Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI ASIA MARKETS ANALYSIS - More Taper Talk

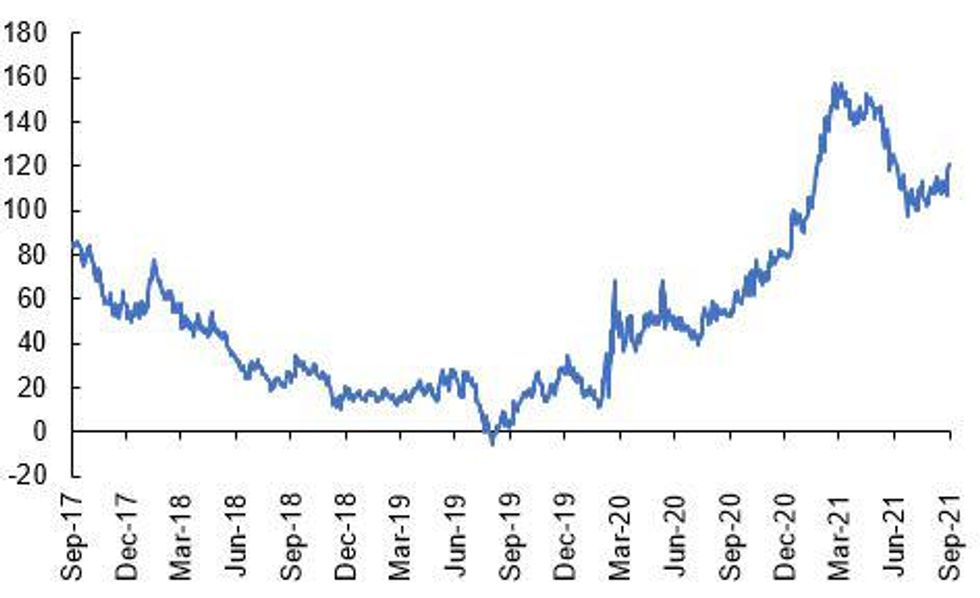

Fig 1. UST 2s10s bp

Source: MNI, Bloomberg

US TSYS: Fed Edging Closer To Tapering

USTs have traded weaker alongside a broader sell-off in European sovereign bonds earlier in the day.

- UST cash yields are 1-3bp higher on the day with the blly of the curve underperforming.

- TYZ trades at 131-25+, towards the lower end of the day's range (L: 131-19+ / 132-05+)

- Comments from several Fed speakers hit the wires earlier. Chicago Fed President Charles Evans argued: "I see the economy as being close to meeting the 'substantial further progress' standard we laid out last December" and further that "If the flow of employment improvements continues, it seems likely that those conditions will be met soon and tapering can commence."

- These comments were echoed by New York Fed President John Williams: "Assuming the economy continues to improve as I anticipate, a moderation in the pace of asset purchases may soon be warranted" and by Governor Lael Brainard: "Employment is still a bit short of the mark on what I consider to be substantial further progress. But if progress continues as I hope, it may soon meet the mark".

- Preliminary Durable Goods Orders for August came in above expectations (headline: 1.8% M/M vs 0.6% survey), while the Dallas Fed Manf. Activity Index update for September missed (4. vs 11.0 expected).

AUCTION RESULTS: 2yr sees lowest bid-to-cover since 2008

US TSYS: Bid-to-Cover Dips, Yields Bounce on 2yr Sale

2yr line relatively well digested, although bid-to-cover dips to 2.28, that's below the 2.55 average from the past six auctions. Dealer takedown also lurches higher to 33.0% - that's well ahead of the average of 28.3%. Two-year yield inches back toward overnight (and post-pandemic) highs of 0.2881% in response. Trades at 0.2861% at typing.

Full results:

* US TSY 2Y NOTE AUCTION: HIGH YLD 0.310%; ALLOTMENT 15.68%

DEALERS TAKE 32.99% OF COMPETITIVES

DIRECTS TAKE 21.69% OF COMPETITIVES

INDIRECTS TAKE 45.32% OF COMPETITIVES

BID/CVR 2.28

US TSYS: 5-Year Auction Fares Better Than 2-Year Sale

Stops through by 0.4bps for the 5-year auction, Bid-to-cover inline with average. Dealer takedown slightly higher at 25.5% vs. 23.2% average.

Five-year yields dip slightly to 0.9732% on release for a slightlybetter-than-expected auction.

Full Results:

* US TSY 5Y NOTE AUCTION: HIGH YLD 0.990%; ALLOTMENT 20.36%

HIGH YLD 0.990%; ALLOTMENT 20.36%

DEALERS TAKE 25.48% OF COMPETITIVES

DIRECTS TAKE 20.21% OF COMPETITIVES

INDIRECTS TAKE 54.32% OF COMPETITIVES

BID/CVR 2.37

EGB/GILTS CASH CLOSE: Bailey Doubles Down on Policy Sequencing

- Bund futures finished broadly flat, with the Dec-21 contract trading inside a 169.73 - 170.68 range as markets digested the German election results. Scholz's Social Democratic party fared most favourably, kicking off weeks of negotiations before a viable governing coalition can be found.

- The UK curve steepened, with the longer-end of the curve adding near 5bps as markets eyed commentary from the Bank of England governor Bailey, who reiterated that the bank rate should be used to combat inflation risks, and bank rate rises could come ahead of the conclusion of the APP.

- Portuguese, Greek and Spanish bond yields traded tighter vs. the German benchmark, whereas Italian, Austrian and French bonds traded slightly wider.

FOREX: G10FX Confined To Narrow Ranges, Cross/JPY Extending Bounce

- G10 FX price action failed to spark interest on Monday with fairly contained ranges to start the week, evidenced by an unchanged dollar index.

- Initial Euro weakness was seen following the poor showing from the German conservative bloc in their Federal elections. EURUSD traded from 1.1720 down to 1.1685, falling just one pip shy of the post-FOMC lows. The selling pressure slowly dissipated throughout the day with the single currency drifting a little higher throughout the US session, back above 1.1800.

- Bearish technical conditions were reinforced last week, opening up key support at 1.1664, Aug 20 low and an important bear trigger.

- Beneficiaries of the relentless bid in crude markets were AUD and CAD, rising between 0.28-0.4%. USDCAD support at the 50-day EMA intersection of 1.2609 has held today. However, with Brent futures narrowing the gap with $80, a clear breach of this average may signal scope for a deeper pullback, potentially exposing the 200-day at 1.2523.

- The weaker Japanese Yen helped extend the strong bounce for cross/JPY from the September 21 lows with AUDJPY and CADJPY rising close to 0.6% for today's session.

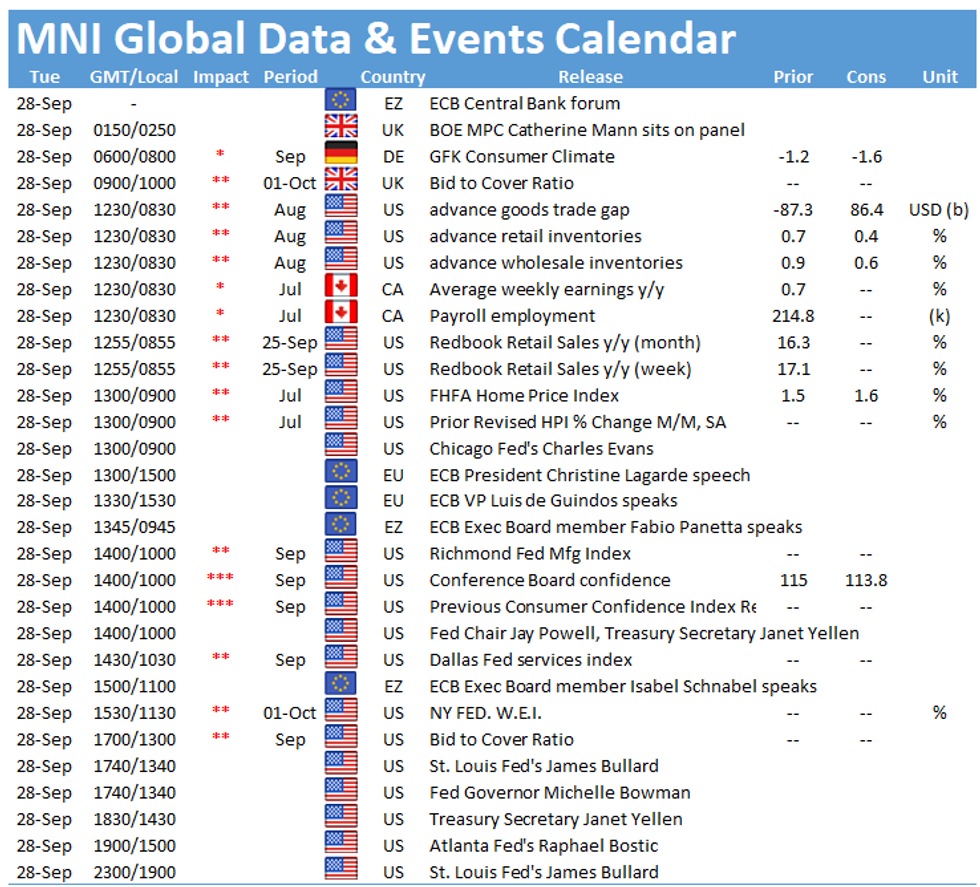

- Australian retail sales data is due overnight before a fairly heavy slate of speakers. These include ECB's Lagarde and MPC's Mann, followed by FOMC Chair Powell and members Evans, Bowman and Bostic.

FX OPTIONS: Expiries for Sep28 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1765-75(E1.5bln), $1.1790-00(E1.5bln), $1.1839-40(E525mln)

- USD/JPY: Y110.00-10($850mln), Y110.40-50($1.2bln)

- GBP/USD: $1.3700-20(Gbp520mln)

- AUD/USD: $0.7235-40(A$620mln), $0.7250-55(A$1.4bln)

- USD/CAD: C$1.2600-15($1.6bln), C$1.2675($1.6bln), C$1.2800-10($1.6bln)

- USD/CNY: Cny6.4500($1.0bln), Cny6.4530($1bln)

EQUITIES: Mixed Performance for Wall Street, as Tech Undermines NASDAQ

- Wall Street looked to finish mixed on Monday, with the Dow Jones Industrial Average holding in the green while the NASDAQ lagged thanks to an underperforming tech sector.

- The e-mini S&P briefly closed the gap with the Sep17 close, but markets will need to close above here (4464.25) to open further gains toward the record highs printed in early September.

- The energy and financials sectors led the nascent recovery off the session's lowest levels, with oil and gas explorers buoyed by a new 2021 high in oil, while banks benefited from the steeper US Treasury curve.

- A stabilization of equity markets kept VIX close to recent lows, with the index less than a point above last week's lows of 17.6 points.

- Europe traded more favourably, with particular outperformance in Spain's IBEX-35. The Spanish index closed higher by 1.5% as a solid rally in Banco Santander underpinned the index.

COMMODITIES: Brent Buoyed Toward $80/bbl

- Energy markets resumed their uptick Monday, with WTI and Brent crude futures both well bid. The rally was most notable in Brent, with prices nearing in on $80/bbl to hit a new 2021 high. A rise through this mark would be the first since late 2018 and comes as markets continue to price a particularly tight energy market across winter.

- The price formation Sep 21 was a doji candle, signalling scope for a resumption of gains and the contract last week breached 76.13, Sep 15 high to resume its uptrend. The move higher paves the way for a climb towards $80.00 next. A rally through here opens $80.37 and $82.61.

- The expected tightness in the market has become most evident in the UK, with queues and outages becoming common across petrol stations throughout the country. Supply chain constraints are largely being blamed, with ministers quick to reassure that stockpiles are plentiful and once demand subsides normality should follow.

- Gold trades within range of the Thursday/Friday lows. This confirms a resumption of the current short-term bear cycle and signals scope for a move towards $1742.5, the 76.4% retracement of the Aug 9 -Sep 3 rally. A breach of this level would open the key support at $1690.6 further out, Aug 9 low.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.