Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

MNI US-CHINA: FT: Move To Open Lines Of Communication Signals "Major Breakthrough"

MNI US: Biden's Handling Of The Economy Remains Primary Concern For Voters

OPEC+ JMMC RECOMMENDS NO CHANGE IN OIL OUTPUT POLICY: DELEGATE

MNI SECURITY: Ukraine Warns Of 'False Flag' To Draw Belarus Into Conflict

MNI JAPAN: PM Kishida Undecided On Snap Election Or Cabinet Reshuffle

Key Links:MNI INTERVIEW: US Labor Market Surpasses Pre-Pandemic Strength / MNI GLOBAL WEEK AHEAD: Chinese Data Drop Raises Focus on Stimulus Hopes / MNI Fed Balance Sheet Tracker - Aug 4, 2023 / MNI TV: Key Exclusive Highlights For Week 31 / MNI EGB Issuance, Redemption and Cash Flow Matrix - W/C Aug 7

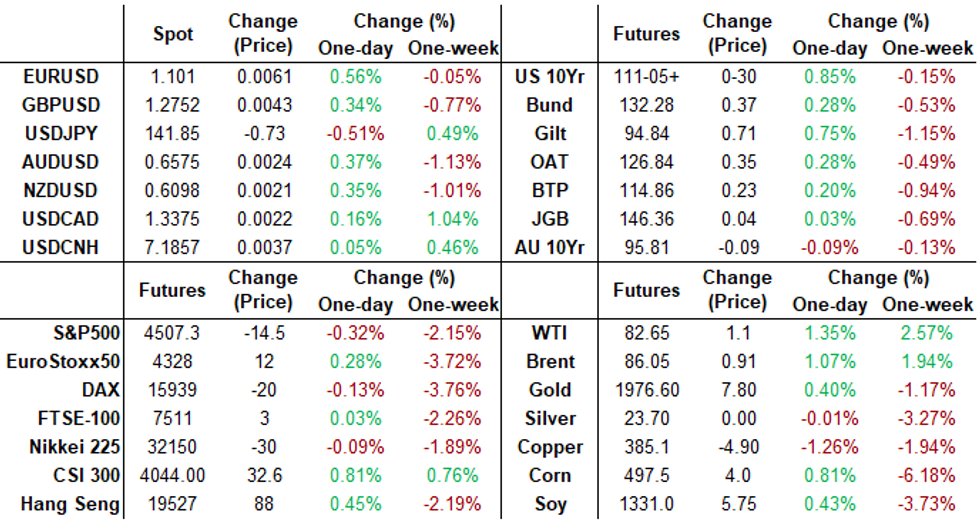

US TSYS Bonds Extending Late Highs

- After briefly paring post-NFP highs at midmorning, Tsy futures continued to extend session highs into the close, curves bull flattening/unwinding some of Thu's move (3M10Y -12.886 at -136.364; 2Y10Y -3.107 at -73.910) with intermediate to long end rates outperforming (USU3 +2.05 at 128-09, 30YY 4.1997% low).

- Fast two-way trade was reported after this morning's July employment data came out slightly lower than expected at +187k vs. 200k est, June down-revised by -49,000. Average hourly earnings, on the other hand, were stronger than expected, rising 0.42% M/M (cons 0.3) after an upward revised 0.45% (initial 0.36% M/M) which was only marginally offset by a lower 0.33% in May (initial 0.36%).

- Rates continued to angle higher amid dovish comments from unscheduled Fed speakers Bostic "US JOBS NUMBERS CAME IN AS EXPECTED; I'M COMFORTABLE" and Goolsbee "SHOULD START THINKING ABOUT HOW LONG TO HOLD RATES" underscoring, if not exactly providing a bid to the rally.

- Cross-asset gains at midday: stocks near highs (ESU3 +28.0 at 4550.0; Crude firm (WTI +1.05 at 82.60), Gold firmer (+8.65 at 1942.7.

- Slow start to next week's data with the first significant release next Thursday with CPI and weekly Claims.

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.00084 to 5.31724 (-.00083/wk)

- 3M +0.00073 to 5.37058 (-0.00133/wk)

- 6M +0.00112 to 5.43419 (-0.01382/wk)

- 12M -0.00252 to 5.36235 (-0.04553/wk)

- Daily Effective Fed Funds Rate: 5.33% volume: $105B

- Daily Overnight Bank Funding Rate: 5.32% volume: $263B

- Secured Overnight Financing Rate (SOFR): 5.30%, $1.413T

- Broad General Collateral Rate (BGCR): 5.28%, $579B

- Tri-Party General Collateral Rate (TGCR): 5.28%, $572B

- (rate, volume levels reflect prior session)

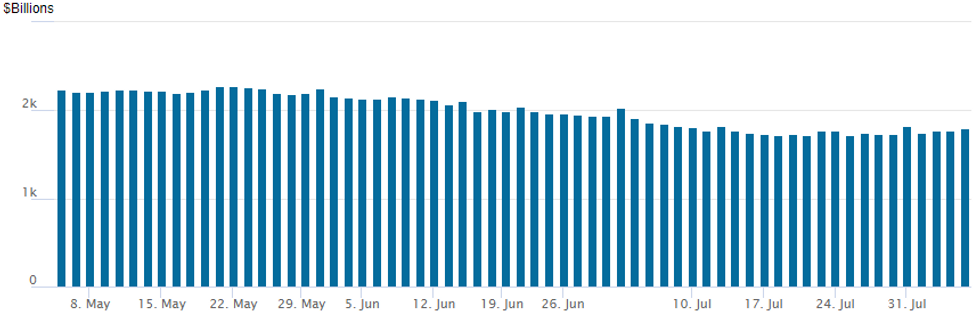

FED REVERSE REPO OPERATION

NY Federal Reserve/MNI

The latest operation inches up to $1,793.804B, w/102 counterparties, compared to $1,776.774B in the prior session. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

SOFR/TREASURY OPTION SUMMARY

Option desks reported two-way put trade in SOFR and Treasury options Friday. Better SOFR put buying was noted prior to the July employment data as accounts hedged a gradual increase in rate hike projections. Looking past the stronger than expected AHE data (4.361% in Jul from 4.413% in Jun), the lower than expected (but still solid) job gain of +187k vs. +200k est. spurred a strong rally in underlying futures. In turn, rate hike projections declined, spurring various put unwinds or repositioning to higher strikes. Fed funds: Sep 20 FOMC is 13% vs. 17% w/ implied rate change of +3.2bp to 5.360%. November cumulative of +8bp at 5.407, December cumulative of 3.8bp at 5.3667%. Fed terminal slips to 5.405% in Nov'23. Salient trade includes:

- SOFR Options:

- -10,000 SFRZ3 94.25 puts, 3.5 ref 94.625

- 5,000 SFRZ3 96.00/96.50 call spds ref 94.60

- 2,000 SFRV3 94.37 puts, 4.5 ref 94.595

- Block 2,500 SFRM4 94.37/94.50 put spds 4.0 vs. 95.10/0.05%

- Block/screen, 20,000 SFRV3 94.50 puts, 7.5 vs. 94.625/0.35%

- 20,400 SFRZ3 95.50/96.50 call spds ref 94.60

- 28,000 OQZ3 95.75 puts, 35.5-36.5 ref 95.83 to -.81

- 1,000 SFRH4 94.37/94.62/94.87 put flys ref 94.84

- 6,500 SFRQ3 94.43/94.56 put spds, ref 94.59

- Treasury Options:

- 2,500 TYU3 109.5 puts vs. TYV3 114.5 calls, 6 net Oct over

- 20,000 wk3 TY 107.5/109 put spds 10-9 ref 110-16 to 110-26

- -15,000 TYU3 109/110 put spds 21 vs. 110-12 to -10.5/0.17%

- 5,000 FVU3 109 calls, 2.5 ref 106-09.25

- -7,000 FVU 106.25/106.5 put spds, 8.5 ref 106-06.5

- 2,500 USU3 117/118.5 put spds 25 ref 120-17

- 3,000 TYU3 112 calls, 15 last ref 110-04.5

- 2,500 FVU3 109 calls ref 106-07

- 2,100 wk1 TY 109.75 puts, 6 ref 110=07

- Block, 4,000 wk1 TY 110.5/111 call spds 7 vs. wk2 TY 111/111.5 call spds 8

EGBs-GILTS CASH CLOSE: Soft US Jobs Growth Triggers Bull Flattening

European curves bull flattened Friday, with yields pulling back from recent extremes after US employment data was seen to be on the soft side.

- An early upside surprise in German factory orders helped extend the bearish tone of the previous two sessions (which had centred around US Treasury supply expectations), but the space rallied in the early afternoon after US nonfarm payroll growth came in below expectations.

- The standout moves were in the UK curve with yields down by high-single digits in a bull flattening move; the German curve moved accordingly but with a less pronounced yield drop.

- Commentary by BoE Pill didn't move the needle, with the Chief Economist reiterating that rates are not on a pre-set course.

- Greek spreads outperformed a broader periphery rally, with DBRS Morningstar noting that Greece is close to receiving investment grade status, while Scope Ratings' reviews the sovereign after market close today.

- Next week is a quieter one on the European calendar, with Monday's highlights including German industrial production data and another appearance by BoE's Pill.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.1bps at 3.014%, 5-Yr is down 2.3bps at 2.581%, 10-Yr is down 4.3bps at 2.562%, and 30-Yr is down 6.3bps at 2.624%.

- UK: The 2-Yr yield is down 6bps at 4.92%, 5-Yr is down 6.7bps at 4.402%, 10-Yr is down 9bps at 4.38%, and 30-Yr is down 8.6bps at 4.569%.

- Italian BTP spread down 1.9bps at 165bps / Greek down 4.7bps at 122.6bps

EGB Options: OTM Bund Put Buying Continues

Friday's Europe rates / bond options flow included:

- RXX3 127p bought for 78, 80 and 81 in 4k total now. Yesterday, saw a RXV3 126/124 ps, bought for 13.5 in 5k.The 125.00 strike would equate to 3.22% in 10yr Yield, last traded in 2010.

- ERU3 96.37/96.25/96.00p fly, bought for 1.75 in 2.5k

- ERV3 96.12^, sold down to 20.5 in 3k

FOREX Greenback Snaps Winning Streak as NFP Undermines Uptrend

- The greenback snapped the winning streak Friday, with the uptrend in the USD Index undermined by the July Nonfarm Payrolls release. A poorer-than-expected headline and negative revisions plus softer hours worked countered any hawkish overtones from strong AHE and the drop in the unemployment rate. The release, compounded with the recent pullback in CPI inflation, has helped ease market-implied peak pricing at the Fed in November by ~4bps off the day's high, weighing on yields and helping support equities. That was until a late slide in US stocks, seemingly flow- rather than headline-driven ahead of the weekend, which has provided a small uplift for the USD index but with DXY still -0.6% on the day.

- The USD pullback helped prompt a corrective recovery in EUR/USD, which rallied to touch 1.1042 and clear the Wednesday high in the process. This cements the 50- and 100-dmas as key supports, which have held well this week at 1.0937 and 1.0920 respectively.

- A firmer oil price into the close has favoured oil-tied FX, putting NOK at the top of the G10 pile, although CAD underperforms notably on US linkages and its own softer jobs print. The moves in NOK come ahead of next week's July CPI report, at which markets expect the Norges Bank's favoured inflation gauge - CPI-ATE - to ease off a cycle high of 7.0%. Continued stubbornness in inflation would work against any expectations that the bank can revert to 25bps hikes at the August rate decision.

- Focus in the coming week turns to global inflation, with US, Norway and China all posting their latest CPI prints. The Banxico decision is also due, with the bank seen standing out from regional peers by keeping the overnight rate unchanged.

FX Expiries for Aug07 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0920-40(E1.4bln)

- USD/JPY: Y141.50($590mln), Y142.00($500mln), Y143.00($792mln), Y145.00($998mln)

- EUR/GBP: Gbp0.8550(E1.0bln)

- AUD/USD: $0.6500(A$585mln)

Late Equities Roundup: Reversing Early Gains

- Late session position squaring/profit taking ahead the weekend, not to mention a 1000+ name sell program has stocks inching back near opening levels recently. Currently, DJIA shares are down -56.97 points (-0.16%) at 35157.1, S&P E-Mini futures down 9.5 points (-0.21%) at 4511.75, Nasdaq up 14.9 points (0.1%) at 13973.58.

- Leading gainers: Consumer Discretionary, Energy and Materials sector shares continue to outperform but have scaled back support over the last couple hours. Discretionary shares weren't led by autos this time but by retailers including Amazon +9.55% in carry over bid from late Thu after blowout positive earnings and rosy forward guidance. Energy gained as crude prices climbed higher (WTI +1.35 at 82.90), Occidental Petroleum +3.15%, Targa Resources +2.85%, Pioneer Natural Resources +2.3%. Reminder, crude rallied Thursday after headline "SAUDI TO EXTEND VOLUNTARY CUT OF 1M B/D THROUGH SEPT".

- Laggers: Utilities, Information Technology and Real Estate sectors underperformed. Utiities weighed by independent power/renewable energy shares AES -4.26%, while Dominion fell 3.25%. Hardware and equipment makers weighed on IT: Fotinet down a whopping 24.3% after beating earnings but missing sales and downgrading forward guidance. Meanwhile, Palo Alto Networks -7.86%, Microchip Tech -7.37%, Apple -3.75%.

- Technicals: E-mini S&P contract continues to trade below 4634.50, the Jul 27 high. This week’s move lower reinforces a bearish theme and has resulted in a break of support around the 20-day EMA. The recent failure at the top of the bull channel and the break of the 20-day average, highlights a developing bearish threat. A continuation lower would open 4452.13, the 50-day EMA. First key resistance is at 4634.50, the Jul 27 high.

E-MINI S&P TECHS: (U3) Bear Cycle Still In Play

- RES 4: 4715.86 3.0% 10-dma envelope

- RES 3: 4670.25 2.00 proj of the Jun 26 - 20 - Jul 7 price swing

- RES 2: 4665.19 Bull channel top

- RES 1: 4593.50/4634.50 High Aug 2 / Jul 27

- PRICE: 4508.75 @ 1440ET Aug 4

- SUP 1: 4505.75 Low Aug 3

- SUP 2: 4470.00 Low Jul 12

- SUP 3: 4452.13 50-day EMA

- SUP 4: 4418.60 Bull channel base drawn from the Mar 13 low

The E-mini S&P contract continues to trade below 4634.50, the Jul 27 high. This week’s move lower reinforces a bearish theme and has resulted in a break of support around the 20-day EMA. The recent failure at the top of the bull channel and the break of the 20-day average, highlights a developing bearish threat. A continuation lower would open 4452.13, the 50-day EMA. First key resistance is at 4634.50, the Jul 27 high.

COMMODITIES Crude Extend Gains With USD Tailwind After Saudi And Russia Production Cut Extension

- Crude oil has extended yesterday’s bounce, with the latest move supported by USD depreciation after the payrolls report (with a late lift in the USD index also taking the edge of crude gains) and yesterday’s announcement of Saudi and Russian cut extensions into September continuing to have an impact.

- There was little reaction to OPEC’s JMMC recommended no change to the group’s current output policy during today’s meeting, widely expected by the market.

- Russia is fully adherent to the OPEC+ deal to reduce output by 500kbpd, while the country has exceeded cuts of 500kbpd in June, Russian Deputy PM Alexander Novak said. Along with the rally in Brent on tightening supplies, key physical crude market indicators in Asia have also strengthened further after Saudi Arabia and Russia extended voluntary supply cuts.

- WTI is +1.5% at $82.80 off a high of $83.22 that moved closer to resistance at $83.59 (Nov 7, 2022 high) having already set fresh YTD highs earlier in the week.

- Brent is +1.3% at $86.20 after a high of $86.63 cleared a key resistance level at $86.18 to open the psychological $90/bbl.

- Gold is +0.3% at $1940.49, benefiting from the softer USD but a surprisingly tame move considering the extent of the slide in Treasury yields as well. It doesn’t trouble resistance at $1972.4 (Jul 31 high).

- Weekly moves: WTI +2.8%, Brent +1.5%, Gold -1.0%, US nat gas -2.4%, EU TTF nat gas +11.7%

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 07/08/2023 | 0545/0745 | ** |  | CH | Unemployment |

| 07/08/2023 | 0600/0800 | ** |  | DE | Industrial Production |

| 07/08/2023 | 1230/0830 |  | US | Fed's Michelle Bowman, Raphael Bostic | |

| 07/08/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 07/08/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 07/08/2023 | 1600/1700 |  | UK | BOE Pill speaks at the MPR Live Q&A | |

| 07/08/2023 | 1900/1500 | * | | US | Consumer Credit |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.