Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Tsys Off 10D Lows Ahead Nov CPI Inflation Report

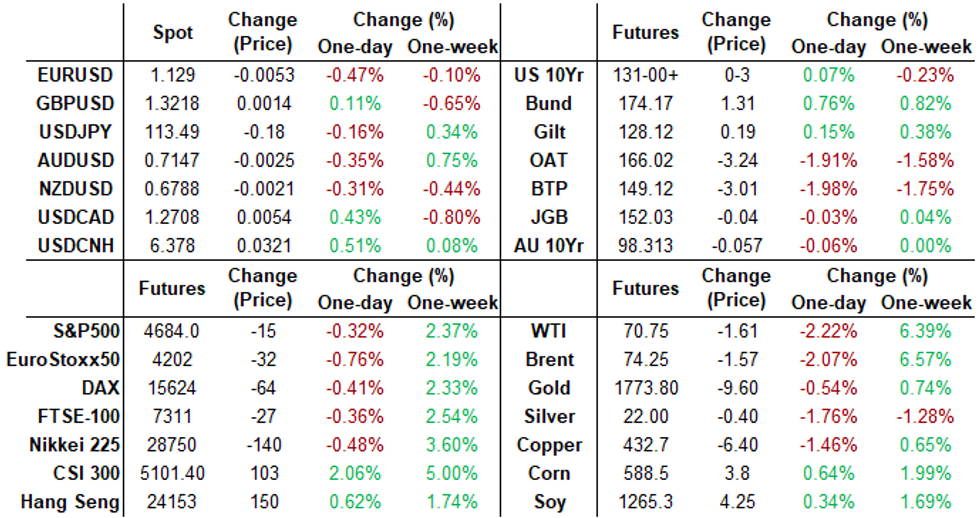

Modest gains across most of the curve, 2s weaker after the bell, bonds near session highs. Tsy futures bounced off levels last seen in late November (30YY tapped 1.9011% high, 1.8579% last) as Asian real$ bought early overnight lows in 10s and 30s, while prop and real$ bought 5s-10s during early London hours, some light curve flatteners in short end.- Tsy futures pared gains after lower than est weekly claims: 184k vs. 220k est -- lowest since 1969 BLS reports! Bonds maintained a bid on two-way trade into the bond auction.

- Tsys gap lower after second consecutive weak $22B 30Y Bond auction re-open (912810TB4) large tail:1.895% high yield vs. 1.863% WI; 2.22x bid-to-cover better than 2.20x last month (2.29x 5-month average). Indirect take-up 60.80% vs. Nov's 59.00%; direct bidder take-up 18.49% vs. 15.78% prior, while primary dealer take-up recedes to 20.71% vs. 25.23%.

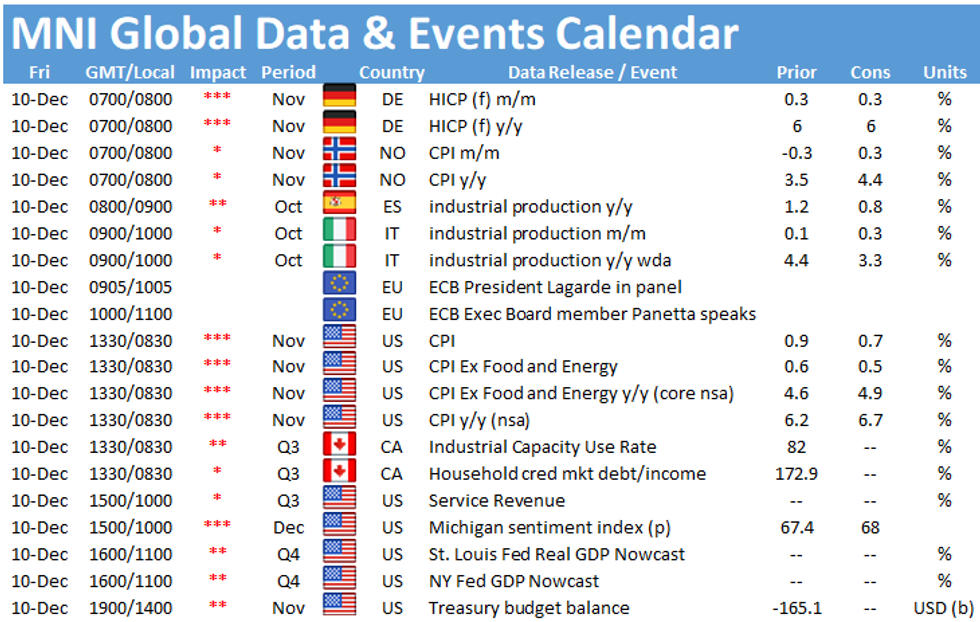

- Focus turns to Fri's headline CPI. Barring a very large miss, Nov inflation report is unlikely to change analysts' views that the Fed will accelerate taper at next Wed's meeting to give it rate hike optionality early next year.

- The 2-Yr yield is down 0.2bps at 0.6797%, 5-Yr is down 2.4bps at 1.25%, 10-Yr is down 3.8bps at 1.4836%, and 30-Yr is down 2.7bps at 1.8661%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00663 at 0.07688% (+0.00038/wk)

- 1 Month +0.00325 to 0.10463% (+0.00050/wk)

- 3 Month +0.0038 to 0.20088% (+0.01325/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00062 to 0.28875% (+0.01762/wk)

- 1 Year +0.00950 to 0.49825% (+0.03675/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $76B

- Daily Overnight Bank Funding Rate: 0.07% volume: $261B

- Secured Overnight Financing Rate (SOFR): 0.05%, $978B

- Broad General Collateral Rate (BGCR): 0.05%, $353B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $339B

- (rate, volume levels reflect prior session)

- Tsy 10Y-22.5Y, $1.401B accepted vs. $5.073B submission

- Tsy 0Y-2.25Y, $10.851B accepted vs. $33.433B submission

- Next scheduled purchase

- Fri 12/10 1010-1030ET: Tsy 7Y-10Y, appr $2.825B

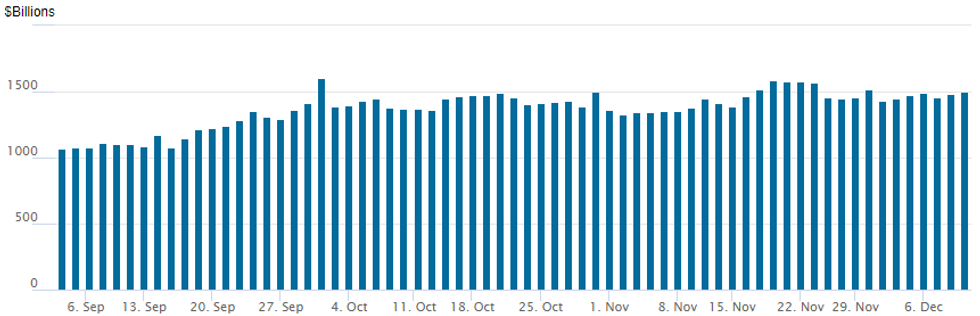

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage rebounds to $1,500.027B from 76 counterparties vs. $1,484.192B on Wednesday. Record high remains at 1,604.881B from Thursday, September 30.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +10,000 Mar 99.93 calls, cab

- +4,000 short Mar 98.25/98.62 3x2 put spds .25 over 8,000 99.12 calls

- total +10,000 Apr 99.25/99.50 put spds 2.0-2.25 over Apr 99.62 calls

- 6,000 Blue Dec 98.25 risk reversal, 0.0

- 4,000 Mar 99.68 calls, 6.5

- -2,000 Red Dec 98.25/98.75 put spds, 11.0

- 5,000 short Jan 98.37/98.62 put spds vs. short Mar 98.25/98.50 put spds

- 3,500 Green Jan 98.00/98.12 3x2 put spds

- 7,500 Blue Dec 98.25/98.50 put spds

- Block, 6,000 Red Dec 98.37/98.62/98.87/99.12 put condors 1.5 over Red Dec 99.25/99.37 call spds

- +16,000 Blue Mar 97.87/98.12 put spds, 8.5 adds to +22k Wed

- 7,500 TYH 127/134 call over risk reversal, 5cr vs. 130-11/0.25%

- 15,000 TYH 127/129 2.5x1 put spds, 2 net, 1 leg over

- +3,200 USF 164 calls, 22

- 7,000 TYF 128.25 puts, 2

- +1,500 USG 162/166 call spds, 111

- -4,500 TYG 129/131.5 strangles, 49

- +5,000 TYZ 130 puts, 4

- Overnight trade

- 10,000 TYF 128/128.5 put spds

- 2,000 FVF 122.5 calls, 1

EGBs-GILTS CASH CLOSE: Gilts Fade Early Gains

Thursday saw yields drop across the European core FI space, with periphery EGB yields also dipping but unable to keep pace with Bunds.

- While Bund and Gilt yields closed with similar moves, the direction of travel varied: UK yields dropping sharply early and retracing higher over the rest of the session (30s yields ending higher after an early drop), while German yields steadily fell.

- The latter mirrored general risk appetite, with Eurozone equities sliding.

- The main news of the session came from ECB sources pieces. Reuters noted the Gov Council will discuss at next week's meeting a temporary increase in the APP with limits on size/timespan. BBG reported the ECB could consider expanding PEPP reinvestment, incl more geographic flexibility.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.5bps at -0.701%, 5-Yr is down 3.9bps at -0.594%, 10-Yr is down 4bps at -0.353%, and 30-Yr is down 2.9bps at -0.045%.

- UK: The 2-Yr yield is down 3.2bps at 0.43%, 5-Yr is down 2.8bps at 0.554%, 10-Yr is down 2bps at 0.755%, and 30-Yr is up 2.3bps at 0.86%.

- Italian BTP spread up 1bps at 134.9bps / Greek up 3.9bps at 173.5bps

Large Bund Risk Reversal Trade Features

Thursday's Europe bond / rates options flow included:

- RXF2 171.5/173.5 RR, bought the call for 86 in 30k vs RXG2 171.5/173.5, sold the call at 103 down to 101 in 30k

- 2RZ1 100/100.12cs, sold at 8 in 4k

- 0NH2 98.90/98.70/98.50 put ladder bought for 1.5 in 5k

FOREX: US Dollar Recoups Losses Ahead Of Inflation Data

- The greenback maintained an upward trajectory on Thursday, slowly eating into yesterday’s drawdown. The DXY remains very close to last week’s close as we approach US CPI data on Friday that will be the focus for global markets.

- Largely tracking the index, EURUSD (-0.44%) edged back below 1.1300 from overnight highs around the 1.1350 mark. Similar moves lower were seen in AUD, NZD and CAD.

- One of the key moves on Thursday was in CNH, following the PBoC raising the forex reserve requirement ratio by 2 percentage points. Thereby incentivising commercial banks to hold more in FX reserves and implicitly boosting demand for USD while restricting supply. This is the second such policy move from the Chinese central bank this year, having raised the FX RRR at the end of May.

- USD/CNH initially rallied around 0.2% to touch session highs at 6.3624 but supportive price action was maintained with the pair residing 0.5% higher for the session.

- In emerging markets, the strength in the dollar combined with a string of poor domestic data releases in South African prompted a sharp pullback for the Rand where USDZAR rallied 1.75% to 16.00.

- Tomorrow’s focus will be solely on US CPI, due at 1330GMT/0830ET. Consensus is for another strong monthly print with headline +0.7% M/M and core +0.5% M/M. Barring a very large miss, November's CPI inflation report is unlikely to change analysts' views that the Fed will accelerate the taper at Wednesday's meeting to give it rate hike optionality early next year.

FX: Expiries for Dec10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1250(E750mln), $1.1290-00(E798mln), $1.1320-25(E679mln), $1.1375-85(E1.5bln)

- USD/JPY: Y113.00-20($1.0bln), Y113.95-00($729mln), Y114.25($1.2bln)

- GBP/USD: $1.3200(Gbp600mln)

- AUD/USD: $0.6900(A$1.0bln), $0.7000(A$580mln), $0.7100-15(A$1.1bln)

- USD/CAD: C$1.2495-10($1.6bln), C$1.2600-20($701mln), C$1.2740-60($808mln), C$1.2850($714mln)

- USD/CNY: Cny6.3500($1.1bln), Cny6.3900-10($710mln)

EQUITIES: Stocks Slip as Soft Oil Prices Drag on Energy Names

- Wall Street traded lower Thursday, with the S&P 500 shedding around 0.3% as sagging commodities prices weighed on oil & gas explorers. This put the energy sector at the bottom of the pile. Real estate and consumer discretionary names added further weight, while defensive healthcare stocks held minor gains.

- Elsewhere, Tesla shares traded poorly as vague rumours that the company could make an announcement failed to materialize and knocked the stock lower by as much as 3.5%.

- S&P E-minis rallied sharply higher Tuesday and the contract is holding onto recent gains. Futures are once again above the 50-day EMA, at 4568.46 today. This average highlights a pivot level and the strong recovery through it has improved conditions for bulls. The focus is on 4717.00 next, the Nov 26 high ahead of the all-time high of 4740.50. Key support and the bear trigger is at 4492.00, the Dec 3 low.

COMMODITIES: Oil Falls Back On Omicron Restrictions

- Oil futures have more than given up yesterday's mild gain, down -1.2% on latest Omicron-related restrictions. Headlines of Pfizer/BioNTech getting emergency use authorisation in the US for boosters in 16yrs+ had very little impact.

- This follows two strong daily gains earlier in the week but prices are nevertheless still circa 9% below pre-Omicron levels.

- WTI is -1.2% at $71.5 for Jan'22, close to session lows and with the first support at $69.52 (Dec 7 low). The dip has been across the futures curve, unlike yesterday where gains were concentrated in shorter-dated contracts.

- Brent is -1.1% at $75.0, below the 50-day EMA of $77.21 and with the first support at $73.20 (Dec 7 low).

- Energy data confined to US weekly rig count tomorrow, although there is dollar risk from US CPI.

- Gold has also dipped -0.45% to $1775. Once again, short-term conditions remain bearish with attention on the base of a bull channel at $1764, drawn off the Aug 9 low.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok