Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- MNI US DATA: GDP Q4 Beat Belies Weak Domestic Demand Details

- IMF WEIGHS UKRAINE AID PACKAGE WORTH AS MUCH AS $16 BILLION, Bbg

- Why the Fed Should Raise Rates 50 Basis Points: Mohamed El-Erian, Bbg

US TSYS: Late Market Roundup: Yields Higher Ahead Fri's Personal Income

Tsys have another whip-saw session, weaker across the board after the bell (30YY 3.6207% +.0270) to near mid-range for the session, yield curves flatter after spending much of the day steeper (2s10s -1.022 at -69.981). Robust volumes on two-way trade (TYH3>1.1m).

- Tsys extend lows (30YY taps3.662% high) before bouncing slightly after Q4 GDP climbs 2.9% (annual rate) - higher than estimated 2.6%, The real GDP beat for the Q4 advance was much less flattering in the details, heavily boosted by changes in inventories swinging from -1.2 to +1.5pps. Weekly claims lower than exp at 186k vs. 205k est, Core Durables beat and New Home Sales stabilized.

- Tsys pared losses after strong $35B 7Y note auction (91282CGJ4) breaking string of three consecutive tails w/ 3.517% high yield vs. 3.537% WI; 2.69x bid-to-cover vs. 2.45x last month. Also of note - January was clean-sweep for Tsy coupon/bond auctions, every one trading through this month.

- Fed funds implied hike for Feb'23 at 26.4bp, Mar'23 cumulative 46.9bp to 4.798%, May'23 56.8bp to 4.897%, terminal at 4.895% in Jun'23.

- Focus turns to Friday's personal income (+0.1% vs. +0.4%) and spending (-0.3% vs. +0.1%) release, last component ahead next week Wed's FOMC policy annc.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00343 to 4.30457% (-0.000057/wk)

- 1M +0.03000 to 4.54729% (+0.02401/wk)

- 3M -0.01214 to 4.80243% (-0.01314/wk)*/**

- 6M -0.00600 to 5.10229% (+0.00029/wk)

- 12M -0.03843 to 5.30086% (-0.04643/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 4.82971% on 1/12/23

- Daily Effective Fed Funds Rate: 4.33% volume: $111B

- Daily Overnight Bank Funding Rate: 4.32% volume: $292B

- Secured Overnight Financing Rate (SOFR): 4.31%, $1.157T

- Broad General Collateral Rate (BGCR): 4.27%, $467B

- Tri-Party General Collateral Rate (TGCR): 4.27%, $445B

- (rate, volume levels reflect prior session)

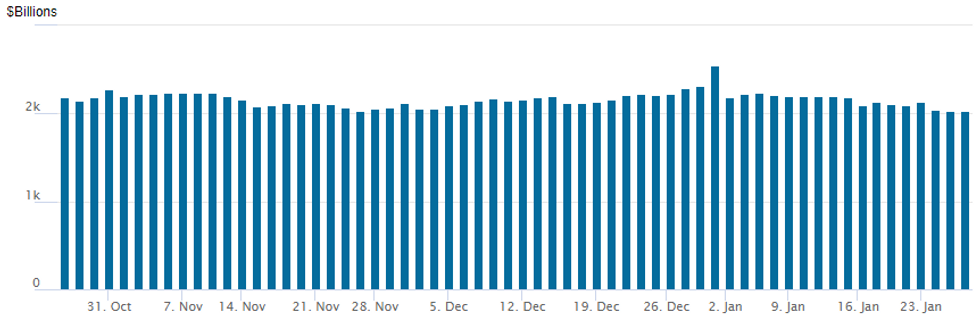

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $2,024.069B w/ 97 counterparties vs. prior session's $2,031.561B. Compares to Friday, Dec 30 record/year-end high of $2,553.716B (prior record high was $2,425.910B on Friday, September 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Consistent and varied put structures dominated Thursday's FI option trade, particularly in SOFR options hedging modest rate hike affect on mid-2023 to mid-2024. Limited downside put fly and funded condors include:- SOFR Options:

- Block, 12,000 OQM3 95.50/95.75/96.25 put flys, 10.0 ref 96.56

- Block, 7,000 SFRK3 94.81/94.93/95.06 put flys 2.25 over SFRK3 95.31/95.43 call spds

- Block, 10,000 SFRJ3 95.25/95.37 call spds, 2.0 ref 95.105

- Block, 20,000 OQM3 95.50 puts, 4.0 ref 96.58

- Block, 7,000 SFRU3 94.50/94.87/95.12/95.5 put condors, 17.5 net vs. 95.28/0.10%

- Block, 8,000 SFRJ3 94.87/95.00/95.12/95.18 broken put condors 0.5 over SFRJ3 95.31/95.43 call spds

- +15,000 SFRK3 94.75/95.00 2x1 put spds, 3.5

- Block, 6,000 OQH3 96.37/96.75 call spds 2.0 over 95.62/95.87 put spds vs 96.135/0.34%

- Block, 5,000 SFRU3 95.25/95.50 put spds, 15.5 vs. 95.275/0.10%

- Block, 6,000 SFRH4 95.00/96.00 put spds 28.5 vs. 96.15/0.25%

- 2,000 OQG3 96.50/96.75/97.00 call flys ref 96.175

- Block, total 6,500 SFRZ3 94.62/94.87/95.12/95.37 put condors, 6.0 vs. 95.625/0.05%

- 6,000 OQM3 96.00 puts ref 96.625

- 2,000 SFRM3 95.06/95.12 put spds ref 95.14

- 21,000 OQH3 96.75/97.00/97.25 call flys ref 96.195

- 4,000 SFRZ3 94.25/95.00/95.50 broken put flys, ref 95.67

- 1,500 SFRU3 94.25/94.75/95.25 put flys ref 95.32

- Treasury Options:

- 1,500 TYH3 116.5/117.5 call spds, 9 ref 114-28

- 1,700 FVK3 107.75/112.25 strangles around 35.5 ref 109-29.75

- 2,500 FVH 112 calls, 3 ref 109-15.25

- 1,500 TYG3 111/112/113.5 put trees, 14 ref 114-29

- over -5,500 TYH3 118 calls, 8 ref 115-00

- 3,000 FVG3 110 calls, 2.5 ref 109-18.25

- over 10,000 TYH3 111/112 put spds ref 114-31

- Over 13,000 TYG3 114 puts, 1-2 ref 115-04 to 114-23

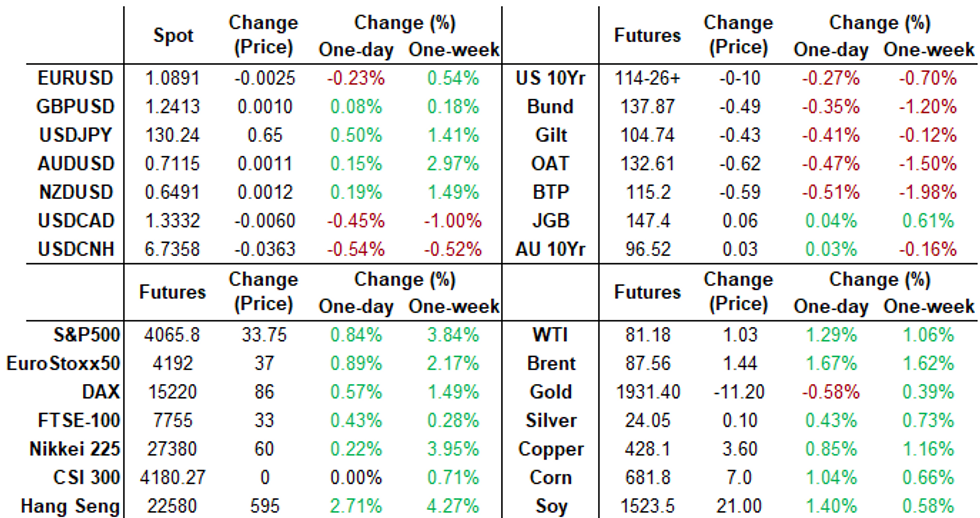

FOREX: Mixed Currency Performance Across G10 Following US Growth Data

- The US GDP beat for the Q4 advance (2.9% vs cons 2.6%) provided an initial spike for the greenback on Wednesday. However, with the details of the report much less flattening, and core PCE coming in exactly in line with expectations at 3.9% annualized, the initial USD strength almost immediately reversed course.

- Most major pairs traded back to pre-data levels as market participants digested the data, which appears very unlikely to move the needle for next week's Fed decision.

- With that said, the USD index looks set to post a quarter percent gains approaching the APAC crossover, with the data doing enough to halt the greenback slide that culminated in the DXY printing fresh trend lows at 101.50 during today’s session.

- Both CAD and CNH are topping the G10 leaderboard, with roughly half a percent gains amid the moderate advances for major equity indices. Perhaps reflecting a similar narrative, the Japanese Yen is one of the worst performers, with USDJPY consolidating back above the 130 handle.

- The pair made a new weekly low of 129.03 overnight before bouncing impressively both ahead of and post the US data. The USDJPY trend outlook remains bearish for now and resistance at 131.58, the Jan 18 high, remains intact.

- Friday’s docket is highlighted by US Core PCE Price index data, as well as personal income/spending, pending home sales and university of Michigan sentiment data.

FX: Expiries for Jan27 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0500(E1.6bln), $1.0700($1.5bln), $1.0780-00(E1.2bln), $1.0825-35(E1.3bln), $1.0850(E858mln), $1.0880-00(E1.2bln), $1.0950(E825mln), $1.1000(E613mln)

- EUR/GBP: Gbp0.8800(E1.2bln), Gbp0.8825-30(E572mln)

- USD/JPY: Y130.00($548mln), Y131.00($549mln), Y132.50($611mln)

- USD/CAD: C$1.3395-15($756mln), C$1.3500($1.0bln)

Late Equity Roundup

Major indexes trading firmer, near top end of range, Energy and Consumer Discretionary sectors still extending gains. SPX eminis currently trades +29.5 (0.73%) at 4061.5; DJIA +125.79 (0.37%) at 33868.99; Nasdaq +144.4 (1.3%) at 11457.75.

- SPX leading/lagging sectors: Energy (+2.81%) lead by O&G refiners (CVX +4.66%, XOM +3.52%, OXY +2.99%, VLO +3.63%). Consumer Discretionary next up (+1.54%) lead by auto make Tesla: +9.16% following earnings, strong guidance (not to mention price target upgrades from Wedbush and Cowen.

- Laggers: Consumer Staples (-0.25%), followed by Health Care (-0.05%) w/ pharmaceuticals and bio-tech names weighing (PFE -2.36%, MRK -2.42%, BMY -0.79%).

- Dow Industrials Leaders/Laggers: Chevron (CVX) +7.94 at 187.02, Microsoft (MSFT) +5.50 at 246.11, Salesforce.com (CRM) +6.44 at 162.61. Laggers: IBM -5.47 at 135.29, Merck (MRK) -2.56 at 106.03, AMGN -2.50 at 254.04.

E-MINI S&P (H3): Fresh Short-Term Highs

- RES 4: 4194.25 High Sep 13

- RES 3: 4180.00 High Dec 13 and the bull trigger

- RES 2: 4090.75 High Dec 14

- RES 1: 4065.50 Intraday high

- PRICE: 4063.50 @ 1515ET Jan 26

- SUP 1: 3944.42 50-day EMA

- SUP 2: 3901.75/3891.50 Low Jan 19 / Low Jan 10

- SUP 3: 3788.50/78.45 Low Dec 22 / 61.8% of Oct 13-Dec 13 uptrend

- SUP 4: 3735.00 Low Nov 3

S&P E-Minis have recovered from yesterday’s low and price is trading higher today . Key short-term resistance at 4056.75, Jan 23 high, has been breached. This confirms a resumption of recent bullish activity and signals scope for a climb towards 4100.00 and key resistance at 4180.00 further out, Dec 13 high. The key short-term support to watch lies at 3901.75, Jan 19 low. A break would be a bearish development.

Friday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 27/01/2023 | 0030/1130 | ** |  | AU | Trade price indexes |

| 27/01/2023 | 0700/0800 | ** |  | SE | Unemployment |

| 27/01/2023 | 0700/0800 | ** | | SE | Retail Sales |

| 27/01/2023 | 0745/0845 | ** |  | FR | Consumer Sentiment |

| 27/01/2023 | 0800/0900 | *** |  | ES | GDP (p) |

| 27/01/2023 | 0900/1000 | ** |  | EU | M3 |

| 27/01/2023 | 1330/0830 | ** |  | US | Personal Income and Consumption |

| 27/01/2023 | 1500/1000 | ** | | US | NAR pending home sales |

| 27/01/2023 | 1500/1000 | *** | | US | Final Michigan Sentiment Index |

| 27/01/2023 | 1600/1100 |  | CA | Finance Dept monthly Fiscal Monitor (expected) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.