Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- MNI US DATA: ADP Employment Misses With Weather Impact

- WHITE HOUSE LIKELY TO TAP BRAINARD TO RUN NEC, CNBC SAYS, Bbg

- US TREASURY KEEPS REFUNDING AUCTIONS IDENTICAL TO PRIOR QUARTER, Bbg

- BN 02/01 13:30 *TREASURY SAYS DEBT LIMIT MEASURES SHOULD LAST UNTIL EARLY JUNE, Bbg

- CHINA, HK TO SCRAP COVID TESTING, QUOTA SYSTEM FOR BORDER: SCMP

- OPEC+ DECIDES TO KEEP OUTPUT LEVELS UNCHANGED:IRAQ OIL MINISTRY, Bbg

US TSYS: Market Reacts as if Rate Hikes Wont Last Much Longer

Tsys experienced a whip-saw session even before the after FOMC policy pivot, 25bp hike to 4.5%. Rates (and stocks: ESH3 taps 4160.75 high) gapped higher after initial two way flow, markets essentially saying any further hikes from the Fed will not run out the calendar very far. As Chairman Powell said himself: the "disinflation process has begun".

- Fed funds implied hike for Mar'23 at 20.4bp, May'23 cumulative 29.8bp to 4.882%, Jun'23 30.7bp to 4.890%, terminal at 4.89% in Jun'23.

- Early data reacts: Tsys extended early highs after ADP jobs data climbed +106k, much less than estimated 180k jobs.

- Fast two-way trade between Mfg PMI and ISM saw bonds sell-off/extend lows (30YY tapped 3.6429% high) as ISM mfg index comes out lower than est at 47.4 (48.0 est), mfg orders, production weakest since mid 2020. JOLTS job openings rise to 11.01M vs. 10.3 est..

- A sharp bond-lead sell-off likely driven by two large steepener Blocks: total +20,000 TYH3 at 114-29 to -28.5 vs. -8,700 USH initially from 130-19 down to 130-12. Tsy 30Y futures fell to 129-31 low by midmorning before staging a rebounding in the lead up to the FOMC.

- Focus now turns to Friday's employment report for January (+175k est vs. +223k prior).

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00157 to 4.29686% (-0.00785/wk)

- 1M +0.00071 to 4.57500% (-0.00387/wk)

- 3M -0.01728 to 4.79629% (-0.02900/wk)*/**

- 6M -0.01257 to 5.08786% (-0.01443/wk)

- 12M -0.02228 to 5.31529% (-0.00085/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 4.82971% on 1/12/23

- Daily Effective Fed Funds Rate: 4.33% volume: $98B

- Daily Overnight Bank Funding Rate: 4.32% volume: $251B

- Secured Overnight Financing Rate (SOFR): 4.31%, $1.281T

- Broad General Collateral Rate (BGCR): 4.28%, $482B

- Tri-Party General Collateral Rate (TGCR): 4.28%, $468B

- (rate, volume levels reflect prior session)

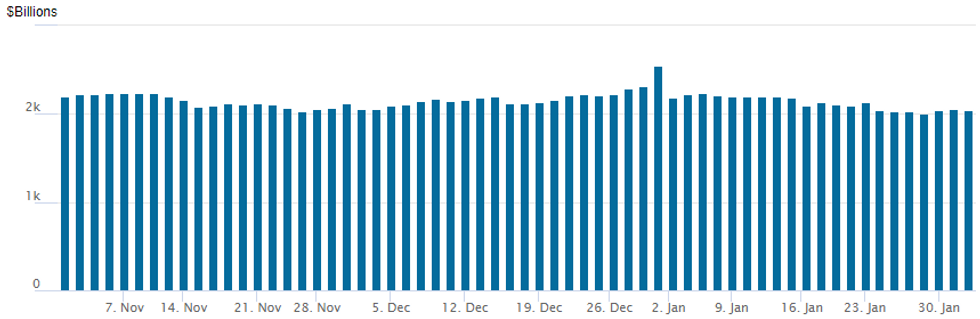

FED Reverse Repo Operation

NY Federal Reseve/MNI

NY Fed reverse repo usage slipped to $2,038.262B w/ 100 counterparties vs. prior session's $2,061.572B. Compares to Friday, Dec 30 record/year-end high of $2,553.716B (prior record high was $2,425.910B on Friday, September 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Heavy option volume in the lead up to - and after the FOMC pivot to 25bps hike, favored upside call and call structures Wednesday. Salient SOFR trade: over +91,000 SFRZ3 95.50/97.50 call spds, 33.5-35.0 ref 95.565 to -.575 as well as 16,000 SFRZ3 95.75/97.75 call spds ref 95.57. Notable 5Y limited upside opener: +24,000 FVJ3 112.25/112.75/113.25 call flys ref 109-31.75.- SOFR Options:

- Block, 20,000 SFRZ3 97.50/98.00 call spds

- 4,000 SFRK3 95.31/95.43 call spds vs. 94.81/94.94/95.06 put flys

- 2,000 SFRH3 95.12/95.25/95.37 call flys

- 16,000 SFRZ3 95.75/97.75 call spds ref 95.57

- over +91,000 SFRZ3 95.50/97.50 call spds, 33.5-35.0 ref 95.565 to -.575

- 4,500 SFRU3 95.00/95.12/95.18/35.31 put condors ref 95.26

- Block, 5,000 SFRG3 95.18/95.25 call spds, 1.5 vs. 95.175/0.10%

- Block, 5,000 SFRM3 94.68/94.75 put spds, 0.5 ref 95.09

- Block, 2,500 SFRN3 95.25/95.62 2x3 call spds, 15.5 vs. 95.28

- Block, 6,486 SFRG3 95.12/95.18 put spds, 2.75 ref 95.17

- 2,500 OQU3 96.00 puts, 11.0 ref 96.855

- Update, over 28,500 SFRH3 95.12 puts, 2.0-2.5 ref 95.16 to -.165

- over 5,800 2QH3 96.50/96.75 put spds, ref 97.11

- 6,000 SFRG3 95.00/95.12 put spds, ref 95.165

- 6,000 OQG3 95.75/96.00 put spds ref 96.075

- 1,500 SFRG3 95.06/95.18/95.31 call flys, ref 95.16

- 2,500 SFRN3 95.31/95.75 2x3 call spds ref 95.27

- over 9,000 SFRH3 95.12 puts ref 95.16

- 15,000 SFRH3 95.25/95.31 call spds ref 95.16

- Treasury Options:

- 5,000 TYH 117/118 call spds, 9 ref 115-12.5

- over 6,000 FVH3 111 calls 4.5 ref 109-12.75

- over 7,600 FVH3 109 puts, 21 ref 109-15.5

- 4,000 USH3 124/126/128 put flys, 13 ref 130-18

- 24,000 FVJ3 112.25/112.75/113.25 call flys ref 109-31.75 - opener

- over 5,100 TYYH3 115.75 calls, 26 ref 114-26

- over 5,700 TYH3 116.5 calls, 12 ref 114-28.5 to -29

- 3,000 TYH3 115/116 call spds ref 114-19.5

EGBs-GILTS CASH CLOSE: Euro CPI Data Fails To Convince Ahead Of ECB, BoE

The German curve twist flattened modestly, underperforming its bull steepening UK While Italian and eurozone core flash CPI prints came in stronger than expected, the eurozone headline print was very soft, helping boost Bunds to session highs.

- However, MNI analysis pointed to the possibility that Eurostat used a low estimate for Germany's as yet unreleased inflation figure, which both obscures the signal from today's readings and heightens potential volatility for the delayed German release as well as the Eurozone final number.

- Markets faded the headline CPI-related jump, with strong US job openings and ISM prices data helping keep a lid on global core FI in the afternoon.

- All eyes after the cash close are on the Federal Reserve decision, with attention swiftly turning to ECB and BoE meetings (our previews are, respectively, here and here).

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

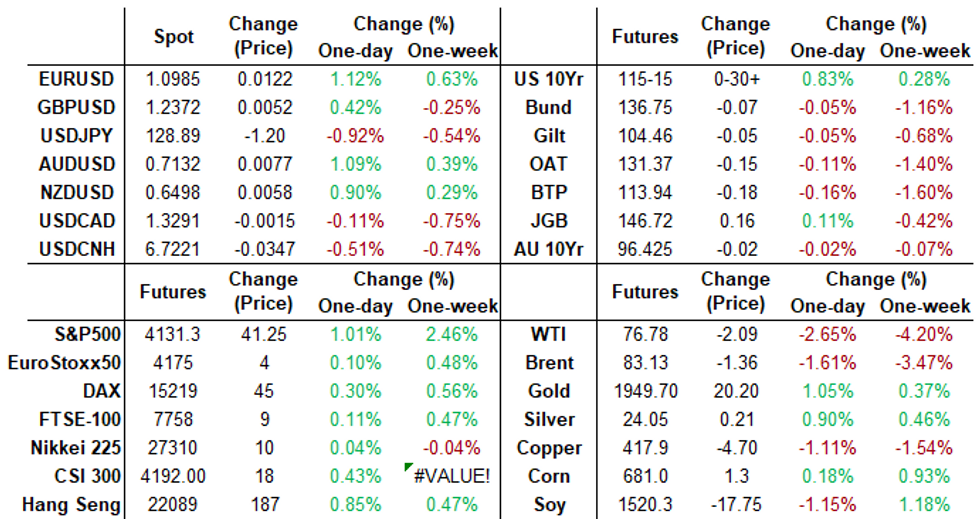

- Germany: The 2-Yr yield is up 2.1bps at 2.672%, 5-Yr is up 0.8bps at 2.318%, 10-Yr is down 0.2bps at 2.284%, and 30-Yr is up 0.3bps at 2.227%.

- UK: The 2-Yr yield is down 2.9bps at 3.439%, 5-Yr is down 3.6bps at 3.179%, 10-Yr is down 2.5bps at 3.307%, and 30-Yr is down 0.1bps at 3.712%.

- Spanish bond spread up 0.1bps at 99.7bps / Greek up 0.4bps at 202.1bps

FOREX: USD Weakness Extends As Powell Confirms Disinflation Process Started

- Despite a moderate pop higher for the greenback on the Fed’s guidance on rates remaining close to unchanged, markets quickly faded the moves. As Chair Powell confirmed the easing of price pressures and the fact the disinflation process has started, substantial greenback weakness has ensued.

- The USD index sits just over 1% weaker on the session and has extended on multi-month lows on Wednesday, continuing to press on session lows approaching the APAC crossover.

- The best performers are the Euro and the Japanese yen, along with the Australian dollar which is benefitting from the renewed optimism in equity markets.

- For EURUSD, technical bulls remain in the driver’s seat and the bull trigger at 1.0929, the Jan 26 high, has been breached. The break resumes the uptrend and initially targets 1.1022, 3.00 proj of the Sep 28 - Oct 4 - Oct 13 price swing.

- In USDJPY, the trend direction is down with price holding below resistance at 131.58, the Jan 18 high and below the 20-day EMA, at 130.57. The resumption of weakness now opens 126.81, a Fibonacci projection – with the bear trigger situated at 127.23, Jan 16 low.

- The focus quickly turns to the next major central bank meetings on Thursday with both the BOE and ECB decisions scheduled.

FX: Expiries for Feb02 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0580-00(E1.1bln), $1.0750(E669mln), $1.0855-60(E586mln), $1.0895-10(E1.1bln), $1.0925-50(E741mln), $1.1150(E744mln)

- USD/JPY: Y127.00($1.4bln), Y128.90-05($1.0bln), Y129.30-50($1.3bln), Y130.00($1.8bln), Y131.55-75($1.0bln)

- GBP/USD: $1.2315(Gbp560mln)

- USD/CNY: Cny6.9500($1.2bln)

Late Equity Roundup: Extending Post-FOMC Highs, IT Leading

Major indexes trading near late session highs after bouncing early in Chairman Powell's press conference. Information Technology and Consumer Discretionary sectors outperforming. SPX eminis currently trades +71.25 (1.74%) at 4162; DJIA +241.54 (0.71%) at 34332.74; Nasdaq +316.4 (2.7%) at 11902.14.

- SPX leading/lagging sectors: IT (+2.87%) as semiconductor shares extend gains (AMD+12.55%, MPWR +7.86%, NVDA +7.5%, AMAT +6.42%). Consumer Discretionary (+2.3%) buoyed by auto makers late (TSLA +5.36%, F +2.74%).

- Laggers: Energy (-1.26%) weighed by O&G/Consumables subsector shares (MPC -4.01% HES -3.66, EOG -3.51%, COP -3.34%).

- Dow Industrials Leaders/Laggers: Microsoft (MSFT) +5.0 at 252.81, Salesforce.com (CRM) +4.19 at 172.10, Home Depot (HD) +3.30 at 327.47. Laggers: Amgen (AMGN) -7.44 at 244.96, Travelers (TRV) -5.37 at 185.75, Chevron (CVX) -2.71 at 171.31.

- Earning after the close: Allstate (ALL; -$1.36 est), Murphy USA (MUSA; $6.36 est); MetLife (MET; $1.64 est), META ($2.26 est), McKesson (MCK; $6.35 est

E-MINI S&P (H3): Trend Signals Remain Bullish

- RES 4: 4250.00 High Aug 26, 2022

- RES 3: 4194.25 High Sep 13

- RES 2: 4180.00 High Dec 13 and the bull trigger

- RES 1: 4160.75 High Feb 1

- PRICE: 4150.75 @ 1545ET Feb 1

- SUP 1: 4007.50/3963.07 Low Jan 31 / 50-day EMA

- SUP 2: 3901.75/3891.50 Low Jan 19 / Low Jan 10

- SUP 3: 3788.50/78.45 Low Dec 22 / 61.8% of Oct 13-Dec 13 uptrend

- SUP 4: 3735.00 Low Nov 3

S&P E-Minis recovered from yesterday's low. The recent move down appears to be a correction and the uptrend remains intact - yesterday’s bounce reinforces bullish conditions. The recent breach of resistance resulted in a print above the 4100.00 handle and an extension higher would open 4180.00, the Dec 13 high and a bull trigger. Initial firm and key support has been defined at 3963.07, the 50-day EMA.

COMMODITIES: Gold Clears Bull Trigger On Powell, Crude Slips On Inventory Build

- Crude oil more than reverses yesterday’s gain, sliding through the second half of the session in a move that appeared to be ignited by EIA data showing a larger than expected crude build, before a late bounce off lows with risk supported through Fed Chair Powell’s press conference.

- The Iraq oil ministry then was quoted as saying OPEC+ has decided to keep its output levels unchanged as broadly expected, whilst Reuters reports the EU aims to agree a price cap on Russian oil products on Friday after postponing a decision today amid divisions between member states.

- WTI is -2.3% at $77.04 having earlier cleared support at $76.53 (61.8% of Jan 5-18 bull leg) before bouncing. It opens next support at $72.74 (Jan 5 low).

- Brent is -2.4% at $83.38 having come close to testing support at $82.06 (61.8% of Jan 5-23 rally).

- Gold is +1.2% at $1951.73 on post-FOMC presser USD weakness, pushing through the bull trigger of $1949.2 (Jan 26 high) to open $1963.0 (76.4% retrace of Mar – Sep 2022 bear leg).

Thursday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 02/02/2023 | 0700/0800 | ** |  | DE | Trade Balance |

| 02/02/2023 | 1200/1200 | *** |  | UK | Bank Of England Interest Rate |

| 02/02/2023 | 1200/1200 | *** | | UK | Bank Of England Interest Rate |

| 02/02/2023 | 1315/1415 | *** |  | EU | ECB Deposit Rate |

| 02/02/2023 | 1315/1415 | *** | | EU | ECB Main Refi Rate |

| 02/02/2023 | 1315/1415 | *** | | EU | ECB Marginal Lending Rate |

| 02/02/2023 | 1330/0830 | * |  | CA | Building Permits |

| 02/02/2023 | 1330/0830 | ** |  | US | Jobless Claims |

| 02/02/2023 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 02/02/2023 | 1330/0830 | ** | | US | Preliminary Non-Farm Productivity |

| 02/02/2023 | 1345/1445 | | EU | ECB Press Conference following Rate Decision | |

| 02/02/2023 | 1500/1000 | ** | | US | Factory New Orders |

| 02/02/2023 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 02/02/2023 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 02/02/2023 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 02/02/2023 | 1830/1930 | | EU | ECB Lagarde Speech at Franco-German Business Awards | |

| 03/02/2023 | 2200/0900 | * |  | AU | IHS Markit Final Australia Services PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.