Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

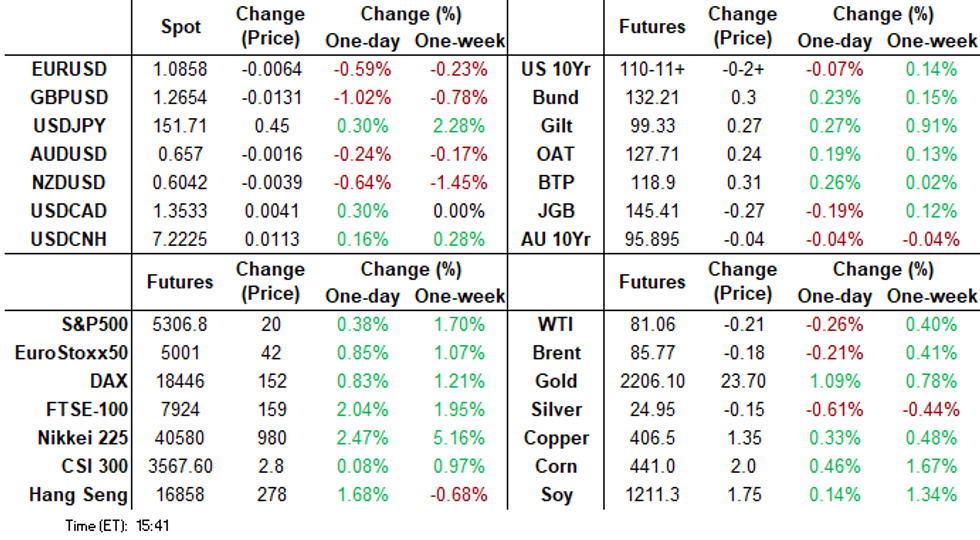

- Treasury support ebbed as Thursday's data tempered post-FOMC rate cut projections.

- Ironically, S&P Eminis climbed to new all-time highs despite the inflationary build flash PMI manufacturing.

- USD index trading back through the pre-FOMC levels and extending above 104 in late trade.

US TSYS: Data Dependent

- Treasury futures look to finish mixed Thursday with 2s-10s weaker, curves unwinding a good portion of the post FOMC steepening as today's data tempered post-FOMC rate cut projections.

- Rates actually opened stronger across the board, extending gains after the bank of England delivered a dovish hold policy announcement this morning. Short end support evaporated in stages, initially on slightly lower than estimated weekly jobless claims data: 210k vs. 213k est (prior up-revised to 212k from 209k, however).

- Treasury futures gapped lower after the S&P Global US PMI releases saw manufacturing beat (52.5 vs cons 51.8 after 52.2) but services miss (51.7 vs cons 52.0 after 52.3) in the preliminary March PMI. Overall input cost inflation hit a six-month high. “Service providers indicated that higher operating expenses generally reflected increasing wages, while rising oil and gasoline costs were often mentioned by manufacturers."

- After the flash data, Treasuries traded sideways through the rest of the session, Jun'24 10Y futures -3 at 110-11 vs. 110-08.5L/110-26.5H, 2s10s curve -3.603 at -36.766. Moving average studies are in a bear-mode position and this highlights a downtrend. Key short-term resistance to watch is 111-01+, the 50-day EMA. A clear break of this average is required to suggest scope for a stronger recovery. On the downside, the bear trigger lies at 109-24+.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M +0.00059 to 5.32941 (+0.00066/wk)

- 3M -0.00853 to 5.31996 (-0.01252/wk)

- 6M -0.02582 to 5.24578 (-0.02936/wk)

- 12M -0.04276 to 5.03684 (-0.04175/wk)

- Secured Overnight Financing Rate (SOFR): 5.31% (+0.00), volume: $1.736T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $685B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $673B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $91B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $248B

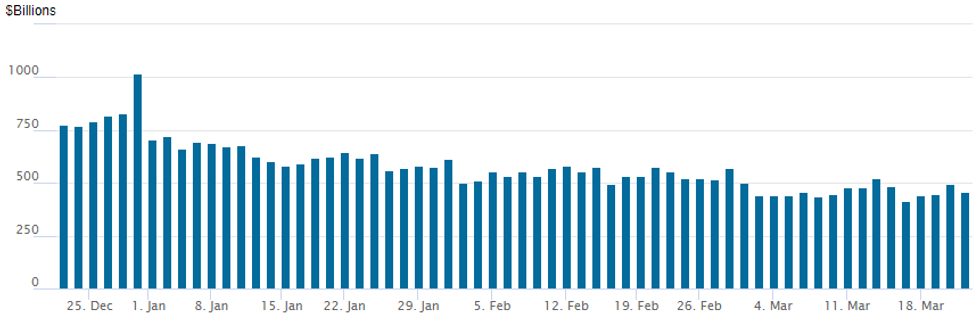

FED Reverse Repo Operation

NY Federal Reserve/MNI

- RRP usage recedes to $460.631B after a potential influx of GSE flows saw usage jump to $496.245B yesterday. Last Friday saw usage fall to $413.877B - the lowest level since May 2021.

- Meanwhile, the latest number of counterparties slips to 74 vs. 78 yesterday (compares to 65 on January 16, the lowest since July 7, 2021)

SOFR/TEASURY OPTION SUMMARY

SOFR and Treasury option trade segued from near pared to better bearish hedging by late morning Thursday, predominantly via put buying but also unwinds of upside call positions as underlying futures traded weaker on data (higher than expected flash manufacturing PMI). A notable exception was a large 10Y weekly midcurve call bought ahead the open - that was followed by a large at-the-money put buy in the first half. Both expire on April 12, covering the next employment report on April 5, CPI on April 10 and PPI the day after. Meanwhile, projected rate cut pricing has receded in the near term: May 2024 at -12.4% vs -14.5% late Wednesday w/ cumulative -3.1bp at 5.297%; June 2024 -66.8% vs. -69.5% earlier w/ cumulative rate cut -19.8bp at 5.130%. July'24 cumulative at -31.0bp vs -32.5bp earlier.

- SOFR Options:

- -20,000 SFRJ4 95.00/95.25 put spds, 24.0 ref 94.89

- 10,000 SFRM4 94.75/94.81/94.87 put flys ref 94.895 to -.89

- Block, 5,000 SFRU4 94.62 puts, 2.0 ref 95.20

- Block/screen: 37,500 SFRM5 95.37/95.87/96.37 put flys, 10.0-10.5 ref 95.985

- +10,000 SFRM4 94.68/94.75/94.81 put flys, 0.5

- Block, 15,000 SFRU4 94.62 puts, 2.0 ref 95.195

- +13,000 SFRK4/SFRM4 94.93 put spds, 1.75

- 4,000 SFRZ4 95.00/95.37/95.75 put flys

- Block, 5,000 SFRM5 95.37/95.87/96.37put flys, 10.0 ref 95.985

- Block, total 10,000 SFRZ4 95.00/95.25/95.50 put flys, 4.5

- Block, 12,000 SFRJ4 95.37/95.12 call spds, 0.5 ref 94.905

- +4,500 SFRJ4 94.81/94.87 2x1 put spds 0.75

- 4,000 SFRZ4 94.50 puts, ref 95.535

- 2,000 SFRU4 95.50/95.68/96.18/96.37 call condors ref 95.21

- 2,500 SFRM4 94.87/95.00/95.12 call flys, ref 94.905

- Treasury Options:

- -10,000 TYK4 112 calls, 16

- +50,000 wk2 TY 110.50 puts, 42 vs. 110-18/0.46%

- +50,000 wk2 TY 110.75 calls, 42 vs. 110-23/0.50%

- 2,000 wk5 10Y 110/111 strangles, 19 ref 110-22

- 2,000 SFJ4/FVK4 106.75 put spds

- over 8,600 TYJ4 109.75 puts, 2 ref 110-14 to -13.5

- 1,500 TYK4 109 puts, 19 ref 110-14.5

- 1,500 FVK4 107 calls, 33.5 ref 106-31

EGBs-GILTS CASH CLOSE: Core FI Gains On Dovish Central Bank Developments

Short-end UK instruments outperformed German counterparts Thursday following a dovish BoE decision, but long-end Bunds outperformed Gilts.

- European FI started on the front foot following the dovish Fed late Wednesday, with further upside early in the session spurred by a surprise rate cut by the SNB and softer-than-expected Eurozone flash manufacturing data (UK PMIs were mixed and had little impact).

- The BoE decision brought a significant dovish shift, including no more hawkish dissenters, and Gilts hit session highs.

- In the afternoon, gains retraced as US data came in on the strong side and the US dollar and stocks strengthened.

- The UK curve twist steepened on the day, with Germany's bull steepening. Periphery spreads tightened, but closed off intraday tights.

- Friday's schedule includes UK retail sales and German IFO data, with multiple ECB speakers including Nagel, Holzmann, and Lane.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 5bps at 2.875%, 5-Yr is down 4.1bps at 2.405%, 10-Yr is down 2.7bps at 2.405%, and 30-Yr is down 1.1bps at 2.578%.

- UK: The 2-Yr yield is down 5.6bps at 4.178%, 5-Yr is down 3.7bps at 3.878%, 10-Yr is down 2.1bps at 3.995%, and 30-Yr is up 1.4bps at 4.493%.

- Italian BTP spread down 1.1bps at 127bps / Spanish down 0.9bps at 80.6bps

EGB Options: Volatility Plays Feature Thursday

Thursday's Europe rates/bond options flow included:

- ERH5 97.25^ trades 70.25 in 7k

- ERM4 96.25/96.00ps 1x2, bought for 3.25 in 6.5k

- ERN4 96.62/96.75/97.00/97.12c condor vs ERN4 96.37/96.12ps, bought the Condor for 2.75 in 4k

- SFIK4 94.95/94.85/94.75/94.65p condor bought for 1.75 in 5k

- SFIM4 95.20/95.35/95.50c fly, bought for 1.25 in 2k

- OEK4 117.00/118.50^^ sold at 46 in 2k

- OEK4 118.25/119.25cs 1x2, bought for 13 in 1.5k

- RXK4 134/136 call spread sold at 26 in 6k (ref 132.23, 16d)

FOREX Greenback Registers Post-FOMC Reversal Higher Amid Stronger-Than-Expected Data

- The greenback completed a V-shaped recovery on Thursday, with the USD index trading back through the pre-FOMC levels and extending above 104 in late trade.

- A dovish Swiss National Bank and Bank of England are providing significant headwinds for CHF (-1.25%) and GBP (-0.98%), the notable underperformers on the session, which are likely assisting the latest upswing for the dollar.

- In addition, firmer than expected US data is likely providing an additional greenback tailwind. Higher-than-expected Philly Fed business outlook and Manufacturing PMIs were then complemented by lower initial jobless claims and a jump in existing home sales, all underpinning the dollar bid.

- The close proximity of major resistance in USDJPY will likely continue to garner attention and could provide an obstacle for further protracted dollar strength as we approach the weekend.

- USDJPY extended the overnight recovery and tracks close to 151.70, now up 0.28% on the day. The cluster of significant resistance starts at yesterday’s highs of 151.82, which precedes the multi-decade highs at 151.91/95. Clearance of this resistance would confirm a resumption of the long-term USDJPY uptrend, with a break opening 152.66, a Fibonacci projection.

- Separately, AUD remains an outperformer following the strong post-holiday rebound in jobs, confirmed by data overnight. Earlier in the session, AUDJPY briefly printed above 100.00, a level that hasn’t traded since late 2014.

- Japan National core CPI crosses overnight on Friday, before UK retail sales headlines the European data docket.

FX Expiries for Mar22 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0800(E962mln), $1.0825-35(E2.3bln), $1.0850(E1.5bln), $1.0865-75(E1.8bln), $1.0890-05(E2.2bln), $1.0940-50(E1.1bln)

- USD/JPY: Y148.80-00($1.9bln), Y149.20-35($774mln), Y149.55($1.1bln), Y150.00($1.1bln), Y150.95-00($1.3bln), Y151.75($647mln)

- GBP/USD: $1.2675-90(Gbp798mln), $1.2750(Gbp547mln)

- AUD/USD: $0.6500(A$1.1bln), $0.6550(A$874mln), $0.6650(A$1.7bln), $0.6750(A$2.6bln), $0.6825(A$2.6bln)

- NZD/USD: $0.6050-60(N$1.8bln)

- USD/CAD: C$1.3350-70($1.7bln), C$1.3480-00($2.2bln), C$1.3510-20($765mln)

- USD/CNY: Cny7.1500($1.1bln), Cny7.2000($810mln), Cny7.2200($1.2bln)

Late Equities Roundup: Late Profit Taking

- Stocks are still bid but off midday highs in late trade, profit taking in IT stocks not surprising after S&P Eminis managed to climb to a new all-time high of 5322.75 earlier. Currently, S&P E-Minis trades up 18.5 points (0.35%) at 5304.75, Nasdaq up 37.1 points (0.2%) at 16406.99, the DJIA up 285.89 points (0.72%) at 39798.07.

- Leading Gainers: Industrials continued to lead while Financials outpaced the Information Technology sector in the second half. Construction and engineering shares continued to buoy Industrials: Stanley Black & Decker +3.32%, Masco Corp +3.0%, Pentair +2.76%. Banks led the Financials sector: Truist Financial +2.85%, Citizens Financial +2.15%, Comerica +2.11%.

- Laggers: Communication Services and Real Estate sectors underperformed in late trade, media shares weighed on the former with Paramount -4.64% after rallying over 11% Wednesday on $11B bid from Apollo for Hollywood Studios. Other laggers included Google -0.82% while Comcast slipped -0.90%. Real Estate investment trust weighed on the latter, particularly Health Care and Specialized REITs: Welltower -1.24%, Ventas -0.64%, Equinix -1.87%.

- Emini technicals: The trend condition in S&P E-Minis remains bullish and this week’s extension reinforces this theme. The break of 5257.25, Mar 8 high, confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. MA studies are in a bull-mode position reflecting positive market sentiment. Sights are on 5370.81, the top of a bull channel drawn from the Jan 17 low. Initial firm support is at 5185.88, the 20-day EMA.

E-MINI S&P TECHS: (M4) Fresh Cycle Highs

- RES 4: 5428.25 1.00 proj of the Oct 27 - Dec 28 - May 1 price swing

- RES 3: 5400.00 Round number resistance

- RES 2: 5370.81 Bull channel top drawn from the Jan 17 low

- RES 1: 5322.75 Intraday high

- PRICE: 5305.75 @ 1445 ET Mar 21

- SUP 1: 5209.19 Bull channel base drawn from the Jan 17 low

- SUP 2: 5185.88 20-day EMA

- SUP 3: 5073.80 50-day EMA

- SUP 4: 5018.00 Low Feb 21

The trend condition in S&P E-Minis remains bullish and this week’s extension reinforces this theme. The break of 5257.25, Mar 8 high, confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. MA studies are in a bull-mode position reflecting positive market sentiment. Sights are on 5370.81, the top of a bull channel drawn from the Jan 17 low. Initial firm support is at 5185.88, the 20-day EMA.

COMMODITIES Crude Retreats, Gold Sharply Pares Gains After Fresh All-Time High

- Crude markets are headed for the US close trading lower on Thursday, amid a strong recovery in the greenback following dovish European central banks and stronger-than-expected US data.

- WTI is down 0.3% on the day at $81.0/bbl.

- Last week’s gains and break of $79.87, the Mar 1 high, confirms a resumption of the uptrend that has been in place since mid-December last year. Sights are on $83.87 next, the Oct 20 ‘23 high. Support to watch is $79.08, the 20-day EMA.

- Spot gold is down 0.2% on Thursday to $2,182/oz, unwinding a rally earlier in the day which had taken the yellow metal to another all-time high at $2,221.

- The earlier rally confirms a resumption of the primary uptrend. Moving average studies remain in a bull-mode condition, reflecting positive market sentiment. This signals scope for a climb towards $2230.1, a Fibonacci projection. On the downside, key short-term trend support has been defined at $2146.2, the Mar 18 low.

- The recovery in the greenback also weighed on silver today, which fell by 3.2% to $24.77/oz.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 22/03/2024 | 0001/0001 | ** |  | UK | Gfk Monthly Consumer Confidence |

| 22/03/2024 | 0700/0700 | *** | | UK | Retail Sales |

| 22/03/2024 | 0700/0800 | ** |  | DE | Import/Export Prices |

| 22/03/2024 | 0730/0730 | | UK | DMO to release calendar for FQ1 (Apr-Jun) Ops | |

| 22/03/2024 | 0800/0900 |  | EU | ECB's Lagarde in Euro Summit | |

| 22/03/2024 | 0900/1000 | *** | | DE | IFO Business Climate Index |

| 22/03/2024 | 1100/1100 | ** | | UK | CBI Industrial Trends |

| 22/03/2024 | 1230/0830 | ** |  | CA | Retail Trade |

| 22/03/2024 | 1300/0900 |  | US | Fed Listens event | |

| 22/03/2024 | 1400/1500 | ** |  | BE | BNB Business Sentiment |

| 22/03/2024 | 1600/1200 | | US | Fed Vice Chair Michael Barr | |

| 22/03/2024 | 1630/1630 | | UK | BOE to announce APF sales schedule for Q2-24 | |

| 22/03/2024 | 1700/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

| 22/03/2024 | 1700/1800 | | EU | ECB's Lane lecture on inflation and MonPol at AMSE | |

| 22/03/2024 | 2000/1600 | | US | Atlanta Fed's Raphael Bostic |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.