Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

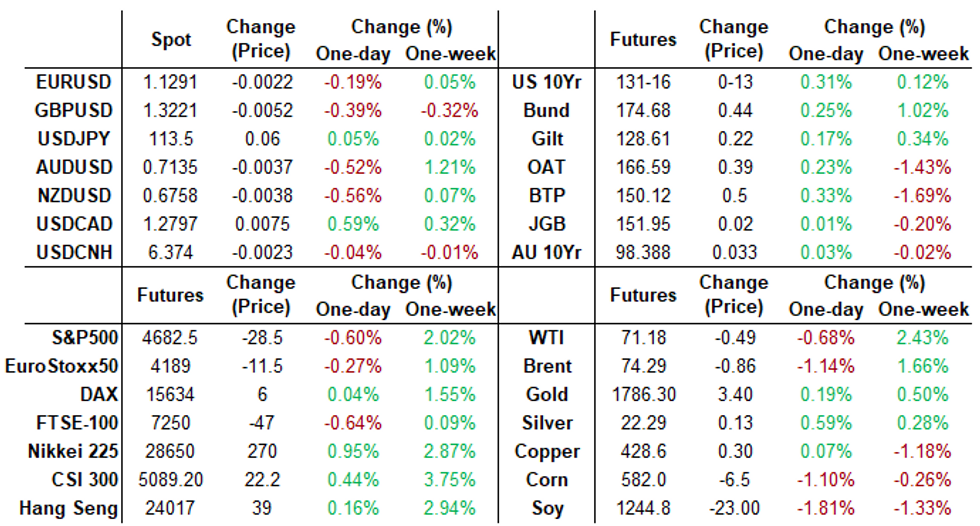

US TSYS: Tsy Yields Recede, Inflation Exp Rise

Subdued start to a busy week for central bank policy annc, FOMC on Wed, BoE and ECB on Thursday. Modest volumes with no data Monday (TYH2 just over 790k late), though NY Fed released 1Y inflation expectation of 6% underpinning rates.- Rates marched steadily higher from narrow pre-open levels. Yield curves bear steepening (5s30s back below 60.0 at 59.605 late), 30YY 1.7991% low, 10YY 1.4105% low.

- Trading desks reported selling into the grinding bid swap-tied selling in intermediates, domestic real$ selling 30s. No corporate or Tsy coupon supply tied hedging. Either risk-off with two-three waves of program selling in equities (ESH2 -30.0 late) -- or simply position squaring ahead the FOMC.

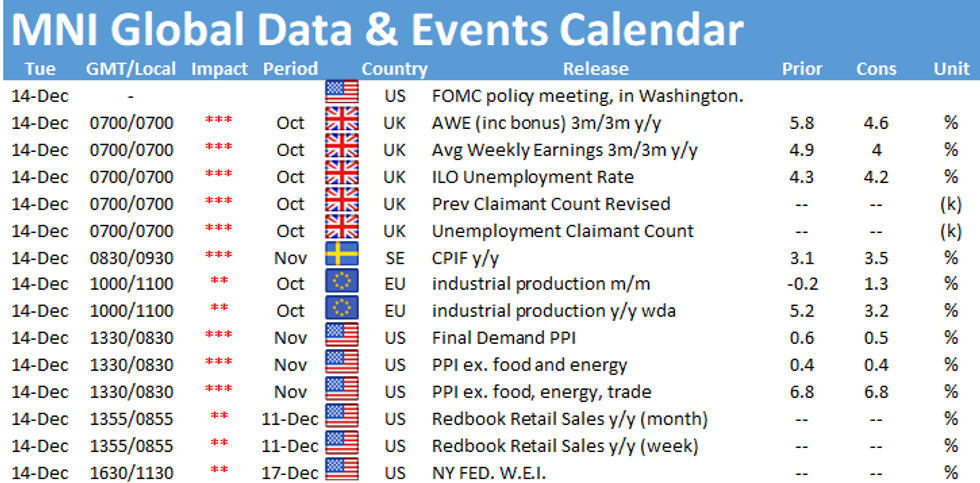

- Tuesday data focus PPI Final Demand MoM (0.6%, 0.5%); YoY (8.6%, 9.2%).

- The 2-Yr yield is down 1.2bps at 0.6425%, 5-Yr is down 3.8bps at 1.2125%, 10-Yr is down 6bps at 1.4241%, and 30-Yr is down 6.6bps at 1.8118%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00488 at 0.07713% (-0.00425 total last wk)

- 1 Month +0.00112 to 0.10975% (+0.00450 total last wk)

- 3 Month +0.00450 to 0.20275% (+0.01062 total last wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00688 to 0.29513% (+0.01712 total last wk)

- 1 Year -0.00438 to 0.50500% (+0.04788 total last wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $74B

- Daily Overnight Bank Funding Rate: 0.07% volume: $261B

- Secured Overnight Financing Rate (SOFR): 0.05%, $919B

- Broad General Collateral Rate (BGCR): 0.05%, $352B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $334B

- (rate, volume levels reflect prior session)

- Tsy 22.5Y-30Y, $1.574B accepted vs. $2.447B submission

- Updated NY Fed Operational Purchase Schedule:

- Tue 12/14 1010-1030ET: Tsy 0Y-2.25Y, appr $9.325B Vs. $10.875B prior

- Thu 12/16 1010-1030ET: Tsy 10Y-22.5Y, appr $1.625B vs. $1.425B prior

- Thu 12/16 1100-1120ET: TIPS 1Y-7.5Y, appr $1.525B vs. $1.775B prior

- Fri 12/17 1010-1030ET: Tsy 22.5Y-30Y, appr $1.825B vs. $1.600B prior

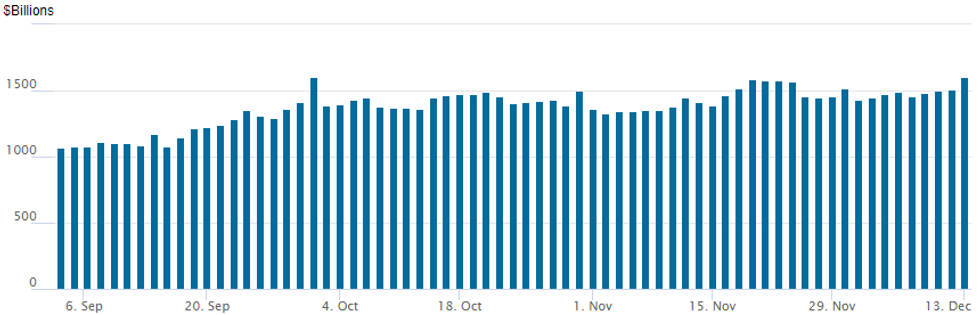

FED Reverse Repo Operation -- Usage Surge Near All-Time High

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $1,599.768B from 80 counterparties vs. $1,507.147B on Friday. Today's operation just off record high of 1,604.881B from Thursday, September 30.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +32,000 Mar 99.68 calls, cab

- +2,500 short Mar 99.12/99.25/99.37 call flys, 1.0

- -2,500 Jun 99.12 puts, 4.5

- 4,000 short Jun 98.00 puts, 8.5, 98.59 ref

- Overnight trade

- 2,000 short Mar 99.50/99.62/99.87 put flys

- +5,500 short Jun 98.31/98.37 put spds, 2.5

- 1,300 FVF/FVG 121.5 straddle spd

- -10,000 TYG 130.5/132 2x3 call spds, 57

- Overnight trade

- +5,000 TYF 128/128.5 put spds, 1

- 4,000 FVG 121.25 calls, 20

- +2,000 FVF 121.25/121.75 call spds, 4

FOREX: Greenback Edges Higher As Equities Fade, NOK Fades

- The dollar held onto early gains on Monday as equities turned from green to red throughout the US trading hours. The dollar index strengthened 0.2% to 96.30, slightly off the 96.44 highs reached during European trade.

- Dampened risk sentiment weighed on AUD, NZD and CAD, all retreating around a half a percent to start the week.

- USDCAD rose for a fourth consecutive day, briefly breaching 1.28 once again. Having broken initial resistance at 1.2768, the Dec 7 high, bearish technical pressure has eased and attention now turns to the key resistance and bull trigger at 1.2854, Dec 3 high.

- EURUSD and USDJPY both less directional, with the early dollar strength for both pairs waning and 1.1300 and 113.50 appearing the short-term inflection points for now.

- The clear underperformer on Monday was the Norwegian Krona. Both EURNOK and USDNOK rose close to one percent as fresh restrictions were announced in Norway. Interestingly, the restrictions appear less strict than perhaps expected, however, the sell-side remain mixed on whether the Norges Bank will proceed with a planned rate hike this Thursday.

- UK unemployment data will kick off the European session on Tuesday, before US PPI and potential comments from RBNZ Governor Orr - due to testify before the finance and expenditure select committee.

- The focus remains on G10/EM central bank decisions this week, with the Fed, ECB and BoE in focus from Wednesday.

FX: Expiries for Dec14 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1295-00(E642mln)

- USD/JPY: Y113.00($825mln), Y113.80-95($1.4bln)

- EUR/GBP: Gbp0.8450(E710mln), Gbp0.8530-50(E879mln)

- AUD/USD: $0.7130(A$596mln)

- USD/CAD: C$1.2670-75($529mln), C$1.2750($515mln)

EQUITIES: Indices Slide in First Hour of Trade

- An hour out from the opening bell, selling pressure accelerating across the e-mini S&P, with the index shedding around 30 points over the past hour to touch 4677.25 at the day's lows.

- Volumes are healthy so far, with over 350k contracts trading inside the past sixty minutes, with Friday's lows of 4657.00 the next level to watch.

- Energy names are leading losses, with softer WTI prices sapping explorers and refiners while consumer discretionary stocks also trade poorly.

- Automobiles and carmakers continue recent underperformance, with Tesla shares under pressure from the off - with the stock sliding as much as 4% today.

COMMODITIES: Oil Edges Higher On Saudi Threat To Shorts

- Oil futures have fluctuated today but are back close to where they started, remaining broadly within the range they’ve settled into since rallying early last week.

- A recent firming has followed the Saudi Oil Minister warning traders shorting oil prices that “I’m calling fellow OPEC+ ministers every day” and that the December meeting is “truly not suspended”.

- WTI is +0.2% at $71.8. The near-term outlook remains bullish. Attention is on $74.53 next, the 50-day EMA, whilst initial firm support lies at $69.52 (Dec 7 low).

- Brent is -0.2% at $75.0, with attention on the 50-day EMA of $77.02 and with initial support at $73.2 (Dec 3 low).

- No commodity data of note tomorrow.

- Gold has edged up +0.3% to $1788, keeping to the relatively narrow range it’s been in for a couple of weeks now. The base of a bull channel remains exposed, at $1766 when drawn off the Aug 9 low.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok