Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SOUTH KOREA

South Korea consumer sentiment headline eased to 100.8 for August, versus 103.6 in July. It is the first headline fall since May of this year and puts the index back close to neutral levels. We are still above late 2023 lows for the index (97.3)

- GDP growth momentum eased in Q2 but current consumer sentiment levels aren't pointing to a further drastic slowing at this stage.

- In terms of the detail, spending plans all ticked down relative to July readings. Employment expectations also edged down but remain within recent ranges.

- On the price outlook, we saw a rise in expected house price changes. This reading is now at 118 versus 92 back in February. The index is now back to 2021 levels. This is a BoK and broader authority watch point, particularly ahead of an expected BoK easing cycle (although no change is expected at this Thursday's meeting).

- Today the Financial Services Commission head will meet with banking executives to discuss household debt levels (per BBG).

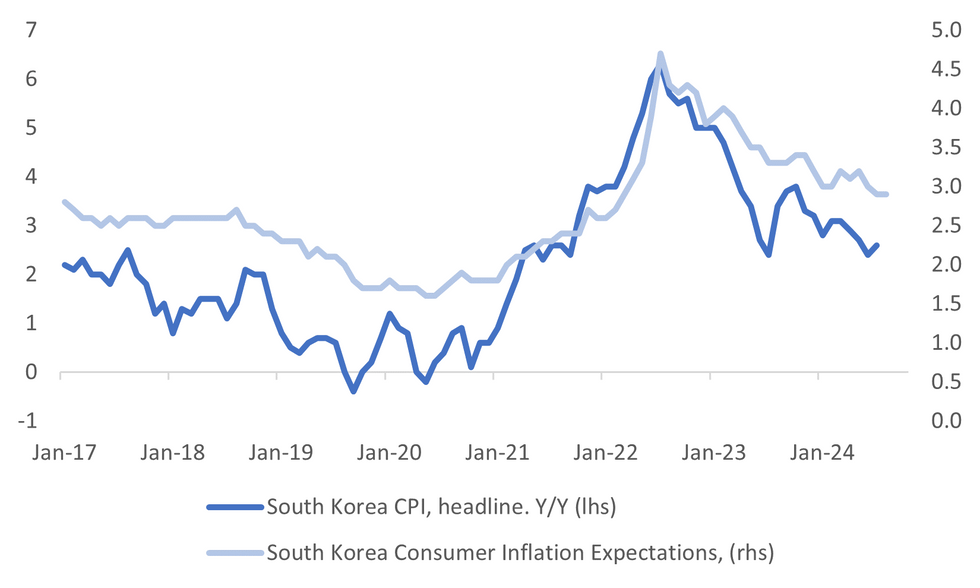

- In terms of inflation, expectations were steady at 2.9%, unchanged from July. This compares with the recent headline inflation read of 2.6%y/y, see the chart below.

Fig 1: South Korea Household Inflation Expectations Steady In August

Source: MNI - Market News/Bloomberg/BOK

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok