmer, Topping Technical Resistance

- Oil markets traded well Thursday, with WTI and Brent crude futures both higher by over 2%. Buoyant equity markets may have contributed, with a burst of demand following the break of the August 30 high and 50-dma (which had previously contained price action) at $69.59. This opens gains toward $70.74 – 76.4%, a Fibonacci retracement and $71.85 - the bear channel top drawn from the Jul 6 high.

- Precious metals traded lower despite the underperformance of the greenback. Silver was the notable mover, with markets unwinding the strength seen during the Wednesday session. Nonetheless, silver remains in the modest recovery uptrend seen off the early August lows, keeping markets on track to test 50-dma resistance at $24.90.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok