Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI: FED NOT REALLY TALKING ABOUT RATE CUTS--WILLIAMS ON CNBC

- MNI US: US-Mexico Border Talks To Continue Through Weekend

- MNI: BOC’s Macklem Opens The Door To Rate-Cut Debate

- MNI SECURITY: Hapag-Lloyd Adds To Shipping Firms Suspending Red Sea Activities

- MNI US: Risk Of Government Shutdown In 2024 High, As Congress Winds Down 2023

- FRENCH PRES MACRON: HUNGARY DECIDED NOT TO BLOCK UNITY OF EU ON UKRAINE MEMBERSHIP, Bbg

- General Motors to Cut 1,314 Jobs at Two Michigan Plants Beginning Jan. 1, MT Newswire

Key Links: MNI INTERVIEW: Fed Could Cut Rates As Early As March-Hoenig / MNI INTERVIEW: Fed Could Cut More Than SEP Anticipates-Evans / MNI: BOC’s Macklem Opens The Door To Rate-Cut Debate / MNI GLOBAL WEEK AHEAD - BoJ Decision, UK CPI and EM CBs / MNI TV: Key Exclusive Highlights For Week 50

US TSYS Markets Roundup: NY Fed Williams Pushed Back on Rate Hike Projections

- Treasury futures looking mixed after the bell, the short end weaker after NY Fed President Williams pushed back on the markets dovish response to Wednesday's steady FOMC rate announcement.

- NY Fed Williams posited markets may have reacted to Wed's FOMC announcement "more strongly than forecasts show". Williams' comments on CNBC were actually not too far removed from what Powell said Wednesday.

- Futures held mixed levels after S&P Flash PMIs, long end still bid vs. weaker 2s-10s after lower than expected Manufacturing PMI (48.2 vs. 49.5 est, 49.4 prior) while Services and Composites come out stronger than expected: 51.3 vs 50.7 est and 551.0 vs. 50.5 est respectively.

- TYH4 112-15 (-1.5) at the moment, curves flatter (2Y10Y -7.342 at -54.296. Tsy 10Y futures still well within technical levels: resistance at 112-28.5 (1.618 proj of the Oct 19 - Nov 3 - Nov 13 price swing). Initial support well below at 111-09+ (High Dec 7 and a recent breakout level).

- Given the curve flattening, projected rate cuts for early 2024 consolidated vs. Thursday highs: January 2024 cumulative -3bp at 5.302%, March 2024 chance of rate cut -64.9% vs. -81.9% late Thursday w/ cumulative of -19.2bp at 5.14%, May 2024 chances -64.9% after fully pricing in the first full cut yesterday with cumulative -40.7bp at 4.926%, while June'24 slipped to -89% vs. -96.9%, cumulative -62.9bp at 4.703%. Fed terminal at 5.33% in Feb'24.

- Monday Data Calendar: Chicago Fed Goolsbee interview on CNBC at 0830, New York Fed Services Business Activity at 0830, NAHB Housing Market Index at 1000, while the US Tsy will auction $75B 13W, $68B 26W bills at 1130ET.

FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00250 to 5.35575 (-0.00428/wk)

- 3M -0.01375 to 5.36399 (-0.00205/wk)

- 6M -0.07394 to 5.21986 (-0.07225/wk)

- 12M -0.15681 to 4.85795 (-0.16217/wk)

- Secured Overnight Financing Rate (SOFR): 5.31% (+0.00), volume: $1.695T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $627B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $616B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $108B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $267B

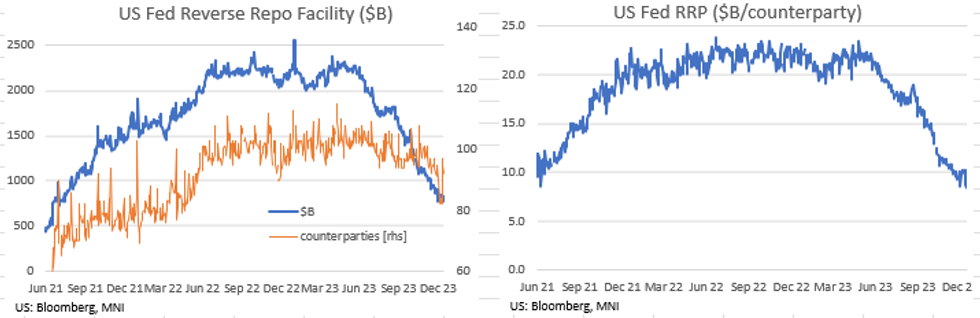

RRP USAGE Tumbles to Lowest Level Since Mid-June 2021

- RRP usage falls to the lowest level since mid-June 2021 this afternoon: $683.254B from -- $769.436B in the prior session and well below $768.543B on December 1.

- The number of counterparties has fallen to 82 from 92 in the prior session.

SOFR/TREASURY OPTION SUMMARY

Mixed overnight trade segued to downside put structures, unwinding calls as underlying futures trade weaker after NY Fed Williams pushed back on market pricing rate cuts in 2024. Projected rate cuts for early 2024 continue to consolidate: January 2024 cumulative -3bp at 5.302%, March 2024 chance of rate cut -65.8% vs. 76.5% earlier (-81.9% late Thursday) w/ cumulative of -19.5bp at 5.138%, May 2024 chances -82.9% vs. -92.3% earlier with cumulative -44.02bp at 4.931%, while June'24 slipped to -92.7% vs. -99.2%, cumulative -63.4bp at 4.699%. Fed terminal at 5.335% in Feb'24.- SOFR Options: (Dec options expire today)

- Block, 5,000 SFRZ4 96.50/97.00 call spds, 14.0 ref 96.135

- Block, 15,000 SFRM5 96.00/96.75 call spds, 39.0 ref 96.66

- -28,000 SFRU4 97.00/98.00 9.0 ref 95.78 (unwind after buying appr 50k from 5.75-6.0 starting Nov 21)

- over 17,000 SFRZ3 94.62 calls, cab

- Update, +40,000 SFRH4 94.62/94.68 put spds, 1.0

- -15,000 SFRF4 94.87/95.00/95.06 broken call flys, 3.5

- over 7,500 SFRM4 95.25 puts, mostly 24.5ref 95.325

- Block/update, total 7,500 SFRH4 94.93/95.06/95.18 call flys, 3.75

- Block, 5,000 SFRM4 95.75/96.00 call spds, 4.5 vs. 95.37/0.10%

- 3,500 SFRM4 95.00/96.00 2x3 call spds ref 95.405

- 3,000 SFRU4 95.00/95.25/95.50/95.75 put condors ref 95.825

- 5,000 SFRH4 94.62/94.75 put spds ref 94.925

- 4,000 2QZ4 96.75/98.00 call spds vs. 2QZ4 97.25/98.00 call spd

- 5,100 0QZ3 96.00 puts, 2.0 ref 96.115

- Treasury Options:

- 5,000 FVH4 108.5 calls, 60.5 ref 108-14.25

- 10,000 TYF4 114.75 calls, 2 ref 112-19.5

- Block, 11,000 TYH4 110 puts, 33 ref 112-12.5

- 5,000 TYG4 113 calls, 54

- -5,000 wk3 TY 112 puts, 4 vs. 112-08

- 2,000 TYF4 111.5/112/112.5 put flys, 10 ref 112-18.5

- 1,000 FVF4 108/109.5 call spds vs. 2,000 FVG4 110/111.5 call spds ref 108-18.25

- 1,500 TYF4 111/112 call spds ref 112-09

- 2,400 TYF4 111.25 puts, 5 ref 112-15.5

EGBs-GILTS CASH CLOSE: Weak Eurozone PMIs Provide Boost Into The Weekend

The UK and German curves bull flattened Friday to close out a very strong week for European bonds.

- Unexpectedly weak German and French December flash PMIs saw core/semi-core EGBs soar early in the session. UK Services PMI beat consensus, but the negative impulse on Gilts was fleeting.

- An unexpected pushback against Fed rate cut speculation by New York Fed President Williams saw EGBs and Gilts pull away from the session's best levels in the afternoon in sympathy with Treasuries.

- But the momentum begun by the Fed's dovish communications midweek and the PMIs saw core FI enjoy a strong close, with UK and German yields down roughly the same magnitude on the day.

- The BOE announced in Q1 2024 it would move from APF sales with equal sizes across maturity buckets, to a higher weight on shorter-maturity sales (by way of equal sizes in terms of initial proceeds when the instruments were purchased). Market reaction was limited.

- 10Y Gilts closed their 2nd best week of the year, falling 35.4bp.

- Periphery EGB spreads were mostly wider, with the exception of Greece which had underperformed in previous sessions.

- Next week kicks off with German IFO data and multiple ECB officials appearing, including Schnabel and Lane.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 6.3bps at 2.504%, 5-Yr is down 8bps at 1.999%, 10-Yr is down 10.3bps at 2.016%, and 30-Yr is down 11.2bps at 2.215%.

- UK: The 2-Yr yield is down 7.2bps at 4.29%, 5-Yr is down 8.1bps at 3.736%, 10-Yr is down 10.2bps at 3.687%, and 30-Yr is down 13.4bps at 4.16%.

- Italian BTP spread up 3.4bps at 170.7bps / Greek down 0.8bps at 116bps

EGB Options: Large Euro Rate Put Structures Buying To Round Off A Busy Week

Friday's Europe rates / bond options flow included:

- RXF4 136/135 put spread paper paid 17.5 on 5K

- ERG4 96.37/96.25ps 1x2, bought for 2.5 in 6.5k

- ERH4 96.00p, bought for half in 8k

- ERH4 96.37/96.25/96.12/96.00p condor, bought for 5.75 in 20k

- ERM4 96.50/97.00^^, bought for 27 in 11k

FOREX Greenback Recovers As Initial Fed Speak Leans Relatively Hawkish

- On Friday, the dollar index has recovered around 0.6% of its substantial losses this week. The first speaker since the FOMC meeting, Fed’s Williams, stated we aren’t really talking abut rate cuts right now and that it is premature to really be thinking about timing of monetary easing.

- Greenback strength was broad based but has only put a small dent in the larger post-fed adjustment with the DXY sitting well over a percent below pre-FOMC levels. In particular, the Euro has been the main victim on Friday, with some weaker than expected PMIs for France, Germany and the EU all weighing throughout European trade.

- EURUSD is down 0.85% and has spent the late session oscillating around the 1.09 mark. The EURUSD recovery this week is a bullish development and signals the end of the recent corrective pullback between Nov 29 - Dec 8. The continuation higher suggests scope for a test of key short-term resistance at 1.1017, the Nov 29 high and a bull trigger. Moving average studies are in a bull-mode position, highlighting an uptrend. Key support has been defined at 1.0724, the Dec 8 low.

- At the other end of the G10 leaderboard, the Norwegian krone is the best performer with EURNOK down another 1.35%. The surprise rate hike and overall firmer price action for oil continues to support the NOK’s recovery.

- Just German IFO on Monday’s docket before the focus turns to Tuesday’s Bank of Japan meeting and Canadian CPI.

Late Equity Roundup: Paring Gains

- Stocks have pares gains in late trade, Dow and S&P indexes lagging the Nasdaq as longs square-up, take profits ahead of the weekend. Currently, DJIA trades down DJIA down 53.1 points (-0.14%) at 37193.93, S&P E-Mini Futures down 11.25 points (-0.24%) at 4762.25, Nasdaq up 22.1 points (0.1%) at 14783.04.

- Leading gainers: IT and Consumer Discretionary sectors continue to outperform in late trade, semiconductor shares buoyed the former: First Solar +5.0%, Enphase +3.19%, Intel +1.93%. Broadline retailers supported the Consumer Discretionary sector with Amazon +1.17%, Home Depot +0.17%, Lowe's +0.1%.

- Laggers: Real Estate and Utilities sectors continued to underperform, real estate investment trusts, particularly for office and residential weighed on the former: Boston Properties -3.26%, Alexandria Real Estate -3.93%, Invitation Homes -3.51%. Multi energy providers weighing on the latter: Exelon -5.67%, Ameren -4.21%, Eversource Energy -2.88%.

- A bullish theme in S&P e-minis remains intact and the contract is trading closer to its recent highs. The rally this week confirms a resumption of the uptrend that started Oct 27. Note too that the contract has cleared resistance at 4738.50, the Jul 27 high, reinforcing current positive trend conditions. This signals scope for a climb towards 4800.00 next. On the downside, initial firm support lies at 4632.25, the 20-day EMA.

E-MINI S&P TECHS: (H4) NORTHBOUND

- RES 4: 4899.09 1.382 proj of Nov 10 - Dec 1 - 7 price swing (cont)

- RES 3: 4862.08 1.236 proj of Nov 10 - Dec 1 - 7 price swing (cont)

- RES 2: 4808.25 High Jan 4 2022 and major resistance

- RES 1: 4800.00 Round number resistance

- PRICE: 4762.50 @ 1515 ET Dec 15

- SUP 1: 4696.75 Low Dec 13

- SUP 2: 4632.25 20-day EMA

- SUP 3: 4594.00 Low Nov 30

- SUP 4: 4548.59 50-day EMA

A bullish theme in S&P e-minis remains intact and the contract is trading closer to its recent highs. The rally this week confirms a resumption of the uptrend that started Oct 27. Note too that the contract has cleared resistance at 4738.50, the Jul 27 high, reinforcing current positive trend conditions. This signals scope for a climb towards 4800.00 next. On the downside, initial firm support lies at 4632.25, the 20-day EMA.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 18/12/2023 | 0900/1000 | *** |  | DE | IFO Business Climate Index |

| 18/12/2023 | 1030/1030 |  | UK | BOE's Broadbent speech at London Business School | |

| 18/12/2023 | 1330/1430 |  | EU | ECB Schnabel Lectures On EU Fiscal Policy And Governance | |

| 18/12/2023 | 1500/1000 | ** |  | US | NAHB Home Builder Index |

| 18/12/2023 | 1500/1600 | | EU | ECB Lane Chairs Panel on EMU Reforms | |

| 18/12/2023 | 1630/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 18/12/2023 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.