Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- US SEPT. UNEMPLOYMENT RATE FALLS TO 3.5% VS 3.7%

- NY Fed WILLIAMS: FED NEEDS TO RAISE RATES TO AROUND 4.5% OVER TIME

- Atlanta Fed GDPNow Q3 estimate up a couple tenths to 2.9%

- Nagel: ECB Rates Must Rise Significantly

US TSYS: Focus Turns to Next Wk's CPI, Sep FOMC Minutes

Tsy futures remain weaker after the bell, off lows after September employment data came out slightly better than expected w/ jobs gain of +263k vs. +255k est, August up-revision by +11k.

- Yield curves bear steepened (2s10s climbed to -40.616) as focus turned to drop in participation rate and unemployment as traders anticipate more rate hikes into 2023. Stocks not taking the data positively either, SPX eminis falling to late session low of 3643.75.

- Tsys held the lower range as desks turn focus on next week Thursday's CPI (0.2% MoM est, 8.1% YoY est) for next inflation metric. Sep FOMC minutes release on Wednesday at 1400ET.

- Earlier Fed speak underscored the hawkish tempo, NY Fed Williams said need to raise rate to around 4.5% "over time" citing strong jobs market. Williams added he does expect to see inflation "down significantly next year."

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N +0.00758 to 3.06629% (+0.00115/wk)

- 1M +0.01328 to 3.31357% (+0.17086/wk)

- 3M +0.08300 to 3.90871% (+0.15400/wk) * / **

- 6M +0.07714 to 4.38471% (+0.15271/wk)

- 12M +0.11158 to 4.99629% (+0.21572/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 3.90871% on 10/07/22

- Daily Effective Fed Funds Rate: 3.08% volume: $109B

- Daily Overnight Bank Funding Rate: 3.07% volume: $282B

- Secured Overnight Financing Rate (SOFR): 3.05%, $985B

- Broad General Collateral Rate (BGCR): 3.00%, $399B

- Tri-Party General Collateral Rate (TGCR): 3.00%, $375B

- (rate, volume levels reflect prior session)

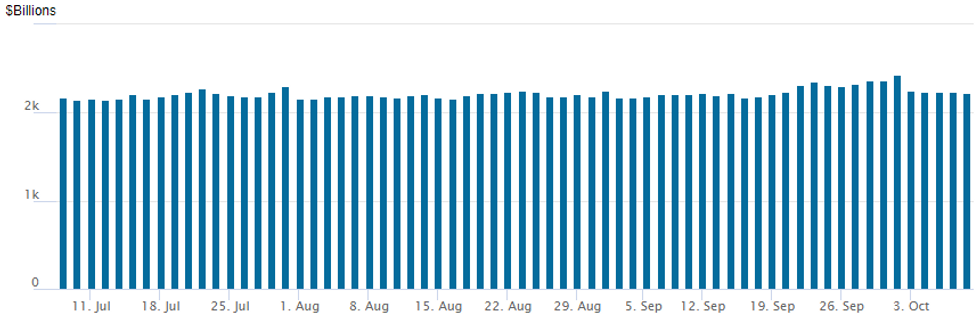

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $2,226.950B w/ 101 counterparties vs. $2,232.801B in the prior session. Recent record high stands at $2,425.910B on Friday, September 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

- SOFR Options:

- Block, 10,000 SFRZ2 95.87/96.18 call spds 1.25 over 94.56/95.12 put spds

- Block, 5,000 SFRZ2 95.87/96.31 call spds, 4.0 ref 95.555

- Block, 4,000 SFRX2 95.37/95.50/95.62 put trees, 1.75

- Block, 7,500 SFRZ2 95.25/95.50 put spds, 8.0 vs. 95.56

- Block, 5,000 SFRX2 95.25/95.50 put spds, 7.0 vs. 95.55

- Block, 3,000 short Mar 95.00/95.25 put spds, 6.0 vs. 95.875/0.07%

- 12,250 SFRH3 96.50/97.00 call spds ref 95.425

- 8,000 SFRF3 95.00/95.12 put spds, ref 95.45

- Eurodollar Options:

- 1,500 long Green Dec'24 98.00/99.00/99.50 broken call flys

- 5,000 short Dec 95.62 calls, 8.0

- Treasury Options:

- 10,000 USZ2 160 calls, 1 ref 125-16

- 2,000 TYZ2 114/116/118 call trees, 13

- 2,500 FVX2 116.5 puts

- 3,500 TYZ 111 puts, 121 ref 111-14.5

- total 7,200 TYX2 113 calls, 16

- 4,000 FVZ2104.5/106 put spds 22.5

- 6,800 TYX2 114.5 calls, 5

- -1,500 TYZ2 112.5 calls, 105

- Block, 7,500 TYX2 109.5 puts 16, 111.5 puts 56

- 6,000 TYZ2 119 calls, 5 ref 111-16

- Block, 9,000 wk1 TY 110.75/111.25 put spds 8 ref 111-24.5

- 8,000 TYZ 111.5 puts, 132

- Block, 1,250 FVZ2 106.75/107.5/107.75 put trees on a 8x3x3 ratio

- 5,000 FVZ2 106.75 puts, 58.5 ref 107-04.5

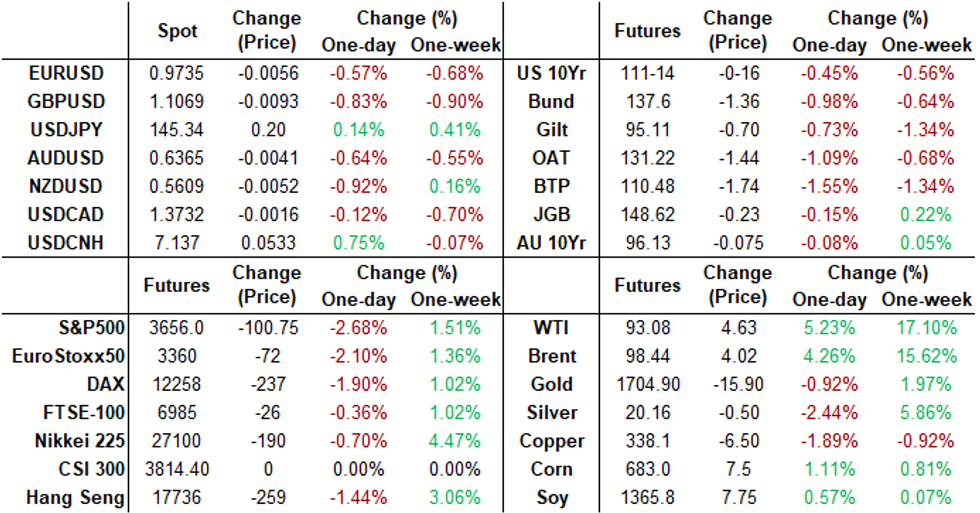

FOREX: USD Edges Higher For Third Consecutive Session Following NFP

- Despite the sharp moves seen in equity indices and oil prices, currencies traded in a less volatile manner on Friday after the greenback was given a firm boost following the release of September jobs data for the US.

- The USD Index (+0.28%) looks set to post a positive week after rising for a third successive session amid surging US yields on the back of the employment report.

- With risk sentiment under significant pressure, GBP (-0.62%) and NZD (0.80%) were the weakest performers, however, losses/ranges were more contained compared to prior sessions this week.

- EURUSD has faded further off the bear channel top throughout Friday trade, erasing the entirety of the mid-week rally and briefly trading below the Sep 30 low of 0.9735.

- A significant 4% extension of the rally in crude futures underpinned CAD and NOK outperformance as general bullish sentiment after the OPEC+ cut this week was reinforced.

- Worth noting that Japanese markets will be closed on Monday owing to observance of the Health Sports Day national holiday. Additionally, US Columbus Day and Canada Thanksgiving Holiday may see a relatively quiet start to next week.

- Wednesday will see the release of the FOMC minutes before Thursday’s important release of US CPI for September.

FX Expiries for Oct10 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9800-10(E1.6bln), $0.9844-45(E1.1bln), $0.9875(E556mln), $0.9950(E709mln), $1.0050(E2.4bln)

- USD/JPY: Y145.00($672mln), Y147.35($779mln)

- EUR/JPY: Y144.00(E848mln)

- AUD/USD: $0.6560(A$616mln)

Late Equity Roundup: Extending Lows, IT Weighing

Stock indexes gradually extending losses in late trade, early support sapped after better than expected Sep NFP data underscored Fed's likely hawkish forward policy path. Information Technology, Consumer Discretionary and Communication Services underperforming. Currently, SPX eminis trade -106 (-2.82%) at 3650.5; DJIA -664.75 (-2.22%) at 29261.17; Nasdaq -407.9 (-3.7%) at 10665.29.

- SPX leading/lagging sectors: Information Technology sector extend losses (-4.21%) as semiconductors, hardware makers, software and services reversed prior session gains (AMD -12.66%, MPWR -9.14$, NVDA -7.63%). Consumer Discretionary (-3.64%) and Communication Services (-2.75%) follow, auto makers weighing on the former, Tesla -6.05%. Leaders: Energy sector shares outperforming (-0.14%) oil/gas names doing well as crude remains strong (WTI +4.26 at 92.71). Consumer Staples (-1.47%) and Industrial (-2.08%) sectors followed.

- Dow Industrials Leaders/Laggers: Merck (MRK) -0.18 at 87.26, Chevron (CVX) reverses earlier gains -0.32 at 161.10, Verizon (VZ) -0.79 at 37.05. Laggers: United Health (UNH) -17.27 at 501.86, Microsoft (MSFT) -12.54 at 234.25, Home Depot (HD) -6.48 at 283.91.

Oil Surges As Disconnect With Equities Grows

- Crude oil prices have surged further today for an extremely strong week that has been dominated by the OPEC+ decision to cut 2mbpd from its output starting November and potential further cuts from Russian production. There are fewer obvious factors for today’s further rise, although a lack of US action could be at play, with oil increasingly seeing a disconnect with equities.

- WTI is +4.8% at $92.64, having cleared multiple resistance levels, the latest being $92.26 (Aug 30 high), opening key resistance at $96.82.

- Brent is +3.7% at $97.9 having cleared two resistance levels to open key resistance at $101.88 (Jul 29 high).

- Gold is -0.8% at $1698.86 as it slips on USD strength & higher yields following lower than expected US unemployment keeping the pressure on the Fed to hike aggressively. It earlier cleared support at $1695.2 (former trendline resistance) to open $1659.7 (Oct 3 low).

- Weekly moves: WTI +16%, Brent +11%, Gold +2.3%, US nat gas 0%, EU nat gas -17%

Monday-Tuesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 10/10/2022 | 0600/0800 | * |  | NO | CPI Norway |

| 10/10/2022 | 0830/1030 | * |  | EU | Sentix Economic Index |

| 10/10/2022 | 1200/0800 |  | US | Chicago Fed's Charles Evans | |

| 10/10/2022 | - | | EU | ECB Lagarde at IMF/World Bank Annual Meetings | |

| 10/10/2022 | 1300/1500 | | EU | ECB Lane Opens ECB Monetary Policy Conference | |

| 10/10/2022 | 1500/1100 | ** | | US | NY Fed survey of consumer expectations |

| 10/10/2022 | 1735/1335 | | US | Fed Vice Chair Lael Brainard | |

| 11/10/2022 | 2145/1045 | ** |  | NZ | Electronic card transactions m/m |

| 11/10/2022 | 2301/0001 | * |  | UK | BRC-KPMG Shop Sales Monitor |

| 11/10/2022 | 2330/1030 |  | AU | Westpac-MI Consumer Sentiment | |

| 11/10/2022 | 0030/1130 | | AU | NAB Business Survey | |

| 11/10/2022 | 0600/0700 | *** | | UK | Labour Market Survey |

| 11/10/2022 | 0800/1000 | * |  | IT | Industrial Production |

| 11/10/2022 | 0900/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 11/10/2022 | 1000/0600 | ** | | US | NFIB Small Business Optimism Index |

| 11/10/2022 | - | | EU | ECB Panetta IMF/World Bank Annual Meetings | |

| 11/10/2022 | 1245/1445 | | EU | ECB Lane Keynote Speech | |

| 11/10/2022 | 1400/1000 | ** | | US | IBD/TIPP Optimism Index |

| 11/10/2022 | 1530/1130 | | US | Philadelphia Fed's Patrick Harker | |

| 11/10/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 11/10/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 11/10/2022 | 1600/1200 | | US | Cleveland Fed's Loretta Mester | |

| 11/10/2022 | 1700/1300 | *** | | US | US Note 03 Year Treasury Auction Result |

| 11/10/2022 | 1800/1900 | | UK | BOE Cunliffe Panels IIF Annual Meeting | |

| 11/10/2022 | 1800/2000 | | EU | ECB Lane NY Fed Fireside Chat | |

| 11/10/2022 | 1835/1935 | | UK | BOE Bailey in Conversation w. Tim Adams at IIF Meeting |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.