Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- ECB LAGARDE: FULL EFFECTS OF ECB POLICY STARTING TO MATERIALIZE, Bbg

- SAUDIS `FED UP' WITH OPEC MEMBERS NOT MEETING OIL OUTPUT GOALS, Bbg

- IRAN AND SAUDI TO REOPEN DIPLOMATIC MISSIONS THIS WEEK: ISNA

- KREMLIN: RUSSIA READY TO TALK TO US ON NUCLEAR ARMS CONTROL:IFX - Bbg

US Tsys: ISM Miss Helps Tsys Snuff Bearish Engulfing Candle

- Treasury futures reversed early losses, gapped to new session highs (TYU3 114-03.5 high, yield tapped 3.6563% low) after May ISM services miss. Curves rebound with short end rates outperforming (2s10s taps -77.212 high).

- Despite the bounce, technical focus is on the bearish engulfing candle posted Friday, signaling the end of the recent recovery and suggesting potential for a continuation lower. Attention is on key short-term support and the bear trigger at 112-29+, the May 26 / 30 low.

- May ISM services disappointed: 50.3 (cons 52.4) after 51.9, printing the lowest since Dec’22. New orders led the decline at 52.9 (-3.2pts), driven domestically rather than external.

- The prices paid index is notable, dropping to lowest since May’20 at 56.2 (-3.4pts) as they build further on March’s particularly sharp -6.1pt drop. Employment component also fell back below 50 (49.2, -1.6pts) for first time since December.

- FOMC-dated OIS have lifted off lows seen after the ISM services miss. Near-term meetings are relatively little changed compared to the start of today’s NY session with June +7bp (unch) and July +20bp (-1.5bp) for a terminal that doesn’t fully price another hike.

- Beyond that, implied rates are down more heavily on the day but remain notably higher than before Friday’s payrolls report. For example, the 4.99% implied effective for the Dec FOMC (marking 9bp of cuts from current levels) is down 4bps since the start of the session but still 11bps higher since payrolls.

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.00935 to 5.15002 (-.01277 total last wk)

- 3M +0.02289 to 5.25323 (-.03340 total last wk)

- 6M +0.04226 to 5.28773 (-.05289 total last wk)

- 12M +0.06557 to 5.09254 (-.13117 total last wk)

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00086 to 5.06471%

- 1M +0.00200 to 5.19057%

- 3M +0.01285 to 5.0914 */**

- 6M +0.03986 to 5.66329%

- 12M +0.12228 to 5.77957%

- * Record Low 0.11413% on 9/12/21; ** New 16Y high: 5.51671% on 5/31/23

- Daily Effective Fed Funds Rate: 5.08% volume: $141B

- Daily Overnight Bank Funding Rate: 5.06% volume: $309B

- Secured Overnight Financing Rate (SOFR): 5.07%, $1.475T

- Broad General Collateral Rate (BGCR): 5.05%, $609B

- Tri-Party General Collateral Rate (TGCR): 5.05%, $600B

- (rate, volume levels reflect prior session)

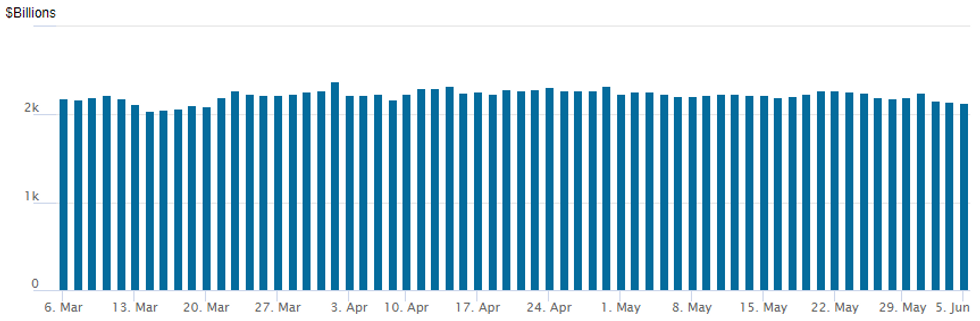

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $2,131.417B w/ 105 counterparties, compares to prior $2,142.102B. Compares to high usage for 2023: $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

SOFR/TREASURY OPTIONS SUMMARY

Early downside puts gave way to some chunky upside call buying Monday as underlying SOFR and Treasury futures recover from weak opening levels, gap higher following disinflationary ISM services miss.

- SOFR Options:

- 10,000 SFRM3 94.68/94.75/94.81put flys ref 94.73 to -.7275

- Block, 6,000 OQU3 98.00 calls, 4.5 ref 96.37

- over 8,000 OQM3 95.87/96.00 put spds, 15.5-16.0

- Block, 30,000 SFRH4 97.00/98.00 call spds, 10.0 ref 95.43

- Block, 5,000 SFRU3 94.00/94.50 put spds, 7.0 ref 94.765

- over 11,600 SFRU3 98.00 calls, 1.5 ref 94.77

- Block/screen 9,500 SFRU3 94.50 puts, 10.5 vs. 94.75 -.755/0.32%

- 1,500 SFRZ3 94.75/94.93/95.12 put flys, ref 95.025

- Block, 4,000 SFRN3 94.56/94.81 put spds, 11.0 ref 94.775

- 1,000 SFRQ3 94.62/94.75 put spds ref 94.76

- 1,000 SFRU3 94.43/94.56 put spds vs. 95.00/95.12 call spds

- Treasury Options:

- 3,000 TYN3 113.75 straddles, 137

- 2,000 USN3 130/133 call spds, 28 ref 128-02

- over 7,000 TYN3 111 puts, 5 ref 113-31.5

- over 28,000 FVN3 112 calls, 2 ref 108-20.5 to -22.75

- 3,200 FVQ3 109.5 calls, 29.5 ref 108-15

- 7,500 FVQ3 106.75 puts appr 6.5 over 110/112 call spds ref 108-11

- over 6,800 TYN3 112.5 puts, mostly at 26 ref 113-16.5

- 1,700 FVN3 107.5 puts, 17.5 ref 108-12.5

- 1,000 TYU3 115/117/119 call flys ref 113-14

- 1,250 TYU3 110/111.5 put spds, ref 113-14

- 2,500 TYN3 116 calls, 8 ref 113-16.5

- 1,250 TYN3 113.5/114 put spds ref 113-18.5

EGBs-GILTS CASH CLOSE: Bear Flattening Resumes

The German and UK curves continued Monday where they left off on Friday with more bear flattening, as dovish central bank hike prospects were reconsidered.

- While curve inversions continue to deepen, the market action of the past couple of sessions has contrasted with the bull flattening seen in the first half of last week amid softer-than-expected Eurozone inflation readings.

- With ECB and BoE peak rate prospects up 2-3bp on the day, Schatz and 2Y UK yields rose 8+bp and are up 19bp from last week's lows; for 10Ys, Bund is up 15bp from last week's low with Gilt up 11bp.

- Central bank commentary didn't move the needle (ECB's Lagarde, Vujcic, Nagel), while European Services/Composite PMIs were mixed (and mostly finals).

- A disinflationary US Services ISM report dragged down European yields in mid-afternoon, but they soon rebounded.

- Periphery EGB spreads were little changed. The BTP Valore retail bond saw strong orders on its first day of sale (over E5.4bln).

- Tuesday sees Eurozone retail sales and consumer survey, along with German factory orders.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

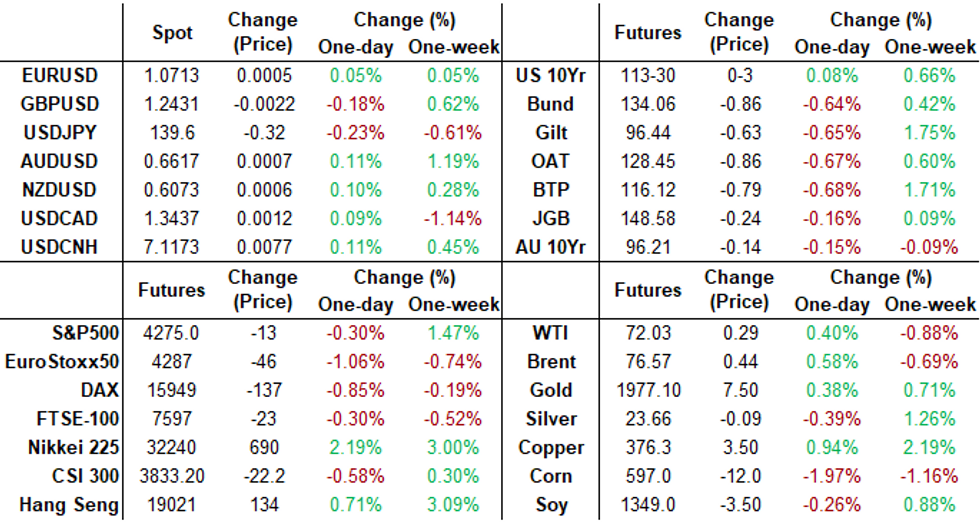

- Germany: The 2-Yr yield is up 8.7bps at 2.889%, 5-Yr is up 6.6bps at 2.403%, 10-Yr is up 6.9bps at 2.381%, and 30-Yr is up 5.6bps at 2.545%.

- UK: The 2-Yr yield is up 8.2bps at 4.445%, 5-Yr is up 6.7bps at 4.169%, 10-Yr is up 5.2bps at 4.208%, and 30-Yr is up 3.1bps at 4.511%.

- Italian BTP spread down 0.1bps at 175.7bps / Spanish down 0.8bps at 99.5bps

EGB Options: Par Euribor Call Buying Makes Another Appearance Monday

Monday's Europe rates / bond options flow included:

- RXQ3 137c sold at 68 and 67 in 15k

- ERM4 100c, bought for 2.5 in 10k - this was also bought on the 26th May for 2.75 in 5k.610k Open Interest at that strike

- ERU3 96.50/97.00cs 1x2, bought for 0.75 in 2.5k

DXY Hovers Around Unchanged As ISM Services PMI Takes Shine Off Greenback

- Early greenback strength on Monday, largely an extension of post-payrolls demand, dissipated in US hours as weaker US data took the shine off the renewed greenback optimism. USDJPY was the most impacted following the data, as has regularly been the case in recent times given the sensitivity to US yields.

- Lower than expected final S&P PMIs set the tone for the pair, with the downside move gaining traction through the overnight lows and then extending on the significant miss for ISM services index (52.4 vs 50.3 est.).

- After reaching as high as 140.45 in early Europe, USDJPY sank to a fresh low of 139.25 although around 50 pips of that move have been pared as we approach the APAC crossover.

- Bullish conditions remain intact with pullbacks appearing to be corrective at this juncture. Recent highs resulted in a test of the top of a bull channel, drawn from the Jan 16 low which intersects at 141.01 today and represents a key resistance. A clear break of it would reinforce bullish conditions and open 141.61, the Nov 23 2022 high. Key support to watch is 138.20, the 20-day EMA.

- Yen weakness beyond the 140.00 level has drawn increased verbal rhetoric from Japan authorities in recent weeks, so this will likely remain a focus point going forward if we see meaningful weakness beyond this figure level. Labour cash earnings and household spending data is due overnight. Final Q1 GDP figures will be released on Thursday, as well as April current account data.

FX Expiries for Jun06 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0685-00(E1.1bln), $1.0750(E2.3bln)

- USD/JPY: Y140.00($1.5bln)

- AUD/USD: $0.6640-45(A$515mln)

- USD/CAD: C$1.3365($500mln)

US EQUITIES ROUNDUP: Late Session Sell-Off

- Stocks extending modest session lows, SPX and Nasdaq joining weaker Dow components in the last few minutes. At the moment, S&P E-Mini futures are down 10 points (-0.23%) at 4278.25; Nasdaq down 21.4 points (-0.2%) at 13223.3; DJIA down 175.3 points (-0.52%) at 33595.97.

- Industrials, Financials and Real Estate sectors continue to lead underperform while some notable weakness in Information Technology sector noted: EPAM Systems Inc, a software and services outsourcing company is trading 20% lower, Intel a distant second is down 4.05%, HP Inc -3.5%.

- Shares of Apple have pared early gains, back near steady after announcing a mixed reality headset in new tech conference.

- On the flipside, Materials, Communication Services and Health Care sectors continue to outperform.

- Despite the late dip, S&P E-minis trend conditions remain bullish and the contract traded higher Friday. Resistance at 4244.00, the Feb 2 high and a medium-term bull trigger, has been cleared. The break reinforces bullish conditions and confirms a resumption of the uptrend that started in October 2022. This opens 4327.50 next, the Aug 16 2022 high (cont). The 50-day EMA, at 4144.35 remains a key support. A break of this average is required to signal a reversal.

E-MINI S&P TECHS: (M3) Clears Key Resistance

- RES 4: 4400.00 Round number resistance

- RES 3: 4393.25 High Apr 22 2022 (cont)

- RES 2: 4327.50 High Aug 16 2022 (cont)

- RES 1: 4301.00 High Jun 5

- PRICE: 4278.50 @ 1450 ET Jun 5

- SUP 1: 4229.00 Low Jun 2

- SUP 2: 4184.26 20-day EMA

- SUP 3: 4144.35 50-day EMA

- SUP 4: 4144.00 Low May 24 and a key support

S&P E-minis trend conditions remain bullish and the contract traded higher Friday. Resistance at 4244.00, the Feb 2 high and a medium-term bull trigger, has been cleared. The break reinforces bullish conditions and confirms a resumption of the uptrend that started in October 2022. This opens 4327.50 next, the Aug 16 2022 high (cont). The 50-day EMA, at 4144.35 remains a key support. A break of this average is required to signal a reversal.

COMMODITIES: Gains From OPEC+ & Saudi Cut Fizzle Out With Demand Concerns

- Crude oil gains are fizzling out, after early large increases following Saudi Arabia pledging an additional 1mbpd voluntary production cut in July. The move came after the weekend OPEC+ meeting at which other members pledged to extend existing cuts until the end of 2024. UAE secured a higher quota for next year as the lower targets for Russia, Nigeria and Angola represent little change in actual output with targets brought into line with current production levels.

- IEA’s Birol says crude prices are likely to rise a lot more, with the market already expecting an imbalance in the oil market in 2H23 and these new measures further deepening the gap.

- Nevertheless, WTI is up just +0.35% at $72.01 off its intraday high of $75.06 straight off the open. It doesn’t trouble support at $70.00 (Jun 2 low). The day’s most active strikes in the CLN3 have been for $80/bbl calls.

- Brent is +0.6% at $76.59 off an intraday high of $78.73 and above support at $74.18 (Jun 2 low).

- Gold is +0.7% at $1961.85, a decent size increase with only modest USD net depreciation on the day and Treasury yields paring earlier declines on the ISM services miss. A pre-ISM low of $1938.25 came closer to but didn’t trouble support at $1932.2 (May 31 low) whilst resistance remains at the key short-term $1985.3 (May 24 high).

Tuesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 06/06/2023 | 2301/0001 | * |  | UK | BRC-KPMG Shop Sales Monitor |

| 06/06/2023 | 0430/1430 | *** |  | AU | RBA Rate Decision |

| 06/06/2023 | 0600/0800 | ** |  | DE | Manufacturing Orders |

| 06/06/2023 | 0700/0900 | ** |  | ES | Industrial Production |

| 06/06/2023 | 0730/0930 | ** |  | EU | IHS Markit Final Eurozone Construction PMI |

| 06/06/2023 | 0830/0930 | ** | | UK | IHS Markit/CIPS Construction PMI |

| 06/06/2023 | 0900/1100 | ** | | EU | Retail Sales |

| 06/06/2023 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 06/06/2023 | 1230/0830 | * |  | CA | Building Permits |

| 06/06/2023 | 1255/0855 | ** |  | US | Redbook Retail Sales Index |

| 06/06/2023 | 1400/1000 | * | | CA | Ivey PMI |

| 06/06/2023 | 1400/1000 | ** | | US | IBD/TIPP Optimism Index |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.