Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Off Lows Ahead Wed's Retail Sales, July FOMC Minutes

Tsys remain weaker, but well off midmorning lows after mixed data: Housing starts weaker for third consecutive month (1.446M), Building Permits down 1.3% on the month still better than expected for second consecutive month (1.674M).

- Bonds extended lows yet again (30YY tapping 3.1703% high) after Industrial Production (+0.6% vs. 0.3% est), Capacity Utilization (80.3% vs. 80.2% est) both stronger than expected.

- Rates spent the rest of the session gradually scaling back from lows amid two-way flow session data out of the way, participants migrating to the sidelines ahead Wed's Retail Sales (0.1% est vs. 1.0% prior) not to mention July FOMC minutes release later in the session.

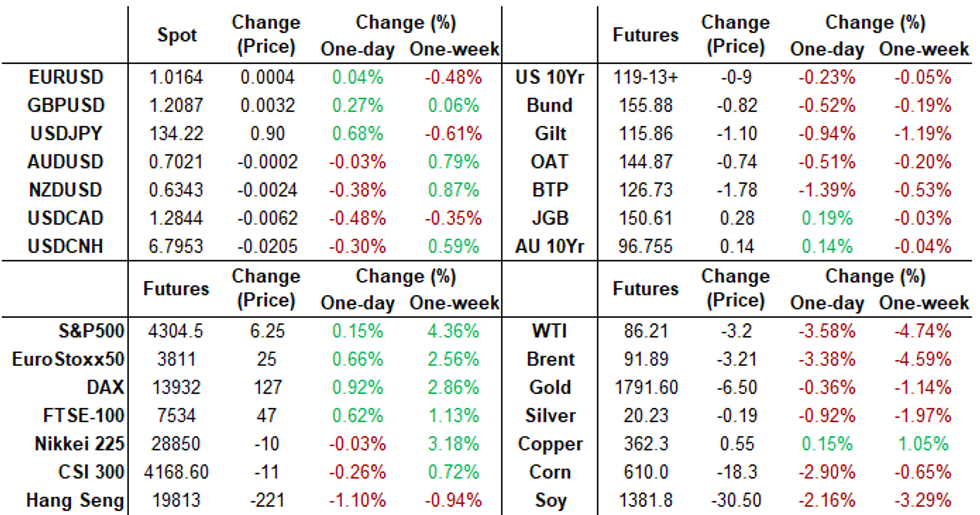

- Technicals for TYU2 currently trading 119-13 (-9.5) sustained losses through midmorning as prices fail to make any headway on 120-00 handle and 120-22 post-CPI high. Weakness at tail-end of last wk put contract through trendline support: 119-16 (Jun 16 low). Sales still considered corrective, however, the trendline break suggests a deeper retracement is likely near-term. This has opened 118-05, a Fibonacci retracement. Initial resistance to watch is 120-22, the Aug 10 high. A break would signal a possible bullish reversal.

- Additional trade tied to corporate debt issuance ($4.5B ADB 5Y SOFR+40 priced, several others including $3B KFW WNG 2Y SOFR and Goldman Sachs) generating two-way hedging/unwinds. Gradual pick-up in Sep/Dec roll volume as well.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00343 to 2.32229% (+0.00743/wk)

- 1M -0.00271 to 2.37700% (-0.00986/wk)

- 3M +0.01871 to 2.96057% (+0.03900/wk) * / **

- 6M -0.02700 to 3.50600% (-0.00329/wk)

- 12M -0.04386 to 3.95071% (-0.00829/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 2.96057% on 8/16/22

- Daily Effective Fed Funds Rate: 2.33% volume: $97B

- Daily Overnight Bank Funding Rate: 2.32% volume: $294B

- Secured Overnight Financing Rate (SOFR): 2.29%, $1.014T

- Broad General Collateral Rate (BGCR): 2.26%, $394B

- Tri-Party General Collateral Rate (TGCR): 2.26%, $388B

- (rate, volume levels reflect prior session)

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Moderate to large (for summer trade) Eurodollar put spds drove Tuesday's volume, apparently ongoing position unwinds even as underlying futures traded lower on mixed housing and better than expected IP/CapU data.- Salient flow, 20,000 Sep 96.12/96.50/96.87 put flys, 18.5 adds to 40k on Mon at 9.25 - option desks said sale as open interest declined a near amount on each leg. As the session progressed, additional spread sales included total 20,000 Dec 95.75/96.50 put spds, 40.0 vs. 96.08/0.05%, 20,000 Dec 96.12/96.50 put spds, 24.5 vs. 96.09/0.25% and 20,000 Mar 95.75/96.25 put spds, 23.0 vs. 96.085/0.24%.

- 2,000 SFRZ2 96.12/96.37 put spds

- Block, 20,000 Mar 95.75/96.25 put spds, 23.0 vs. 96.085/0.24%

- Block, 20,000 Dec 96.12/96.50 put spds, 24.5 vs. 96.09/0.25%

- Block, total 20,000 Dec 95.75/96.50 put spds, 40.0 vs. 96.08/0.05%

- Block 20,000 Sep 96.12/96.50/96.87 put flys, 18.5 adds to 40k on Mon at 9.25 (option desks say sale as open interest declines on each leg)

- 15,000 Sep 99.50/99.75 put spds

- 5,000 Sep 99.50/99.62 put spds

- +2,000 Jun 94.00/94.75/95.50 put flys, 8.75

- 40,000 Dec 98.75/99.75 put spds ref 96.095-.105

- 10,000 Dec 99.00/99.12 put spds ref 96.105

- +3,500 TYU 121 calls, 6

- -3,000 USU 138 puts, 17

- 2,000 TYX 123/125 call spds, 12

- +5,000 USU 136 puts, 5

- 3,000 wk3 TY 120 calls, 12 ref 119-19.5

- 2,000 TYV 122 calls, 21

EGBs-GILTS CASH CLOSE: BTPs Blow Out While UK Short End Underperforms

BTPs underperformed the European space as a whole Tuesday, while Gilts weakened vs Bunds.

- Widening BTP spreads (10Y yields rose the most since Jun 14, up 20+bp at session highs) couldn't be pinned to any particular catalyst but political risk ahead of September elections and thin trading volumes contributed.

- The Gilt curve bear flattened with 2Y yields briefly hitting 2-month highs; some desks cited strong wage pressures in this morning's employment report potentially encouraging more BoE hikes.

- Supply consisted of Bobl and Gilt, little reaction. The only remaining auction this week is France (Thurs).

- UK July CPI takes centre stage Wednesday, with Eurozone GDP up later in the morning.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is up 4.7bps at 0.577%, 5-Yr is up 6.6bps at 0.744%, 10-Yr is up 7.1bps at 0.971%, and 30-Yr is up 7.5bps at 1.23%.

- UK: The 2-Yr yield is up 12.3bps at 2.155%, 5-Yr is up 11bps at 1.965%, 10-Yr is up 10.8bps at 2.125%, and 30-Yr is up 8bps at 2.515%.

- Italian BTP spread up 8.8bps at 216.3bps / Greek up 7.6bps at 236.5bps

EGB Options: Bund Unwinding And Rolling

Tuesday's Europe rates / bond options flow included:

- DUV2 109.0/108.5 put spread bought for 9.5 in 3.7

- OEX2 125/123.50/122p fly, bought for 17 in 1.5k

- RXV2 154.5/157 call spread vs 149 put bought for 29 in 3.6k

- RXU2 152/153/154 call fly sold at 6 in 4k. Hearing this is an unwind

- RXV2 150.00/146.00/145.00 put ladder bought for 33.5/34 in 6k

- Selling 5.5k RXU2 156.00 puts, buying 5.5k RXV2 151.00/147.50 ps, receiving net 30 (roll Sep into Oct)

- ERU2 99.125/99.00 put spread bought for 1 in 5k

- 0RU2 98.50/98.25 put spread vs 2RU2 98.375/98.125 put spread, sold at 3 in 5k (-0R, +2R)

- SFIU2 97.75/97.80 call spread vs 97.45/97.40 put spread, net paid flat in 4k

FOREX: JPY Under Pressure As Core Yields Reverse Monday Price Action

- The Japanese Yen was the poorest performer in G10 FX on Tuesday as global fixed income markets reversed Monday’s price action and core yields took a leg higher.

- USDJPY (+0.68%) took out the Monday highs in early Europe and the rally gained momentum as we broke back above 134, narrowing the gap with the pre-US CPI levels for the pair around the 135 mark. Firm short-term resistance has been defined at 135.58, the Aug 8 high.

- USDJPY’s ascent lent overall support to the dollar index, which extended north of the Monday highs and briefly made a new high for August at 106.94. However, greenback momentum from this point waned and after the DXY had reversed to unchanged levels on the day, FX markets were happy to consolidate ahead of tomorrow’s data.

- Both EUR and GBP traded higher as a result of the greenback’s turnaround, however they both remain comfortably below the week’s opening levels as the European energy crisis continues to loom in the backdrop.

- The Chinese offshore Yuan saw a moderate pullback after Monday’s significant drop. USDCNH (-0.30%) dropped back to 6.7908 and looks set to close around yesterday’s breakout point around 6.7950.

- Focus overnight will be on the RBNZ rate decision. With a 50bp OCR hike seen as a done deal this week, the focus will fall on the Reserve Bank's forward-looking comments, with particular emphasis on the OCR track. The tone of this MPS will be set by the combination of hints on how policymakers are planning to handle the inflation/growth dilemma further down the road.

- Elsewhere, Australia wage price index data will precede the Uk’s release of July CPI and Eurozone GDP. The focus will then turn to US July Retail Sales and the release of the FOMC minutes.

FX: Expiries for Aug17 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1000-15($1.2bln), $1.0190-00($727mln), $1.0300(E697mln)

- USD/CAD: C$1.2855($515mln), C$1.3065($864mln)

- USD/CNY: Cny6.7600-14($685mln)

Late Equity Roundup: Midday Support Evaporating

Consumer Discretionary and Staples sectors continue to outperform, while late session sell-programs taking wind out modest rally. Currently, SPX eminis trade +12.25 (0.29%) at 4310.5; DJIA +162.21 (0.48%) at 34075.94; Nasdaq underperforming -76.3 (-0.6%) at 13052.53.

- Stocks ignored mixed data that weighed on Tsys earlier, held range even after positive earnings from Home Depot (HD) beat exp: $5.05 vs. $4.983 exp, and Walmart (WMT) beat: $1.77 vs. $1.626 exp.

- Consumer Discretionary sector lead by specialty retail with Bed Bath and Beyond (BBBY) surged over 85% to late morning high of 28.60 after trade halt called. Incidentally, Bath and Body Works (BBWI) gaining 6.40% at the moment, Best Buy (BBY) +6.01%, Target (TGT) +5.38%. ahead additional retailer and high-tech earnings this wk: Target (TGT) early Wed: $0.725 est; Lowe's Group (LOW): $4.611 est; Tech: Cisco (CSCO): $0.816 est; Applied Materials (AMAT) $1.77 est early Thu.

- SPX leading/lagging sectors: As noted, Consumer Staples and Discretionary averaging +1.20%, Financials (+0.64%), Materials (+0.60%). Laggers: Information Technology (-0.56%), Energy (-0.43%) and Real Estate (-0.29%).

- Dow Industrials Leaders/Laggers: Home Depot (HD) surge on strong earnings: +15.67 at 330.28, Walmart (WMT) +7.99 at 140.59, Boeing (BA) +2.62 at 173.09. Laggers: Salesforce (CRM) -0.70 at 190.36, Goldman Sachs (GS) -0.39 at 355.46, 3M (MMM) -0.34 at 151.09.

E-MINI S&P (U2): Bullish Extension

- RES 4: 4419.15 2.236 proj of the Jun 17 - 28 - Jul 14 price swing

- RES 3: 4400.00 Round number resistance

- RES 2: 4345.75 2.00 proj of the Jun 17 - 28 - Jul 14 price swing

- RES 1: 4306.50 High May 4

- PRICE: 4296.00 @ 12:35 BST Aug 16

- SUP 1: 4111.80 20-day EMA

- SUP 2: 4044.28/3913.25 50-day EMA / Low Jul 26 and a key support

- SUP 3: 3820.25 Low Jul 18

- SUP 4: 3723.75 Low Jul 14

S&P E-Minis traded higher once again Monday and the contract maintains a bullish tone. The climb extends the positive price sequence of higher highs and higher lows. Moving average conditions are in a bull mode set-up too. The focus is on 4306.50 next, the May 4 high and potentially 4400.00 further out. On the downside, initial firm support is at 4111.80, the 20-day EMA. The 50-day EMA intersects at 4044.28 - a key support.

COMMODITIES: Crude Oil Slides On Iran Deal Prospects (Again)

- After a mixed session, crude oil has declined more than 3% with renewed prospects of eventual Iranian supply after the EU saw Iran’s response to the draft nuclear deal as constructive, with the US currently studying Iran’s response and consulting with EU allies.

- WTI is -3.3% at $86.45 as it reinforces bearish conditions having cleared support at $86.82 (Aug 15 low) and in doing so opened $85.37 (Mar 15 low).

- Brent is -3.03% at $92.22, clearing support at $92.78 (Aug 5/15 lows) and opening the bear trigger at $91.22 (Jul 14 high).

- Gold is -0.2% at $1775.9 on higher UST yields but still maintains a bullish tone despite recent retracement having previously cleared trendline resistance at $1784.7. That said, support is currently eyed at the 20-day EMA of $1772.0 after which it would open a key short-term support at $1754.4 (Aug 3 low).

- US natural gas meanwhile at one point surged 7.3% to session high of $9.37 in delayed response to Germany denying reports it will keep three nuclear plants running.

Wednesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 17/08/2022 | 0130/1130 | *** |  | AU | Quarterly wage price index |

| 17/08/2022 | 0200/1400 | *** |  | NZ | RBNZ official cash rate decision |

| 17/08/2022 | 0600/0700 | *** |  | UK | Producer Prices |

| 17/08/2022 | 0600/0700 | *** | | UK | Consumer inflation report |

| 17/08/2022 | 0600/0800 | ** |  | NO | Norway GDP |

| 17/08/2022 | 0830/0930 | * | | UK | ONS House Price Index |

| 17/08/2022 | 0900/1100 | * |  | EU | Employment |

| 17/08/2022 | 0900/1100 | *** | | EU | GDP (p) |

| 17/08/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 17/08/2022 | 1230/0830 | *** | | US | Retail Sales |

| 17/08/2022 | 1330/0930 | | US | Fed Governor Michelle Bowman | |

| 17/08/2022 | 1400/1000 | * | | US | Business Inventories |

| 17/08/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 17/08/2022 | 1700/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

| 17/08/2022 | 1820/1420 | | US | Fed Governor Michelle Bowman |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.