Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Fed Gov Waller Supports Hawkish Fed Pivot

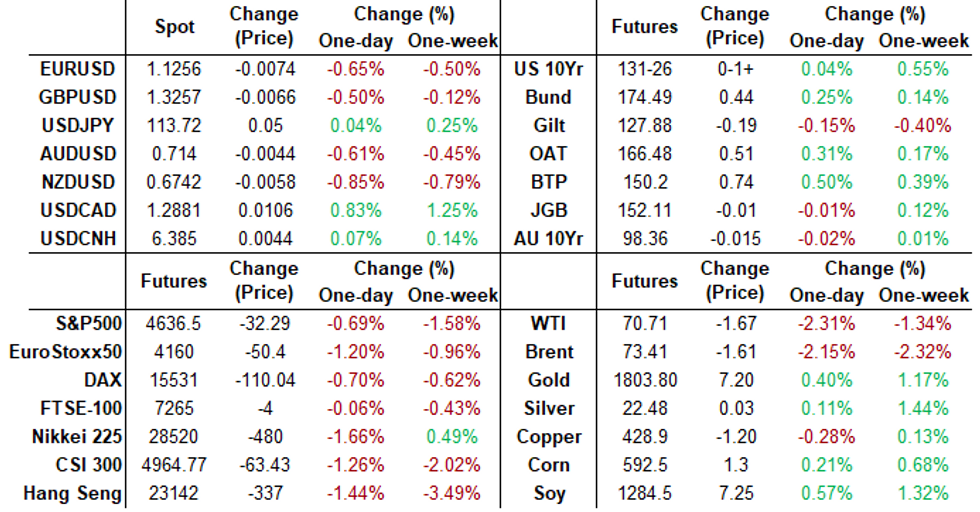

Tsys finished mixed Friday, just off week highs tapped by midmorning. Yield curves unwound a fair portion of Thu's steepening (5s30s -4.5 to appr 64.0) as rate support quickly evaporated on Fed Gov Waller comments in the second half. US$ index finished strong (DXY +.559, 96.601), stocks weaker (ESH2 -33.0 at 4626.0); crude weaker (WTI -1.71 at 70.67 after dip below 70.0).- No data, but NY Fed Pres Williams CNBC interview held market interest early, followed by Fed Gov Waller economic outlook speech to Forecasters Club in NY and SF Fed Pres Daly on live WSJ event, both at 1300ET. SF Fed Daly (non-voter 2022) a non-event, but comments from Gov Waller weighed as he aggressively supported the 2x taper pace/asset buying ending in March calling March a live event for a hike.

- Rates were back to opening levels after Gov Waller posited balance-sheet run-off by summer of 2022 "WOULD ALSO HELP REMOVE ACCOMMODATION, REDUCING THE NEED FOR ADDITIONAL RATE HIKES" Rtrs.

- Short end rates traded lower in turn, TYH2 mildly higher, well off first half levels (10YY 1.3699% low). Two-way trade, positioning from prop and fast$ accts ahead weekend and next week's Christmas holiday.

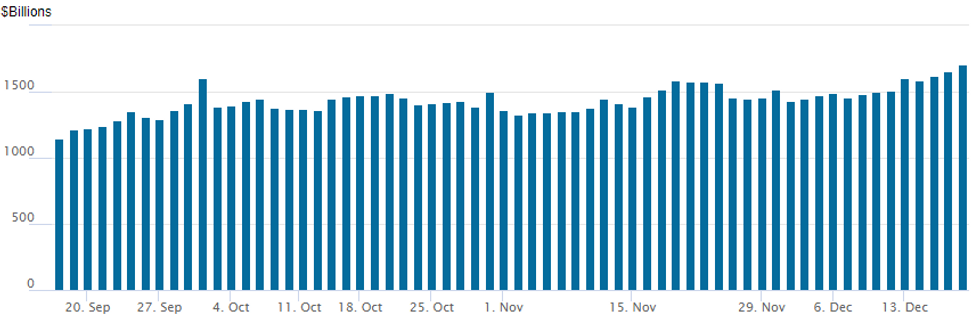

- NY Fed reverse repo usage climbs to third consecutive all-time high of $1,704.586B from 77 counterparties vs. Wednesday's $1,657.626B.

- The 2-Yr yield is up 2.7bps at 0.6396%, 5-Yr is up 1.1bps at 1.1749%, 10-Yr is down 0.9bps at 1.4021%, and 30-Yr is down 3.7bps at 1.8159%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00213 at 0.07425% (+0.00200/wk)

- 1 Month -0.00138 to 0.10250% (-0.00612/wk)

- 3 Month -0.00100 to 0.21263% (+0.01438/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00125 to 0.31275% (+0.02450/wk)

- 1 Year +0.00500 to 0.52963% (+0.02025/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $73B

- Daily Overnight Bank Funding Rate: 0.07% volume: $248B

- Secured Overnight Financing Rate (SOFR): 0.05%, $914B

- Broad General Collateral Rate (BGCR): 0.05%, $348B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $329B

- (rate, volume levels reflect prior session)

- Tsy 22.5Y-30Y, appr $1.799B accepted vs. $3.096B submission

- Next scheduled purchases

- Mon 12/20 1010-1030ET: Tsy 4.5Y-7Y, appr $4.525B vs. $5.275B prior

- Tue 12/21 1010-1030ET: TIPS 7.5Y-30Y, appr $0.925B vs. $1.075B prior

- Wed 12/22 1010-1030ET: Tsy 10Y-22.5Y, appr $1.625B

- NY Fed buy-operations pause for holidays, resume Jan 3

FED Reverse Repo Operation -- Third Consecutive New High

NY Federal REserve/MNI

NY Fed reverse repo usage climbs to third consecutive all-time high of $1,704.586B from 77 counterparties vs. Wednesday's $1,657.626B.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +15,000 short Mar 98.50/98.62 put spds vs. 98.835/0.10%

- 10,000 Green Jun 97.93 puts, 4.0

- +10,000 May 98.68 puts, 0.75-1.0

- Block, +10,000 Green Mar 98.0 puts, 4.5, +6k in pit

- +7,000 Mar 99.37/99.50/99.62 put flys, 2.5

- Overnight trade

- +12,000 short Feb 99.25 calls, 3.5

- 2,000 Green Mar 97.87/98.12 put spds

- 1,000 Blue Mar 97.75/98.00/98.25 put flys

- 25,000 Green Mar/Feb 98.00 put calendar spd, 2.0 -- adds to Block

- Blocks, 14,000 Green Mar/Feb 98.00 put calendar spd, 2.0 vs. 98.49-.50

- 47,000 FVG 122.25 calls, 8-9

- 19,000 FVF 121.5 calls, 4 last

- 19,000 FVF 121.75 calls, 2

- +5,000 TYF 132.5 calls, 5

- 3,400 TYH 128/129.5/131/131.5 put condor

- 18,000 FVG 120.5 puts

- 1,500 FVH 119.75 puts, 12

EGBs-GILTS CASH CLOSE: Gilts Underperform Again

Bunds outperformed Gilts for a second consecutive session, settling into a risk-off tone going into the weekend, amid continued concern over the Omicron variant, and ahead of a less liquid holiday period.

- Gilts were basically flat on the session as the market continued to digest Thursday's semi-surprise rate increase.

- BoE's Pill noted uncertainty of the impact of rate hikes, as well as "genuine two-sided uncertainty" over the economic impact of Omicron.

- We published our BOE and ECB meeting reviews today, see our website / emails for full analysis.

- Among periphery EGBs, BTP spreads reversed Thursday's widening, with Greece giving back some post-ECB gains.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 3bps at -0.72%, 5-Yr is down 2.4bps at -0.607%, 10-Yr is down 3bps at -0.378%, and 30-Yr is down 3.2bps at -0.037%.

- UK: The 2-Yr yield is up 0.1bps at 0.509%, 5-Yr is up 0.4bps at 0.614%, 10-Yr is up 0.2bps at 0.759%, and 30-Yr is up 1.4bps at 0.932%.

- Italian BTP spread down 4.9bps at 127.3bps / Greek up 2.1bps at 158.4bps

EGB Options: Mainly Eyeing Downside

Friday's Europe rates / bonds options flow included:

- RXF2 174.50/174.00ps bought for 18 in 5k

- RXF2 174.00/172.50ps, bought for 18 in 2k

- RXF2 174/173.5ps 1x2, bought for 1 in 2k

- RXG2 172/170ps, sold at 24 in 6k

- 0RH2 99.75p, bought for 0.75 in 3k

- SFIM2 99.30/99.00ps 1x2, bought for 1 in 1k

FOREX: US Dollar Back In Favour, Retraces Thursday Sell-Off

- After consolidating just above Thursday’s lows for much of the European session on Friday, the dollar index began a grinding retracement higher throughout the US session, rising a little over half a percent.

- The DXY retraced the entirety of the prior day’s sell-off and remains closely pinned to pre-FOMC levels around 96.60.

- Waning risk sentiment prompted a flight to quality, weighing on the Euro, Aussie, Kiwi and CAD which all fell between 0.65%-0.85%.

- EURUSD once again failed to test key resistance at 1.1383, Nov 30 high. German IFO survey suggesting GDP growth has stalled, which also weighed on the single currency. The trigger for a resumption of the downtrend is 1.1186/85, a break would open 1.1128, a Fibonacci projection.

- USDJPY, despite being unchanged, had a volatile session. Initial dollar and a softer tone for risk prompted more bailing of longs and fresh recent lows at 113.14. The sell-off was cut short as strong broad dollar demand supported the pair back to around unchanged at 113.70. Sub 112.53 levels would reverse the overall bullish trend conditions.

- In emerging markets, another turbulent day for the struggling Turkish Lira. At its worst point, USDTRY was up around 9.5% on the day to fresh all-time highs of 17.1452. CBRT intervention managed to halt the pair’s ascent, however TRY is still 5% lower on the session, with likely headwinds still lingering.

- With all major central bank meetings out of the way, next week’s event risk declines dramatically in the lead up to the holiday period. RBA minutes will be published Tuesday before markets see US Core PCE Price Index on Thursday December 23.

FX: Expiries for Dec20 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1250(E625mln), $1.1300(E916mln), $1.1335-55(E1.1bln), $1.1400(E1.4bln)

- USD/JPY: Y113.65-75($726mln), Y114.10-25($741mln), Y115.00($1.2bln)

- AUD/USD: $0.7100(A$686mln), $0.7200-05(A$1.6bln); $0.7240-50(A$1.5bln)

- USD/CAD: C$1.2800-20($690mln)

EQUITIES: Stocks Finish Week Lower, But 50-dma Provides Support

- The S&P 500 looks to finish the trading week lower, with the S&P 500 showing through the Tuesday lows ahead of the Friday closing bell. Nonetheless, the 50-dma provided some support, helping prop price action at 4,604.3.

- The financials and energy sector led the way lower, with banks suffering as the curve re-flattened and trimmed assumed interest margins. The likes of Wells Fargo and Goldman Sachs traded softer by as much as 4%, while the energy sector dropped alongside soft oil prices.

- The slip lower in prices follows a strong Thursday session for the e-mini S&P that resulted in a print above 4735.00, Nov 22 high. The break to fresh all-time highs confirms a resumption of the underlying uptrend and paves the way for a climb towards 4800.00 next. However, the contract has failed to hold onto this week's high and attention turns to support at 4589.76, the 50-day EMA. A break would strengthen a bearish threat.

COMMODITIES: Oil Ending The Week Lower On Broad Risk-Off

- Oil futures are down ~2% today amidst broader risk-off moves with equities dipping.

- WTI is -1.9% at $71.1 as it continues to swing within the $69-73.5 range from most of the past two weeks. The latest declines have been relatively spread across the curve.

- A deeper retracement would signal scope for weakness towards $65.6 (Dec 3 low) whilst on the upside, clearance of $73.34 (Dec 9 high) and the 50-day EMA at $74.05 would reinstate a bullish focus.

- Brent is -2.0% at $73.5. First support is seen at $72.5 (Dec 15 low) whilst major support is at $65.72 (Dec 2 low). Clearance of $76.61 (50-day EMA) and $76.70 (Dec 9 high) required to reinstate a bullish focus.

- Gold has pulled back from December highs in recent hours but is still up 0.3% today at $1804.1. The clearing of $1794.5 (Dec 1 high) has signaled potential for a stronger recovery towards $1815.6 (Nov 26 high).

OUTLOOK

- US Data/Speaker Calendar (prior, estimate)

- Dec-17 0830 NY Fed President Williams on CNBC Squawk Box interview

- Dec-17 1030 NY Fed buy-op: Tsy 22.5Y-30Y, appr $1.825B vs. $1.600B prior

- Dec-17 1300 Fed Gov Waller economic outlook, text, Q&A

- --

- Dec-20 1000 Leading Index (0.9%, 0.9%)

- Dec-20 1030 NY Fed buy-op: Tsy 4.5Y-7Y, appr $4.525B vs. $5.275B prior

- Dec-20 1130 US Tsy $60B 13W, $51B 26W bill auctions

- Dec-20 1300 US Tsy $60B 78D bill auction

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok