Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Fed Speak Flattens Yld Curves Ahead Jackson Hole Eco-Summit

Tsy futures near late session highs after the bell, focus turns to KC Fed's annual Jackson Hole Economic Symposium: Reassessing Constraints on the Economy and Policy, agenda release tonight at 2000ET; Chairman Powell speaks Fri at 1000ET (0800 local), text is expected but no Q&A.- Modest reaction to early data: Tsys bounced after setting session lows on lower than expected weekly claims at 243k vs. 252k est, first revision of Q2 GDP is -0.6% vs. -0.7% est. Yield curves briefly extended session highs (2s10s tapped -25.669) before mixed Fed speak:

- Trading desks citing Philly Fed Harker comment on a 50bp hike is "still a substantial move" for latest bounce after conceding there is no decision yet on the size of a hike at the Sep FOMC. That said, Harker told MNI the Fed should hike above 3.4% by Dec to combat soaring inflation, adding that rates could continue rising next year or hold at that level for some time. Atlanta Fed Bostic said strong data could tip Fed toward 75bp, while KC Fed George: rates could exceed 4%.

- Yield curves flatter/near lows after Tsys extend highs on strong $37B 7Y note auction (91282CFJ5) stopped through: 3.130% high yield vs. 3.159% WI; 2.65x bid-to-cover vs. 2.60x last month

- Heavy session volumes (TYZ>2.6M) tied to surge in Sep/Dec rolling ahead next Wed's First Notice date (Dec takes lead).

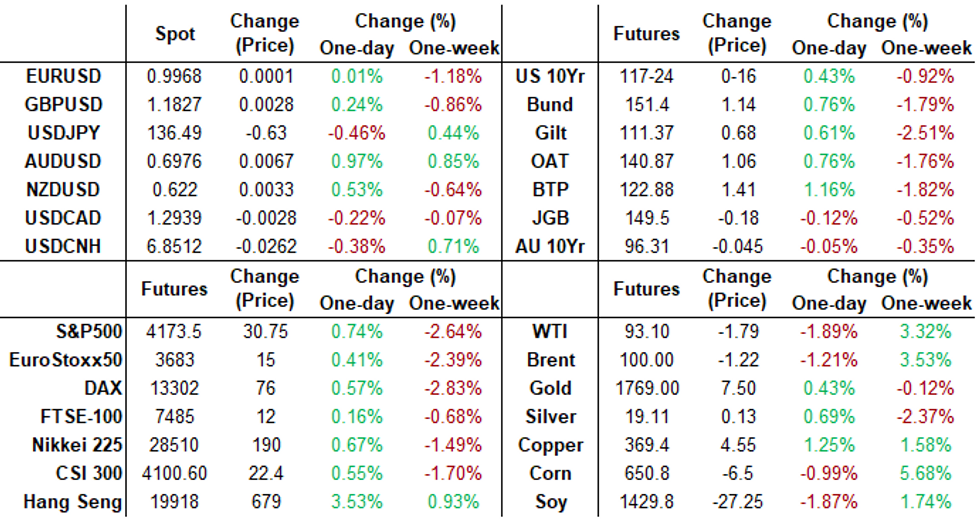

- Currently, 2-Yr yield is down 2bps at 3.3701%, 5-Yr is down 7.9bps at 3.1539%, 10-Yr is down 8.2bps at 3.0221%, and 30-Yr is down 8.1bps at 3.2314%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00100 to 2.32043% (-0.00071/wk)

- 1M +0.03857 to 2.49343% (+0.06815/wk)

- 3M +0.03314 to 3.04314% (+0.08543/wk) * / **

- 6M +0.03343 to 3.52686% (-0.02071/wk)

- 12M +0.01815 to 4.09729% (+0.08143/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 3.01000% on 8/24/22

- Daily Effective Fed Funds Rate: 2.33% volume: $94B

- Daily Overnight Bank Funding Rate: 2.32% volume: $278B

- Secured Overnight Financing Rate (SOFR): 2.27%, $969B

- Broad General Collateral Rate (BGCR): 2.26%, $388B

- Tri-Party General Collateral Rate (TGCR): 2.26%, $375B

- (rate, volume levels reflect prior session)

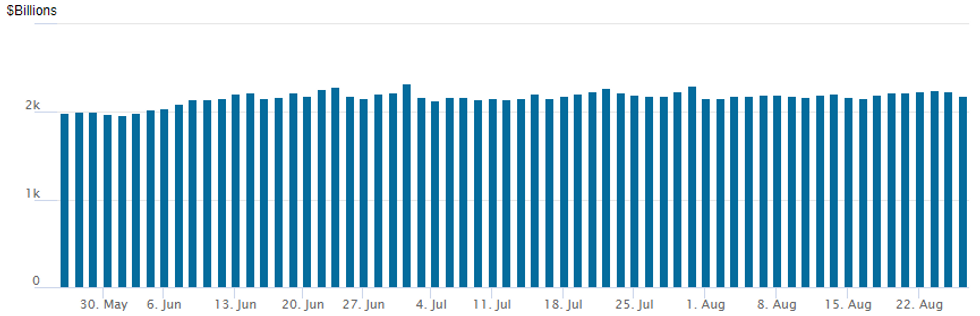

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage continues to recede, latest at $2,187.907B w/ 97 counterparties vs. $2,237.072B prior session. Record high still stands at $2,329.743B from Thursday June 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Limited second half option volume included a buy og 12,000 Oct 2Y 105.75 calls at 2.5 (opener). First half highlight: chunky limited downside SOFR put fly buyer targeting 96.00 by year end, SFRZ2 currently trading 96.36 (+0.005)- SOFR Options:

- +70,000 SFRZ2 95.50/96.00/96.50 put flys

- 3,000 short Sep SOFR 96.12/96.37/96.62 put flys

- 2,000 SFRM3 99.50 puts 11.5

- Block, 2,700 SFRM3 94.00 puts, 4.0

- Eurodollar Options:

- 2,500 Dec 96.25 calls, 13.5

- Treasury Options:

- 12,000 TUV 105.75 calls, 2.5

- 2,500 FVZ 112 calls

- 3,000 TYV 117/117.5 put spds 13 over TYV 119/119.5 call spds

- 5,000 TYV 113/114 put spds, 4 ref 117-08

- 3,000 FVV 109.75/111 put spds

- +2,000 USU 135 puts, 12

- 2,500 TYU 117.25/117.75 1x2 call spds

EGBs-GILTS CASH CLOSE: Some Relief Ahead Of Jackson Hole

EGBs and Gilts enjoyed a relief rally Thursday following a selloff earlier in the week, and ahead of Friday's highly anticipated speech by Fed Chair Powell.

- Little in the way of obvious headline drivers Thursday, with trading within the prior session's ranges, and only a modest and brief reaction to data (stronger-than-expected German IFO in the morning and US GDP / jobless claims in the afternoon).

- As losses have been led earlier this week by the short end and belly of the UK and German curves, those segments outperformed today.

- Euribor futures rose for the first time since Aug 14 (Dec23 down 9bp implied), while UK rate futures enjoyed their biggest jump of the month (down 13.5bp implied).

- Periphery EGB spreads fell sharply: 10Y BTPs down nearly 8bp to Bunds (the biggest narrowing since Aug 3), while GGBs were 4+bp tighter.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is down 5bps at 0.871%, 5-Yr is down 7.3bps at 1.085%, 10-Yr is down 5.3bps at 1.317%, and 30-Yr is down 0.8bps at 1.496%.

- UK: The 2-Yr yield is down 13.2bps at 2.806%, 5-Yr is down 12.6bps at 2.577%, 10-Yr is down 8.3bps at 2.615%, and 30-Yr is down 4.4bps at 2.89%.

- Italian BTP spread down 7.7bps at 224.1bps / down 4.2bps at 258.3bps

EGB Options: Further Bobl Put Spread Buying Thursday

Thursday's rates / bond options flow included:- RXV2 139.00/136.50ps 1x1.5, bought for flat in 2k. Note: was also bought in 5k on Wednesday.

FOREX: AUD Outperforms As Equities Edge Higher

- Growth proxy currencies have outperformed on Thursday, with AUD/USD (+1.01%) holding onto the majority of overnight gains, narrowing the gap with $0.70. A break above this mark opens initial firm resistance at 0.7040, the Aug 16 high where a break is required to ease the current bearish pressure.

- The greenback trades generally weaker putting the USD Index further off the recovery high printed earlier this week at 109.27, but pullbacks are expected to remain shallow ahead of the Jackson Hole Policy Symposium which has formally kicked off with Fed officials giving interviews throughout he US session. Markets watch for confirmation of the full agenda, with a speech from Fed's Powell the focus on Friday.

- NZD (+0.61%) is gaining in sympathy with the AUD, while EUR rallies continue to meet stiff supply, explaining the pair being unchanged on Thursday. Energy costs continue to add to the stagflation narrative, with 2023 power costs across Germany rising to new record highs ahead of the NY open.

- Elsewhere, the greenback weakness has been broad based and the likes of JPY, GBP, CAD, CHF and CNH have all posted modest gains ahead of tomorrow’s main event. Overall, price action has been expectedly subdued.

- Aside from Powell, potential comments from RBNZ Governor Orr who is due to speak in an interview conducted by Bloomberg TV at Jackson Hole overnight. Although data will likely take a back seat tomorrow, we have US Core PCE Price Index, personal spending and UniMich consumer sentiment on the docket.

FX: Expiries for Aug26 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9850(E2.3bl) $1.0000(E1.5bln), $1.0049-55(E1.1bln)

- USD/JPY: Y134.00($550mln), Y136.95-10($1.4bln)

- USD/CAD: C$1.2870-85($698mln)

- USD/CNY: Cny6.8500($576mln)

Late Equity Roundup, Communication Services Takes Lead

Stocks inching back near midmorning highs in late trade, Communication Services sector edging past Materials. Currently, SPX eminis trade +26.75 (0.65%) at 4169.5; DJIA +97.54 (0.3%) at 33066.43; Nasdaq +120 (1%) at 12550.83. OTC shares appeared to receive a boost earlier on WSJ headline that "U.S. CHINA NEAR DEAL TO LET U.S. INSPECT CHINESE COMPANY AUDIT RECORDS IN HONG KONG.

- SPX leading/lagging sectors: Communication Services outperforming (+1.46%) media and entertainment leading w/ Dish Network (DISH) +4.54%; Materials sector a close second (+1.43%) lead by Freeport McMoRan (FCX) +4.25%, NuCor (NUE) +3.01%; followed by Financials (+1.0%). Laggers: Consumer Staples (flat), Energy (+0.07%) and Utilities (+0.08%).

- Dow Industrials Leaders/Laggers: Boeing (BA) +4.60 at 168.20, Caterpillar (CAT) +4.19 at 198.35, Goldman Sachs (GS) +3.22 at 345.16. Laggers: Salesforce.Com (CRM) paring steeper losses currently -8.77 to 171.24 -- hammered after beating earnings est while trimming full-year guidance; Procter & Gamble (PG) -0.95 at 144.87, Merck (MRK) -0.47 at 89.54.

- Notable earnings annc's after today's close: Dell $1.636 est, Gap Stores (GPS) -$0.68, Marvell Technology (MRVL) $0.564 est.

E-MINI S&P (U2): All Eyes On The 50-Day EMA

- RES 4: 4419.15 2.236 proj of the Jun 17 - 28 - Jul 14 price swing

- RES 3: 4345.75 2.00 proj of the Jun 17 - 28 - Jul 14 price swing

- RES 2: 4288.00/4327.50 High Aug 19 /16 and the bull trigger

- RES 1: 4221.50 High Aug 22

- PRICE: 4161.00 @ 14:23 BST Aug 25

- SUP 1: 4085.13 50-day EMA

- SUP 2: 4000.00 Round number support

- SUP 3: 3994.50 Low Jul 28

- SUP 4: 3913.25 Low Jul 26 and a key support

The S&P E-Minis contract remains vulnerable following recent weakness. The move lower is allowing an overbought reading in momentum studies to unwind. The 20-day EMA has been breached and attention is on the 50-day EMA, at 4085.13 - a key pivot support. Key resistance and the bull trigger is at 4327.50, the Aug 16 high. Initial resistance to watch is at 4221.50, Monday’s high. A break would ease the current bearish threat.

COMMODITIES: Crude Oil Slides Despite OPEC Willingness To Cut Production

- Crude oil more than unwinds yesterday’s gains, despite OPEC noting openness to cutting oil production, with declines gaining through the US session despite limited drivers. Product prices meanwhile face further pressure after a fire at the biggest US Midwest refinery broke out with BP still working to assess the damage and determine when it could restart.

- WTI is -1.95% at $93.05, in a sharp pullback from the week’s gains improving the short-term outlook for bulls having traded through key resistance. Instead, it now moves closer to support at $90.42 (Aug 23 low), after which sits the bear trigger at $85.37 (Aug 16 low).

- Brent is -1.23% at $99.98, again moving closer to support at $96.53 (Aug 23 low) with the bear trigger at $91.22 (Jul 14 low) below that.

- Gold is +0.27% at $1755.86, continuing gains from the past two days on a softer USD and Treasury yields ahead of Jackson Hole. It briefly cleared the 20-day EMA at $1762.2 before retreating, but opens the 50-day EMA at $1777.2.

Friday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 26/08/2022 | 0600/0800 | * |  | DE | GFK Consumer Climate |

| 26/08/2022 | 0600/0800 | ** |  | SE | Unemployment |

| 26/08/2022 | 0600/0800 | ** | | SE | PPI |

| 26/08/2022 | 0645/0845 | ** |  | FR | Consumer Sentiment |

| 26/08/2022 | 0800/1000 | ** |  | IT | ISTAT Business Confidence |

| 26/08/2022 | 0800/1000 | ** | | IT | ISTAT Consumer Confidence |

| 26/08/2022 | 0800/1000 | ** |  | EU | M3 |

| 26/08/2022 | 1230/0830 | ** |  | US | Personal Income and Consumption |

| 26/08/2022 | 1230/0830 | ** | | US | Advance Trade, Advance Business Inventories |

| 26/08/2022 | 1400/1000 | *** | | US | Final Michigan Sentiment Index |

| 26/08/2022 | 1400/1000 | | US | Fed Chair Jerome Powell at Jackson Hole | |

| 26/08/2022 | 1500/1100 |  | CA | Finance Dept monthly Fiscal Monitor (expected) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.