Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US: Tsy/Eurodollar Roundup: Appetite for Risk Evaporates

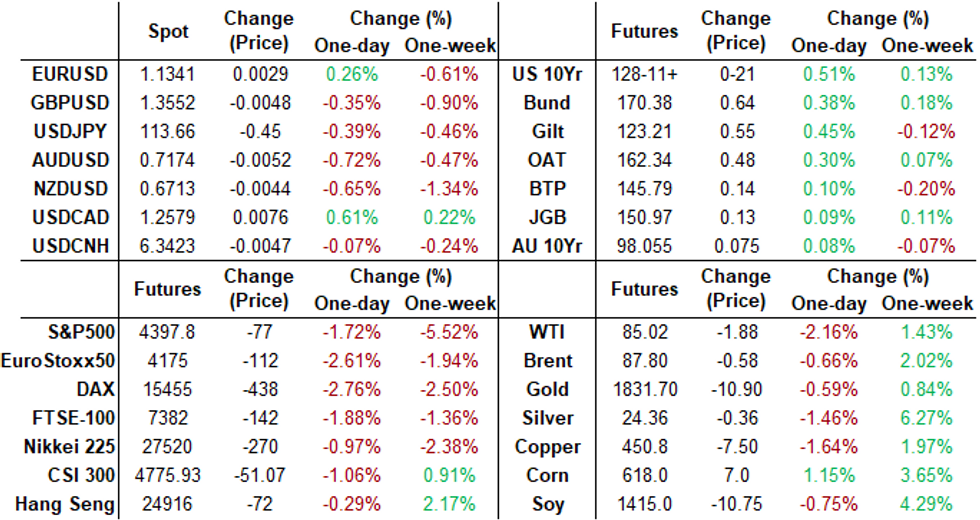

After robust midday trade, Tsy futures bounced back near early session/week highs, TYH2 tapped 128-16 -- shy of Jan 13 high/20D EMA resistance at 128-27. Equities under heavy pressure after FI close: SPX emini: 4393.0 -83.75.

- Heavy volumes (TYH2>1.8M) by the close as risk-off tone gained momentum (Russia/Ukraine and China/S China Sea flashpoints). Aside from exogenous geopolitical risk-off support/bounce, underlying positioning continues to price in tighter Fed policy for 2022 ahead next week's FOMC: four .25bp quarterly rate hikes to start in March.

- After some chunky Block buys in 2s and 5s earlier, buy-stops triggered on the rally while trading desks report better leveraged$ acct selling in 10s and 30s, prop acct steepener unwinds in shorts to intermediates.

- No corporate supply today, but hear reports of selling ahead next week's 2s, 5s and 7Y Tsy supply; Corp debt issuance expected to resume after $188.31B issued on Month so far.

- Feb serial ops expire today. Decent amount of options coming off the sheets for a serial expiry. Though accts have been active unwinding/rolling to avoid pin risk, today's rally have exposed larger positions in higher strikes, namely TYG 128 and FVG 119.25

- Option trade appears more mixed with two-way puts and larger unwinds of tactical longs (-25k TYH 127 puts, 18-21 after heavy buying this week), large 5Y call sale/exit going short (total over 83,000 FVH 120 calls from 15-19).

- The 2-Yr yield is down 3.4bps at 0.9912%, 5-Yr is down 4.1bps at 1.5454%, 10-Yr is down 5.7bps at 1.7474%, and 30-Yr is down 5.3bps at 2.0638%.

SHORT TERM RATES

US DOLLAR LIBOR: Settlement resumes:

- O/N -0.00372 at 0.07471% (+0.00071/wk)

- 1 Month -0.00158 to 0.10771% (+0.00442/wk)

- 3 Month -0.00115 to 0.25771% (+0.01642/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month -0.00186 to 0.44443% (+0.04943/wk)

- 1 Year +0.00014 to 0.79857% (+0.07286/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $75B

- Daily Overnight Bank Funding Rate: 0.07% volume: $265B

- Secured Overnight Financing Rate (SOFR): 0.04%, $927B

- Broad General Collateral Rate (BGCR): 0.05%, $346B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $339B

- (rate, volume levels reflect prior session)

- Tsy 0Y-2.25Y, $12.401B accepted vs. $42.943B submission

- Next scheduled purchases:

- Tue 01/25 1010-1030ET: TIPS 1Y-7.5Y, appr $2.025B vs. $1.525B prior

- Pause for FOMC policy annc on Jan 26

- Thu 01/27 1010-1030ET: Tsy 22.5Y-30Y, appr $1.825B steady

- Mon 01/31 1010-1030ET: Tsy 2.25Y-4.5Y, appr $8.425B vs. $6.325B prior

- Tue 02/01 1100-1120ET: TIPS 7.5Y-30Y, appr $1.225B vs. $0.925B prior

- Thu 02/03 1100-1120ET: Tsy 10Y-22.5Y, appr $1.625B steady

- Tue 02/08 1010-1030ET: Tsy 22.5Y-30Y, appr $1.825B steady

- Thu 02/10 1010-1030ET: Tsy 7Y-10Y, appr $3.225B vs. $2.425B prior

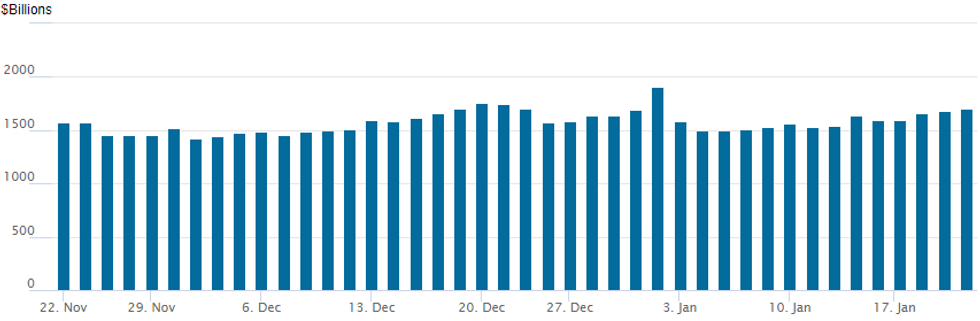

FED Reverse Repo Operation, Usage Hits New High for 2022

NY Federal Reserve/MNI

Third consecutive new high for 2022: NY Fed reverse repo usage climbs to $1,706.127B w/81 counterparties today vs. $1,678.931B prior session -- still well off all-time high of $1,904.582B on Friday, December 31.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- 12,000 Apr 99.56/Jun 99.87 1x2 call spds

- 4,000 Green Feb 98.00 straddles

- 3,600 Sep 99.50 calls, 3.5

- -12,000 Mar 99.87 puts, 36 vs. 99.515/0.95%

- -5,000 short Jun 97.93/98.00/98.25 put trees, 0.5

- +1,000 Green Mar 97.00/98.00 put spds, 30

- 8,600 TYH 127 puts, 11 over TYH 131/132.5 call spds ref 128-09

- 3,300 TYJ 129/130 strangles, 48

- 3,100 TYH 126.5/130 strangles, 22

- Update, appr -75,000 FVH 120 puts, 15-19

- over 6,000 TYJ 130 calls, 26

- over 12,000 TYG 128.25 calls, 6

- 9,500 TYG 128 puts, 1

- Overnight trade

- 5,000 TYJ 124.5/126.5 put spds

- Blocks, -25,000 TYH 127 puts 18-21 early overnight, more on screen

- +5,000 TYH 124/126 2x1 put spds, 6 vs. 127-31.5/0.08%

- Weekly midcurves:

- +9,000 wk4 TY 126/126.5 put spds, 2 vs. 127-31/0.03%

- +5,000 wk4 TY 126.5/127 put spds, 3-4

EGBs-GILTS CASH CLOSE: Strong End To The Week

European core FI enjoyed a strong end to the week, with Germany outperforming at the short end sand the UK impressing further down the curve.

- A few factors set a bullish tone early in the session: a broad sell-off in equities, weakness in commodities prices, and poor UK data (Dec retail sales missed badly).

- Bund and Gilt yields ended off their lows, as equities bounced a little in the afternoon.

- Volumes on the lighter side however, with an eye on next week's Fed decision.

- More immediately, some focus on the Italian presidential election Monday.

- BTPs and GGBs underperformed.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 4.1bps at -0.618%, 5-Yr is down 3.7bps at -0.333%, 10-Yr is down 4.1bps at -0.065%, and 30-Yr is down 4.1bps at 0.231%.

- UK: The 2-Yr yield is down 1.7bps at 0.882%, 5-Yr is down 4.6bps at 0.997%, 10-Yr is down 5.4bps at 1.171%, and 30-Yr is down 4.9bps at 1.298%.

- Italian BTP spread up 2.7bps at 135.3bps / Greek up 3.4bps at 176.5bps

EGB Options: Euribor Downside Buying Continues

Friday's Europe rates / bond options flow included:

- RXH2 169.5/167.5 ps v 171.5/172.5 cs, bought the ps for 33 in 20.5k total vs RXG2 172 put, sold at 195 in 7.5k total

- RXH2 169/168ps bought for 25 in 2k

- RXH2 172.50/174.50cs bought for 19 in 2.5k

- RXH2 171.5/173cs, bought for 29.5 in 2.5k

- RXH2 157p, bought for 1 and 1.5 in 5k (also bought Weds for 2 in ~9.3k)

- ERH3 100.12/99.87/99.62p fly (ref 100.14 d10), bought for 3 in 2k

- ERZ2 100.25/100.99.75p fly, bought for 3 in 4k straight and 4k (ref 100.30,10 del), 8k total. (This has been bought for ~20k in the past 2 sessions.)

FOREX: Safe Havens In Favour Amid Continued Slide In Equities

- Global equity indices remained under pressure with Russia/Ukraine tensions the driving factor behind the waning global risk appetite. While currency markets continue to play second fiddle to the volatility experienced in equity markets, the Swiss Franc and the Japanese Yen did outperform in the G10 space with risk-tied FX broadly on the retreat.

- USDJPY fell 0.37% to 113.70, however, much more significant moves were seen in the crosses with the likes of AUDJPY, NZDJPY and CADJPY all falling just shy of 1%.

- In similar vein, the EUR was underpinned by solid demand for EUR crosses and it is worth noting a strong bounce for EURGBP after being unable to break significant technical support at the 0.8300 mark.

- The dollar index is slightly in the red for Friday although the DXY looks likely to post 0.5% gains for the week.

- Notably, USDRUB did break to the highest levels for the year, rising 1% on the day to 77.50. This represents the highest levels for the pair since April 2021.

- Ongoing developments on the Ukrainian border will likely dominate the early price action next week, however, the release of manufacturing and services flash pmis will provide the markets with their first set of data for the week.

- In focus will be both the Federal Reserve and the Bank of Canada due to release their monetary policy decisions/statements on Wednesday.

FX: Expiries for Jan24 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1230-35(E875mln)

- USDJPY: Y113.95-05($795mln), Y114.85-00($634mln)

- AUDUSD: $0.7200(A$761mln), $0.7235(A$1.6bln)

EQUITIES: Stocks Slide for Fourth Consecutive Session

- Wall Street traded uniformly lower Friday, extending the recent weakness to put the e-mini S&P through key support at the 200-dma of 4423.7. The last time markets broke below this level was February 27th - the onset of the Coronavirus pandemic on the West Coast of the US.

- Elsewhere, earnings continue to conspire against headline index prices, with Netflix's report released late on Thursday providing a solid headwind for sentiment. Their stock slid over 20%, erasing over $40bln in market cap and reverting prices back to pre-pandemic levels.

- Communication services lagged the broader market thanks to Netflix's distinct underperformance, but weakness across consumer discretionary and materials names underlined the risk-off sentiment.

- European shares traded similarly poorly, with Germany's DAX again touching the lowest levels of 2022. The UK's FTSE-100 fared slightly better, but still managed to finish 1.2% lower.

COMMODITIES: Oil Up For Fifth Week On Supply Disruption, Geopolitics

- Crude oil prices are ending -0.6% lower on a day of broad risk-off with equities sliding. However, for the week, WTI is up +3.5% and Brent +2% after various supply disruptions and an intensification of Russia-Ukraine geopolitical risks.

- WTI is -0.6% at $85.04 after the break of key resistance at $80.72 (Oct 26 high) earlier in the week had reinforced a bullish theme. Support is $82.78 (intraday low) and resistance is seen at $87.10 (Jan 20 high).

- The most active strikes in the Mar’22 contract were $75/bbl puts.

- Brent is -0.63% at $87.82. Support is $85.54 (Jan 15 low) and resistance $89.50 (Jan 19 high).

- Gold also suffered today, -0.5% at $1830.7 as it dipped back below the previous bull trigger of $1831.9 (Jan 3 high). Support had been seen at $1805.9 (Jan 18 low) and resistance at $1848.1 (76.4% retracement of Nov 16 – Dec 15 downleg).

DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 24/01/2022 | 2200/0900 | *** |  | AU | IHS Markit Flash Australia PMI |

| 24/01/2022 | 0030/0930 | ** |  | JP | IHS Markit Flash Japan PMI |

| 24/01/2022 | 0815/0915 | ** |  | FR | IHS Markit Services PMI (p) |

| 24/01/2022 | 0815/0915 | ** | | FR | IHS Markit Manufacturing PMI (p) |

| 24/01/2022 | 0830/0930 | ** |  | DE | IHS Markit Services PMI (p) |

| 24/01/2022 | 0830/0930 | ** | | DE | IHS Markit Manufacturing PMI (p) |

| 24/01/2022 | 0900/1000 | ** |  | EU | IHS Markit Services PMI (p) |

| 24/01/2022 | 0900/1000 | ** | | EU | IHS Markit Manufacturing PMI (p) |

| 24/01/2022 | 0900/1000 | ** | | EU | IHS Markit Composite PMI (p) |

| 24/01/2022 | 0930/0930 | *** |  | UK | IHS Markit Manufacturing PMI (flash) |

| 24/01/2022 | 0930/0930 | *** | | UK | IHS Markit Services PMI (flash) |

| 24/01/2022 | 0930/0930 | *** | | UK | IHS Markit Composite PMI (flash) |

| 24/01/2022 | 1445/0945 | *** |  | US | IHS Markit Manufacturing Index (flash) |

| 24/01/2022 | 1445/0945 | *** | | US | IHS Markit Services Index (flash) |

| 24/01/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 24/01/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 24/01/2022 | 1800/1300 | * | | US | US Treasury Auction Result for 2 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.